Many homebuyers and refinancers mistakenly believe that mortgage rates will return to the historic lows of 3% or 4% seen during the pandemic. The reality is starkly different: experts forecast rates to stabilize around the mid-6% range throughout 2026. Understanding these trends helps you make smarter decisions about buying or refinancing. This guide explains what drives mortgage rates, what forecasters predict, and how to secure the most competitive rates available in 2026.

Table of Contents

- How Mortgage Rates Are Determined: Key Drivers In 2026

- Expert Forecasts And Economic Factors Shaping 2026 Rates

- Common Misconceptions About Mortgage Rates In 2026

- Leveraging Wholesale Mortgage Brokers To Secure Competitive Rates

- Practical Implications For Homebuyers And Refinancers In 2026

- Explore Competitive Mortgage Options With LO FI RATE

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| 2026 rate expectations | Mortgage rates will remain stable around 6.0% to 6.4% throughout 2026 with limited downward movement. |

| Economic drivers | Federal Reserve policy pauses and 10-Year Treasury yields primarily determine mortgage rate levels. |

| Wholesale broker advantage | Wholesale mortgage brokers access multiple lenders, offering more competitive rates than retail banks. |

| Refinancing outlook | Refinancing activity expected to increase from 26% to 35% as rates modestly improve. |

| Affordability improvements | Income growth outpacing home price increases creates slightly better affordability conditions in 2026. |

