Finding a mortgage broker marketplace that delivers fast competitive offers, transparent pricing, and reliable loan matchmaking is harder than expected. Some platforms hide fee schedules, restrict product information, or delay loan processing for borrowers who do not fit traditional profiles. This list compares four direct mortgage broker marketplaces so borrowers and professionals can match features, pricing, and loan types to their needs.

Table of Contents

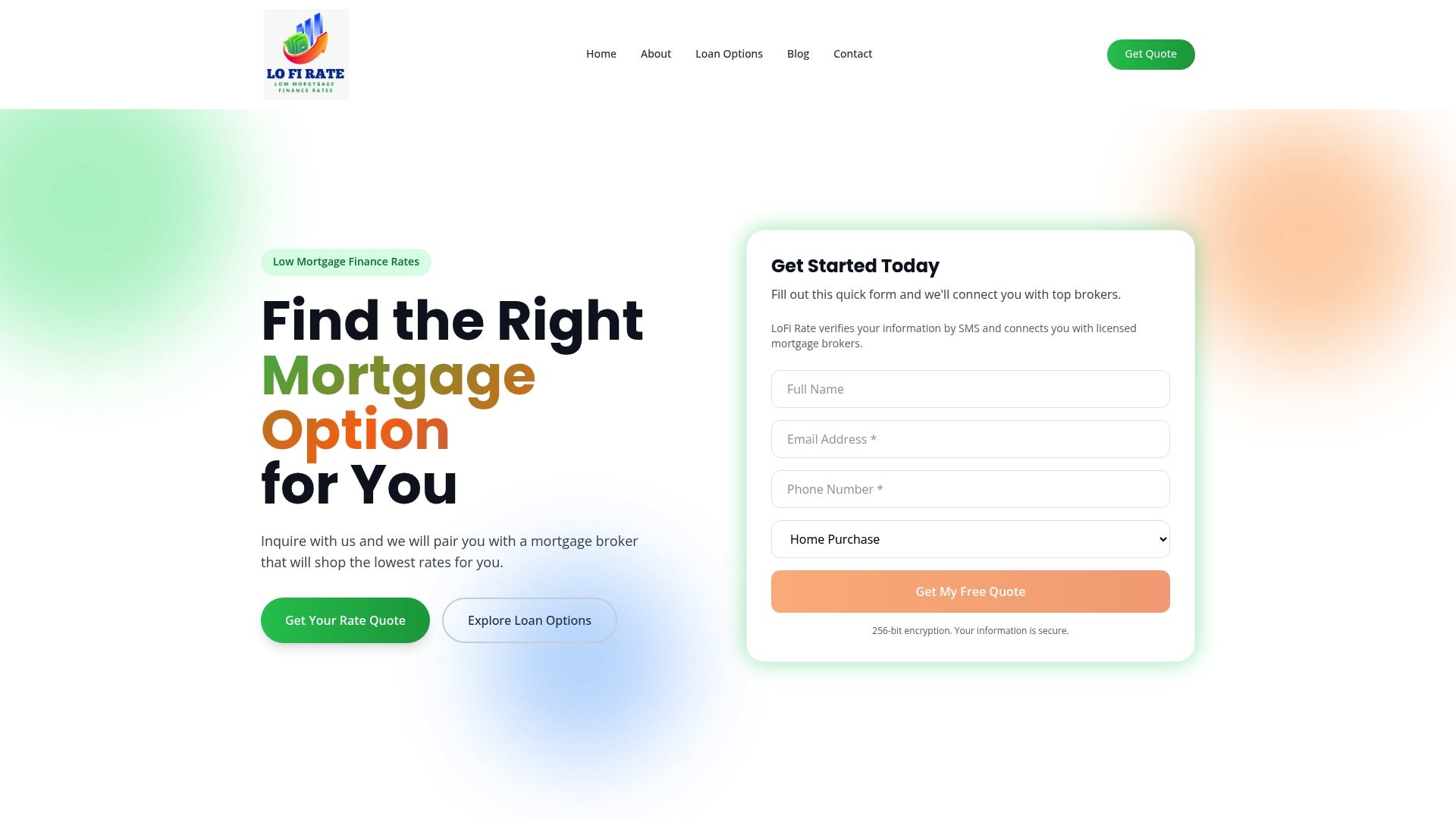

LoFi Rate

At a Glance

Free service: LoFi Rate does not charge borrowers for broker matchmaking. The platform connects you with licensed mortgage brokers across the United States who compete to present rate and term options. The site uses a secure online application so you can compare offers without visiting multiple lenders.

