Refinancing your mortgage doesn't always lower your monthly payment. In fact, depending on your goals and loan terms, it might even increase it. Many homeowners miss this reality and overlook critical costs that can erase potential savings. This guide breaks down how home refinancing actually works, what it costs, and how licensed wholesale mortgage brokers help you access competitive rates and real savings that retail lenders often can't match.

Table of Contents

- What Is Home Refinance? Fundamentals And Purpose

- How Does Home Refinance Work? The Financial Mechanics

- Types Of Refinance Loans: Rate And Term Vs Cash Out

- The Role Of Wholesale Mortgage Brokers In Refinancing

- Common Misconceptions About Refinancing And Truths You Need To Know

- How To Evaluate If Refinancing Makes Financial Sense For You

- Practical Steps To Refinance Using Licensed Wholesale Mortgage Brokers

- Save More On Your Refinance With Lofirate

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| What refinance means | Replacing your current mortgage with a new loan to adjust rate, term, or access equity. |

| Costs and eligibility | Closing costs run 2% to 5% of loan amount; credit score, equity, and debt ratios determine approval. |

| Wholesale broker advantage | Licensed brokers shop multiple lenders for rates often 0.25% to 0.75% lower than retail. |

| Loan type differences | Rate and term refinance adjusts interest or term without tapping equity; cash out increases loan balance for lump sum funds. |

| Evaluation and application | Calculate break even period, compare offers from wholesale brokers, and apply with required documents. |

What is home refinance? Fundamentals and purpose

Refinancing replaces an existing mortgage with a new loan, giving you a fresh start with different terms. Most homeowners refinance to achieve one or more financial goals that improve their situation.

Common reasons to refinance include:

- Lowering your monthly payment by securing a lower interest rate

- Reducing your loan term to pay off the mortgage faster and save on total interest

- Accessing home equity for major expenses like renovations or debt consolidation

- Switching from an adjustable rate to a fixed rate for payment stability

Refinancing can reduce your monthly payment by 10% to 30% depending on current rates and your original loan terms. The impact extends beyond monthly cash flow. A lower rate or shorter term can save you tens of thousands in interest over the life of the loan.

It's not just about saving money. Refinancing lets you adjust your mortgage to match your current financial needs and long term goals. Whether you want to free up monthly budget or build equity faster, refinancing gives you control over your mortgage structure.

Pro Tip: Before refinancing, check mortgage refinancing basics to understand how new loan terms affect your total interest and payment schedule.

How does home refinance work? The financial mechanics

Refinancing follows a process similar to your original mortgage application but focuses on replacing existing debt. Understanding eligibility and costs upfront prevents surprises and bad timing.

Eligibility depends on three key factors:

- Credit score: Most lenders require at least 620, with better rates available at 740 or higher

- Debt to income ratio: Lenders prefer total monthly debts below 43% of gross income

- Home equity: You typically need at least 20% equity to qualify for the best rates and avoid private mortgage insurance

Refinancing costs typically range from 2% to 5% of the loan amount. These include appraisal fees, origination charges, title insurance, and closing costs. On a $300,000 refinance, expect to pay $6,000 to $15,000 upfront.

The break even period shows when your monthly savings offset refinancing costs. If refinancing saves you $200 per month and costs $8,000, your break even point is 40 months. You need to stay in the home beyond that timeline to realize net savings.

Refinancing temporarily impacts your credit score due to hard inquiries and the new loan account. Expect a 5 to 10 point dip that recovers within a few months as you make on time payments.

Pro Tip: Calculate your break even period before committing. If you plan to move within a few years, refinance costs explained may outweigh potential savings, making refinancing a poor financial choice.

Explore different loan options to find terms that align with your timeline and budget.