How mortgage rates are determined: key drivers in 2026

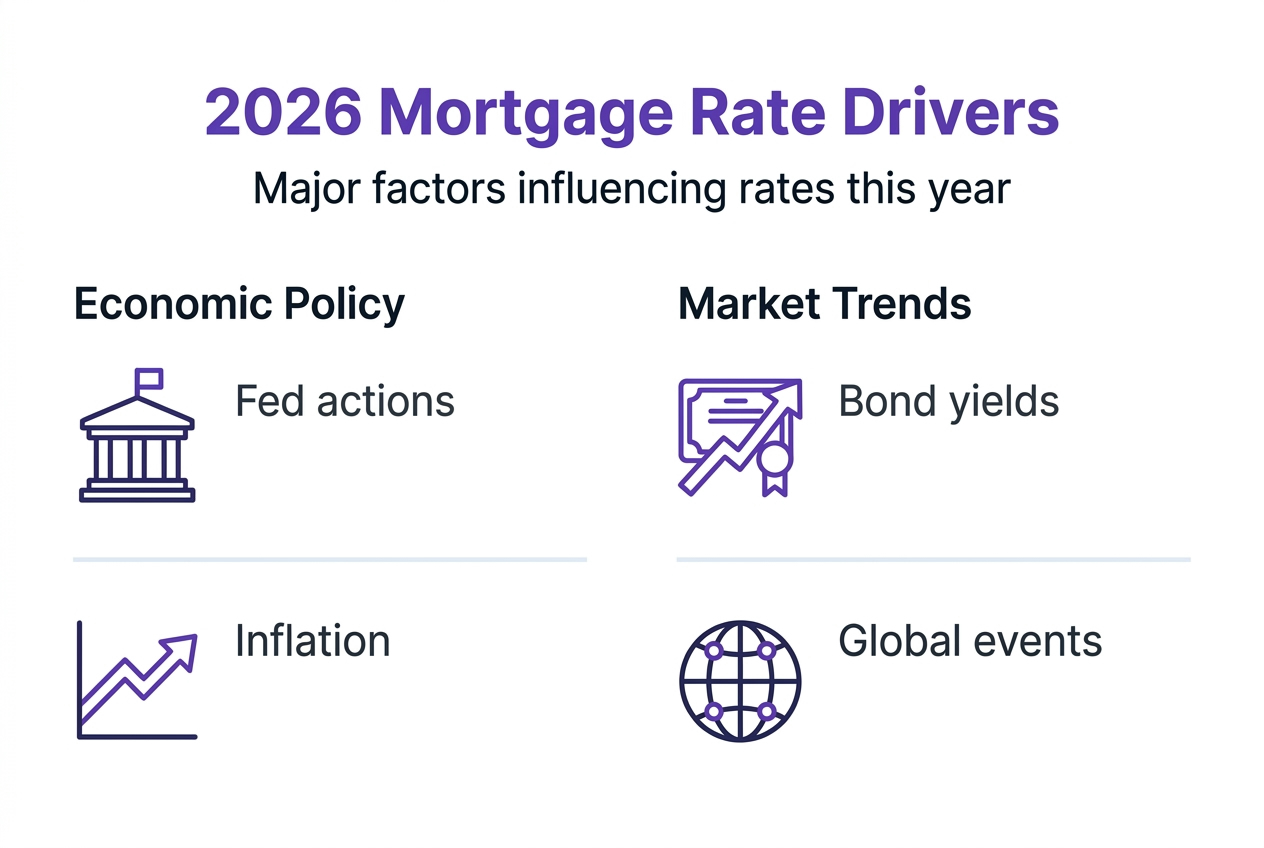

Mortgage rates don't move randomly. Several interconnected economic factors determine where rates settle each day. Understanding these drivers helps you anticipate rate changes and time your mortgage decisions more effectively.

The Federal Reserve influences short-term interest rates through monetary policy decisions, but it doesn't directly set mortgage rates. When the Fed raises or lowers its benchmark rate, it signals its economic outlook and inflation expectations. These signals ripple through financial markets and affect longer-term interest rates, including mortgages.

The 10-Year Treasury yield closely correlates with 30-year fixed mortgage rates. When investors buy Treasury bonds, yields fall; when they sell, yields rise. Mortgage lenders use these yields as a baseline and add a spread to cover their costs and risk. This connection explains why mortgage rates track Treasury movements so closely.

Inflation expectations play a massive role in bond market behavior. If investors anticipate rising inflation, they demand higher yields to compensate for reduced purchasing power. Employment data, GDP growth, and consumer spending all feed into these inflation expectations. Strong economic growth can paradoxically push mortgage rates higher as investors anticipate the Fed maintaining tighter policy.

Geopolitical events and economic uncertainties add volatility to rate movements. Trade tensions, international conflicts, or unexpected economic shocks cause investors to seek safe-haven assets like Treasury bonds, temporarily lowering yields and mortgage rates. The opposite happens when confidence returns.

Key factors influencing 2026 mortgage rates:

- Federal Reserve policy stance and forward guidance on interest rates

- 10-Year Treasury yield movements reflecting inflation and growth expectations

- Employment trends and wage growth affecting Fed policy decisions

- Global economic conditions and geopolitical stability

- Housing market supply and demand dynamics

Understanding these mechanisms lets you interpret economic news and anticipate potential rate shifts. You'll recognize when conditions favor locking in a rate versus waiting for potential improvements.

Expert forecasts and economic factors shaping 2026 rates

Mortgage rate predictions for 2026 cluster around a narrow band, but uncertainty remains. Most forecasters agree on a stable trajectory with modest volatility rather than dramatic swings.

Consensus estimates place 30-year fixed rates between 6.0% and 6.4% for most of 2026. This represents only slight improvement from late 2025 levels. The range reflects disagreement about inflation persistence, Federal Reserve actions, and economic growth strength. Some optimistic forecasts suggest brief dips toward 5.8%, while more cautious analysts warn rates could spike to 6.5% if inflation resurges.

The Federal Reserve paused rate cuts in early 2026, stabilizing mortgage rates around 6.18%. This pause reflects the Fed's assessment that inflation remains above its 2% target despite progress. The central bank wants more evidence of sustained inflation decline before resuming cuts. This cautious stance limits how far mortgage rates can fall in the near term.

Economic wildcards introduce forecast uncertainty. Potential recession risks, unexpected inflation spikes, or major geopolitical events could rapidly shift rate trajectories. The housing market itself adds complexity as low inventory and affordability challenges persist. Forecasters build these uncertainties into their models, creating the range of predictions you see.

| Source | 2026 Q1 Forecast | 2026 Q4 Forecast | Key Assumption |

|---|---|---|---|

| Fannie Mae | 6.3% | 6.1% | Modest Fed easing |

| Mortgage Bankers Association | 6.2% | 6.0% | Stable inflation |

| National Association of Realtors | 6.4% | 6.2% | Slow economic growth |

| Wells Fargo | 6.1% | 5.9% | Fed cuts resume |

Comparing multiple expert forecasts helps you understand the consensus view and the range of possibilities. No single forecast perfectly predicts the future, but the collective wisdom provides valuable guidance. Focus on the central tendency rather than outlier predictions when planning your mortgage timing.