Core Features

LoFi Rate maintains a nationwide network of licensed mortgage brokers so borrowers can access local and national options. The platform offers a secure online application protected by 256-bit encryption and a free matching service that produces competing broker offers. It supports a wide array of mortgage products, including FHA, VA, jumbo, refinance, and investment property financing, and it presents quick rate comparisons alongside expert guidance.

Key Differentiator

Aggregates multiple licensed broker offers nationwide to simplify how borrowers shop for mortgages. That aggregation yields competing proposals from brokers rather than a single retail lender quote. The result is a side by side view of rates and terms so you can choose the offer that fits your timeline and goals.

Pros

Nationwide coverage and a broad loan menu mean first time buyers, veterans, and investors can find brokers who specialize in their loan type. The service charges no matchmaking fees, so borrowers pay only closing costs and lender specific fees rather than platform fees. Secure online forms and customer testimonials point to a mostly streamlined, remote experience where several brokers bid for your business.

Cons

- Service relies on third party brokers, so individual experience and responsiveness may vary.

Who It's For

U.S. homeowners and prospective buyers who prefer an online mortgage shopping experience will find LoFi Rate useful. It fits people who want competing broker offers without contacting many lenders directly. The platform also suits veterans, first time buyers, homeowners seeking a refinance, and investors financing rental properties.

Unique Value Proposition

Free matching with licensed brokers sends multiple competing offers to your inbox with no LoFi Rate fee. LoFi Rate does not lend money or quote rates directly. That separation keeps the platform focused on connecting you to brokers who can negotiate terms and manage underwriting while preserving transparency about where fees and lending decisions originate.

Real World Use Case

A first time homebuyer submits a secure online form and receives multiple broker matches within a short period. The borrower reviews side by side offers on rate, term, and closing costs and selects the broker with the best fit. The chosen broker then guides the borrower through application, underwriting, and closing primarily online.

Pricing

LoFi Rate is free to use for borrowers. The company charges no fee for broker matchmaking. Borrowers are responsible for closing costs and any lender specific fees tied to the chosen loan.