Common misconceptions about mortgage rates in 2026

Several persistent myths about mortgage rates lead borrowers to make poor decisions. Clearing up these misconceptions helps you set realistic expectations and avoid costly timing mistakes.

Myth: Rates will drop below 4% again soon. Many buyers remember the pandemic era's rock-bottom rates and expect a return. The reality: rates will not dip below 4% in 2026, with mid-6% being the realistic expectation. Those historic lows required extraordinary economic circumstances including a pandemic, near-zero Fed rates, and massive bond-buying programs. None of these conditions exist in 2026.

Myth: The Federal Reserve directly controls mortgage rates. Many people believe the Fed sets all interest rates, including mortgages. In truth, the Fed influences the economy and short-term rates, but bond markets largely determine mortgage rates. The 10-Year Treasury yield matters far more for your mortgage rate than the Fed's overnight rate. Understanding this distinction helps you focus on the right economic indicators.

Myth: Waiting guarantees better rates. Some buyers perpetually wait for the "perfect" rate, missing opportunities as home prices rise. Rates could improve slightly in 2026, but they could also rise if inflation persists. Waiting costs you in lost equity and continued rent payments. The best rate is the one you can afford that lets you buy the home you need.

Myth: All lenders offer similar rates. Borrowers often assume rate shopping won't yield significant savings. Reality shows rate spreads of 0.5% or more between retail lenders and wholesale brokers. This difference translates to thousands of dollars over your loan's life.

Pro Tip: Track 10-Year Treasury yields and bond market movements instead of obsessing over Fed announcements. These indicators provide earlier signals of mortgage rate direction. Set rate alerts with multiple brokers to catch favorable windows quickly.

Armed with accurate information, you can make confident decisions based on market realities rather than wishful thinking. Focus on securing the best rate available today rather than chasing an unlikely dramatic drop.

Leveraging wholesale mortgage brokers to secure competitive rates

Wholesale mortgage brokers offer a powerful advantage over traditional retail lenders, especially in a stable rate environment like 2026. Understanding this difference can save you thousands.

Wholesale brokers connect borrowers with multiple lenders simultaneously. Instead of offering only their own mortgage products, they shop your application across dozens of wholesale lenders competing for your business. This competition naturally drives rates lower. You benefit from lender pricing wars without doing the legwork yourself.

Retail lenders like large banks offer only their proprietary products. You're limited to whatever rates that institution decides to offer that day. Even if a competitor has better pricing, you won't know unless you apply elsewhere. This lack of competition means higher rates and fewer options for rate buy-downs or loan customization.

The cost savings add up dramatically over time. A 0.25% rate difference on a $400,000 30-year mortgage equals roughly $60 monthly and over $21,000 in total interest. Wholesale brokers frequently beat retail rates by 0.25% to 0.5% or more. That's real money staying in your pocket.

Pro Tip: Request loan estimates from both a wholesale broker and a retail lender simultaneously. Compare not just the interest rate but also fees, closing costs, and terms. This parallel comparison reveals the true cost difference and negotiating leverage.

| Factor | Wholesale Broker | Retail Lender |

|---|---|---|

| Lender access | 20 to 50+ lenders | Single lender only |

| Rate competitiveness | Highly competitive through lender bidding | Set by institution policy |

| Loan options | Broad product variety | Limited to proprietary products |

| Flexibility | High; can match borrower needs precisely | Low; fits borrower into existing products |

| Potential savings | 0.25% to 0.5%+ lower rates typical | Standard retail pricing |

Accessing low mortgage finance rates through wholesale channels puts you in control. You're not locked into a single lender's pricing or products. Instead, you benefit from market competition working in your favor.

Wholesale brokers also provide expertise in navigating complex loan scenarios. If you're self-employed, have unique income sources, or need specialized loan options, brokers know which lenders handle these situations best. This matching expertise saves time and improves approval odds.

Practical implications for homebuyers and refinancers in 2026

Understanding mortgage rate trends means little without actionable strategies to apply that knowledge. Here's how to translate forecasts into smart decisions.

Refinancing activity is poised to surge as rates stabilize or dip slightly. Refinancing volume is forecast to rise to 35% of new mortgages in 2026, up from 26% in 2025. If you locked in a rate above 7% in 2023 or 2024, even a drop to 6.2% generates substantial savings. A 0.75% reduction on a $350,000 loan saves roughly $175 monthly, justifying refinancing costs within a year.