Website: https://lofirate.com

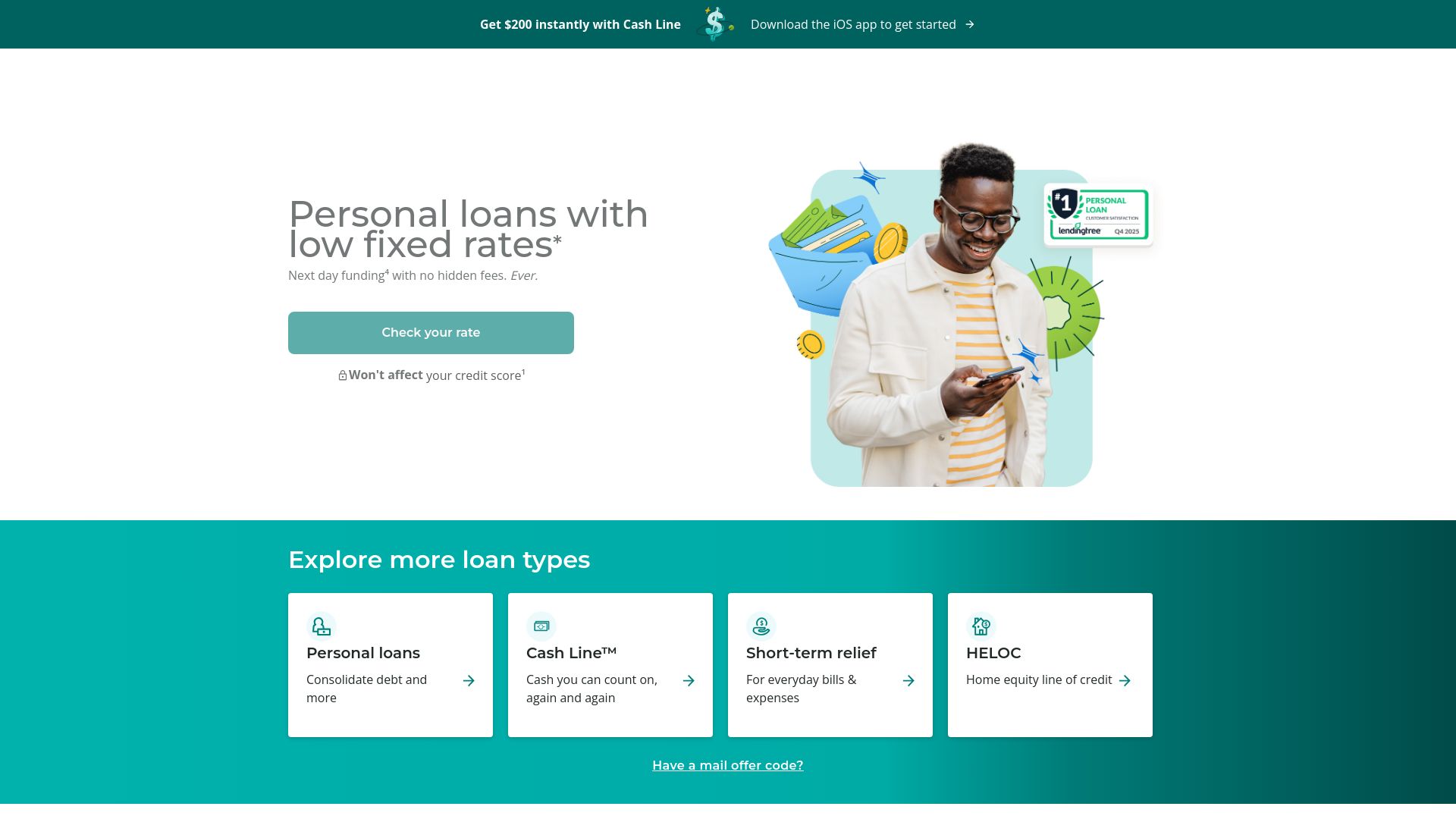

Upstart

At a Glance

Checking rates does not affect your credit score. Upstart automates approvals for personal loans up to $75,000 and offers a Cash Line™ credit product. The company advertises instant decisions and funding as soon as the next day in many cases.

Core Features

Personal loans carry fixed rates and aim for fast approval, and Cash Line™ provides an immediately accessible credit option with a $200 minimum limit. Home equity lines of credit range from $26,000 to $250,000, and short term relief loans cover small emergency needs from $200 to $2,500. The application flow emphasizes speed, with decisions and funding targets that move borrowers through underwriting quickly.

Key Differentiator

The main distinction is the ability to check rates without a hard credit pull. That lets you compare loan options without an immediate impact on your credit report. Automation and a rules driven underwriting flow help move approved borrowers to funding faster than many retail lenders.

Pros

Upstart's marketing materials state a 4.9/5 Trustpilot rating. The application is quick, and checking rates does not affect your credit score, which lowers friction when you shop for options. A mix of products covers common borrower needs, including fixed rate personal loans, a revolving Cash Line, HELOCs, and small emergency loans, and the platform advertises transparent fee language with no prepayment penalties.

Cons

-

Several product pages and links on the site are broken or missing, which makes detailed specs hard to find.

-

Public information on specific product restrictions and eligibility rules is limited, so precise qualification criteria are not always clear.

-

APRs vary by product and applicant qualification, and the site does not present fixed pricing details for every product in an easy to compare format.

Who It's For

Borrowers with moderate credit who need quick access to unsecured personal loans or a small revolving credit option will find Upstart relevant. It fits people focused on speed, transparent fees, and simple online applications rather than borrowers who need bespoke loan structures or deep offline underwriting. Homeowners seeking a HELOC are a secondary audience if they want an online application.

Real World Use Case

A borrower uses a personal loan to refinance high interest credit card balances. They check rates without a credit score impact, complete the online application, and accept a fixed rate offer that shortens payoff time. The borrower then uses the loan to lower monthly interest expense and pay down balances faster, with no prepayment penalty.

Pricing

Upstart's marketing materials report APRs from as low as 6.52% for HELOC to around 6.2% for personal loans, but actual rates depend on product, loan term, and applicant qualification. The vendor states that some applicants will see higher pricing based on creditworthiness. The site does not publish a single fixed price table for every product.

Website: https://upstart.com

MAMRAMIM

At a Glance

Built by mortgage professionals, MAMRAMIM pairs AI decision tools with a proprietary bidding engine. The marketplace runs real time competitive bids and supports anonymous negotiations among lenders, brokers, and note buyers. It focuses on U.S. mortgage and note transactions and uses role based workflows to move deals through matching and execution.

Core Features

A real time competitive bidding system handles offers and counteroffers while secure anonymous negotiation preserves confidentiality for sellers and buyers. Built in AI analyzes deal flow and provides decision support for pricing and risk assessment. The marketplace supports multiple participant roles, so brokers, lenders, and institutional investors each access tailored workflows.