Home affordability improves modestly in 2026 as wage growth outpaces home price appreciation in many markets. While rates remain elevated compared to pandemic levels, stable income growth helps more buyers qualify. Median household incomes rising 3% to 4% annually while home prices grow 2% to 3% creates a slowly improving affordability picture.

Timing your rate lock requires monitoring multiple signals simultaneously. Watch Federal Reserve meeting minutes for policy clues, track 10-Year Treasury yields for immediate rate direction, and consult economic calendars for major data releases like jobs reports or inflation figures. These events trigger rate volatility, creating opportunities to lock favorable rates.

Consulting wholesale brokers streamlines the process of securing competitive offers. They monitor rate sheets from multiple lenders daily and alert you when favorable pricing appears. This proactive approach beats reactive rate shopping after you've already found a home and face closing deadlines.

Key action steps for 2026:

- Calculate your refinance breakeven point if your current rate exceeds 6.5%

- Get pre-approved through a wholesale broker to understand your true buying power

- Set rate alerts with your broker to catch temporary rate dips quickly

- Focus on total monthly payment including taxes and insurance, not just the rate

- Lock your rate when you find a home rather than gambling on further drops

- Compare multiple loan estimate documents to verify you're getting competitive pricing

The path to low mortgage finance rates in 2026 requires preparation and strategic timing. Rates won't drop dramatically, but small improvements combined with wholesale broker access create real savings opportunities. Act decisively when conditions align rather than waiting for the perfect scenario.

Explore competitive mortgage options with LO FI RATE

Navigating 2026's mortgage landscape requires access to competitive rates and expert guidance. LO FI RATE connects you with licensed wholesale mortgage brokers who shop multiple lenders on your behalf, securing rates that retail banks can't match.

Whether you're purchasing your first home or refinancing to lower your payment, wholesale access means more lender options competing for your business. This competition translates directly into lower rates and better loan terms. You benefit from broker expertise without sacrificing rate competitiveness.

The loan options available through wholesale channels cover every scenario. Fixed-rate mortgages, adjustable-rate products, government-backed loans, and specialized programs all compete for your business. Your broker matches your financial situation with the lenders most likely to offer optimal pricing.

Benefits of the LO FI RATE platform:

- Access to 30+ wholesale lenders shopping competitively for your loan

- Potential rate savings of 0.25% to 0.5% versus retail lenders

- Expert broker guidance through application, underwriting, and closing

- Transparent comparison of rates, fees, and terms across multiple offers

- Fast pre-approval process to strengthen your purchasing position

Apply now to see how much you can save with wholesale mortgage access. A quick consultation reveals your rate options and potential monthly payment, with no obligation to proceed. In a year when every 0.1% matters, wholesale access provides the edge you need.

Frequently asked questions

What are the expected average mortgage rates in 2026?

Experts forecast 30-year fixed mortgage rates averaging between 6.0% and 6.4% throughout 2026, with most estimates clustering around 6.2%. Rates should remain relatively stable with modest fluctuations based on economic data releases and Federal Reserve guidance. Brief dips toward 5.8% are possible if inflation cools faster than expected.

Will mortgage rates drop back to pre-pandemic lows in 2026?

No, mortgage rates will not return to the 3% to 4% range seen during 2020 and 2021. Those historic lows required emergency Federal Reserve interventions and a global pandemic. Current economic conditions including persistent inflation and normalized Fed policy mean rates will stabilize in the mid-6% range instead.

How does the Federal Reserve affect mortgage rates?

The Federal Reserve influences short-term interest rates and economic conditions but doesn't directly set mortgage rates. The 10-Year Treasury yield, driven by bond market investor behavior, correlates most closely with mortgage rates. Fed policy affects these yields indirectly through inflation expectations and economic growth signals.

Why should I consider a wholesale mortgage broker?

Wholesale brokers access multiple lenders simultaneously, creating competition that drives your rate lower. Retail lenders offer only their own products at prices they set. Brokers typically secure rates 0.25% to 0.5% lower than retail, saving thousands in interest over your loan term.

When is the best time to lock in a mortgage rate in 2026?

Lock your rate when you've found a home you want to purchase and current rates align with your budget. Monitor Federal Reserve announcements and 10-Year Treasury yields for short-term direction, but don't try to time the absolute bottom. Consult your broker when rates dip into favorable territory and lock decisively rather than gambling on further drops.