Key Differentiator

The platform combines AI driven deal support with a proprietary bidding engine developed by mortgage professionals. That pairing gives market participants tools to surface competitive pricing and run simultaneous negotiations without exposing counterparty identities.

Pros

The marketplace was developed by industry specialists, which shows in workflows that match common broker and lender practices. Its anonymous negotiation and bid format increase transparency and reduce bargaining friction for sellers and buyers. By concentrating lending notes and investors in one venue, the platform can reduce transaction steps and cut intermediary time for many deal types.

Cons

-

Focused on the U.S. mortgage and note market, which limits usefulness for international sellers and buyers.

-

New users unfamiliar with electronic marketplaces face a learning curve before they can run bids effectively.

-

Liquidity depends on active participation, so thin markets may yield fewer competitive offers.

-

Regulatory and compliance details are not clearly documented in public storefront content.

When It May Not Fit

If you operate outside the United States, the platform will likely not meet your access needs. Small consumer lenders who prefer one on one retail channels may find the marketplace model awkward. If you lack basic note or servicing knowledge, the features will be harder to use and will deliver less value.

Who It's For

Mortgage brokers, lenders, note sellers, and note investors who want a focused venue for mortgage note transactions will benefit most. The platform fits professionals aiming to run anonymous auctions, test pricing, and access a concentrated pool of counterparties. Institutional buyers seeking portfolio diversification can also use the deal flow tools.

Real World Use Case

A mortgage broker signs up, uploads a pool of notes, and uses the AI tools to flag attractive lot pricing. The broker runs an anonymous bid session, receives multiple offers, and closes with a lender that matched price and risk appetite faster than a phone based process.

Pricing

Pricing details are not publicly specified. The platform operates on a membership or sign up basis with different participant types and access levels depending on whether you act as a broker, lender, seller, or investor.

Website: https://mamramim.com

AMP Mortgage

At a Glance

According to the company, AMP Mortgage can complete loan setup in 1 to 2 days and return initial underwriting in two days. That timeline extends to one day for document processing and one day for funding per the vendor. The lender targets nontraditional borrowers, including foreign nationals, ITIN applicants, and investors.

Core Features

AMP offers a wide set of loan products that include full documentation loans, bank statement programs, 1099 and profit and loss options, asset depletion, DSCR, foreign national financing, ITIN programs, and down payment assistance. The platform pairs these product types with rate sheets and appraisal management resources and publishes expected turn times to help broker partners plan closings. Advanced technology supports broker communication and status visibility during processing.

Key Differentiator

AMP’s main advantage is its combination of flexible, niche mortgage programs and fast operational rhythm. That emphasis on speed and specialized product mix helps brokers place loans for borrowers who do not fit conventional guidelines.

Pros

AMP covers borrowers who often struggle with retail channels, such as self employed clients, foreign nationals, and investors, which gives brokers more placement options. The company highlights rapid processing and predictable turn times. That timeline helps reduce closing friction when a borrower has limited documentation or an unusual income profile. AMP also supplies practical broker tools like rate sheets, appraisal coordination, and loan resources to support underwriting and disclosures.

Cons

- Public site pages are incomplete or broken, which makes researching product specifics slow and unreliable.

- Detailed pricing, fee schedules, and rate grids are not published on the site, complicating side-by-side comparisons.

- No visible integration or connectivity documentation is available, so loan delivery workflows may require manual steps.

When It May Not Fit

Brokers who need transparent, fully published pricing before engaging will find AMP’s public materials lacking. Teams that require automated integrations with their loan origination system will face uncertainty because integration details are not visible. Mortgage shops that rely on consumer-facing online rate shopping may prefer lenders with live, public rate engines.

Who It's For

Mortgage brokers and lending professionals who serve complex borrower profiles will benefit most. AMP fits firms that place nontraditional loans for self employed clients, international buyers, ITIN holders, and real estate investors seeking DSCR or asset depletion financing. Smaller broker shops needing a partner that accepts unusual documentation will also find value.

Real World Use Case

A broker working with a self employed borrower who cannot provide standard W2 income uses AMP to package a jumbo loan with bank statement or profit and loss documentation. Another broker places DSCR financing for a real estate investor who needs rental income treated differently than personal income.

Pricing

Pricing information is listed as not applicable, with the site presented for informational purposes only. The website does not publish public rate tables or detailed fee schedules, so brokers must contact AMP directly for pricing and lock instructions.

Website: https://amp.mortgage

Comparison of alternatives

For prospective homeowners in the United States, comparing effective mortgage broker platforms involves evaluating access, cost, and unique features. Each platform offers distinct advantages, and understanding the trade-offs helps determine the right choice for diverse borrowing needs and preferences.

Cost structure and transparency

LoFi Rate provides free access to an expansive network of mortgage brokers, allowing users to evaluate multiple offers without incurring platform-specific costs. Conversely, AMP Mortgage specializes in underwriting processes tailored to nontraditional profiles, yet lacks a user-friendly, publicly available fee structure. Upstart shines with unsecured personal loan offerings but may incur higher interest rates depending on individual qualifications.

Specialized audience services

While LoFi Rate simplifies comparison shopping for diverse loan types nationwide, MAMRAMIM caters exclusively to real-estate note professionals, offering distinct features like real-time bidding and anonymous negotiations. Upstart’s quick funding for small personal loans suits individuals in immediate need of cash advances.

Best fit

- Borrowers seeking competitive mortgage rate comparisons and nationwide broker access with a zero-cost platform will find LoFi Rate highly appealing.

- Users needing fast personal loan approval and transparent fee structures may consider Upstart for its simplicity and efficiency.

- Real estate professionals requiring detailed bidding mechanisms and a high-volume note marketplace will appreciate MAMRAMIM’s advanced capabilities.

Our pick

For borrowers prioritizing free, clear access to numerous competing mortgage broker offers, LoFi Rate delivers performance. Its emphasis on transparent matchmaking and expert assistance positions it as the primary choice for exploring financing options effectively. However, those needing quick turnaround on personal or emergency loans, or real estate professionals focused on large-scale investment portfolios, may find specific competitors more fitting for their needs.

Lofirate connects borrowers with licensed brokers who offer competitive mortgage options across the United States.

| Product Name | Core Feature | Key Differentiator | Pricing | Notable Limitation |

|---|---|---|---|---|

| Lofirate | Nationwide licensed broker network | Competing broker offers | Free to use | Relies on third-party brokers, varying experiences |

| Upstart | Personal loans, HELOCs, Cash Line | No hard credit check | From 6.2% APR | Limited access to specific product details |

| MAMRAMIM | Real-time competitive bidding | AI-driven deal support | Price not published | Limited to U.S. mortgage and note markets |

| AMP Mortgage | Niche loan products for complex borrower profiles | Fast processing timelines | Price not published | Public site lacks published pricing details and integration documentation |

How to Compare LoanLosAngeles.com Alternatives for Better Mortgage Rates

Finding the right loan can feel frustrating when faced with limited lender options and unclear pricing. Many borrowers want transparent access to multiple competitive offers without contacting multiple lenders individually. Lofirate solves this by connecting U.S. homeowners and prospective buyers with licensed wholesale mortgage brokers who shop several lenders at once. This approach helps avoid overpaying retail rates and provides valuable side-by-side comparisons of terms and costs.

Lofirate focuses on simplicity and consumer protection by matching you with brokers who offer no-obligation consultations and competitive mortgage pricing. Use Lofirate to receive multiple broker quotes quickly and decide which loan fits your financial goals and timeline. Visit Lofirate.com now to request your free broker match and get competing mortgage offers in your inbox.

FAQ

What are the key features of Lofirate?

Lofirate connects borrowers with licensed mortgage brokers nationwide without charging matchmaking fees. The platform enables users to access a wide range of mortgage products and presents quick rate comparisons alongside expert guidance.

How does Lofirate compare to Upstart?

Upstart automates approvals for personal loans and emphasizes speed, often offering instant decisions and funding. In contrast, Lofirate allows borrowers to receive competing broker offers from licensed mortgage brokers, making it a better fit for those specifically looking for mortgage solutions rather than personal loans.

Does Lofirate offer real-time rate comparisons?

Yes, Lofirate aggregates multiple licensed broker offers to show competing rates and terms side by side. This feature simplifies the shopping process for borrowers looking for the best mortgage deal based on their needs.

Who would benefit most from using Lofirate?

U.S. homeowners and prospective buyers who prefer an online mortgage shopping experience will find Lofirate useful. It caters especially to those who want multiple competing offers without the hassle of contacting various lenders directly.

Are there any fees associated with Lofirate?

Lofirate is free to use for borrowers, charging no matchmaking fees while borrowers only pay closing costs and any lender-specific fees associated with their chosen loan. This structure makes it an appealing option for cost-conscious users seeking mortgage options.