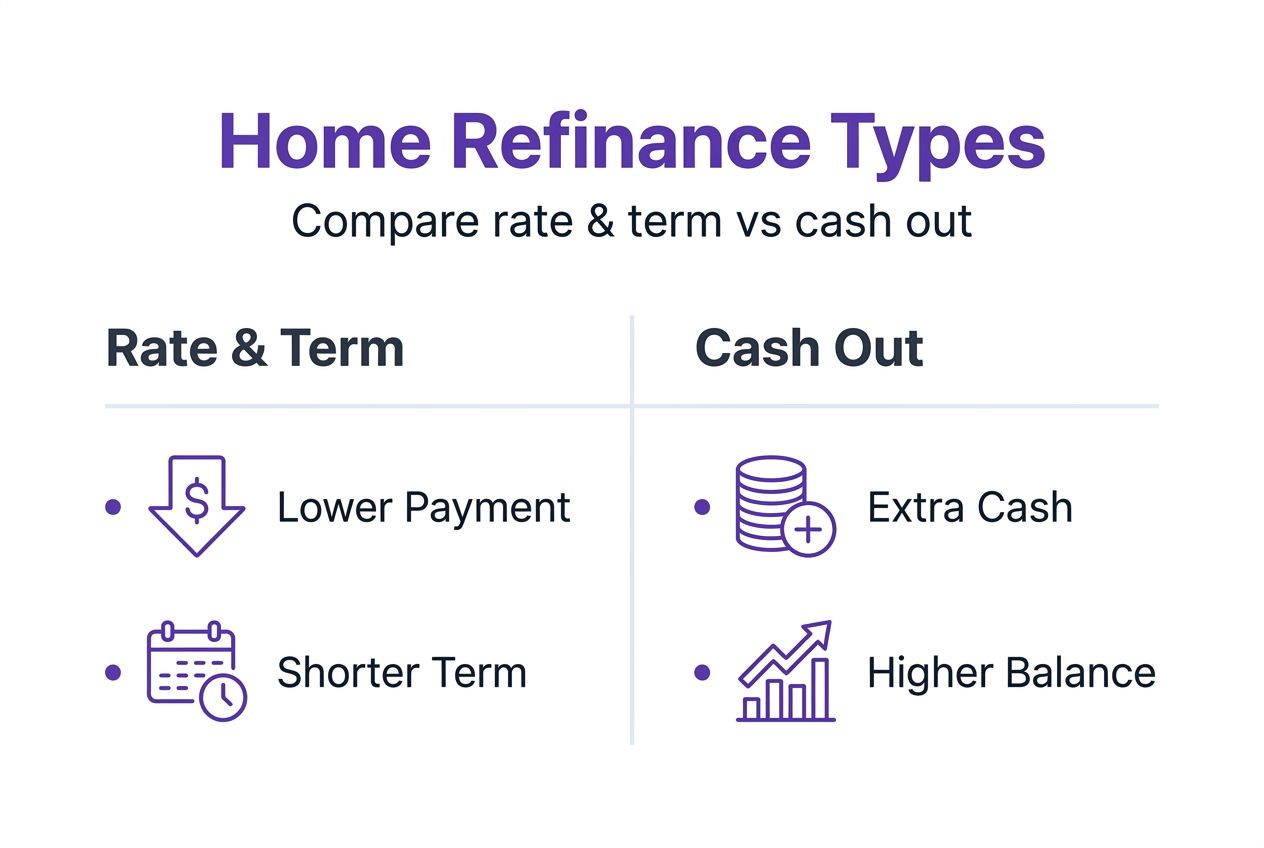

Types of refinance loans: rate and term vs cash out

Refinance products fall into two main categories, each serving distinct financial goals. Choosing the wrong type can cost you money or fail to meet your needs.

Rate and term refinance replaces your existing loan with a new one at a different interest rate or loan term without increasing the principal balance. You might lower your rate to reduce monthly payments or shorten your term from 30 years to 15 years to build equity faster and pay less total interest.

Cash out refinance increases your loan balance above what you currently owe, giving you a lump sum of cash from your home equity. You might use this for home improvements, debt consolidation, or other major expenses. Because you're borrowing more, your monthly payment usually increases even if you secure a lower rate.

| Feature | Rate and Term Refinance | Cash Out Refinance |

|---|---|---|

| Loan balance | Stays the same or decreases | Increases above current balance |

| Monthly payment | Typically decreases | Often increases |

| Best for | Lowering rate or shortening term | Accessing equity for expenses |

| Equity requirement | At least 20% recommended | At least 20% must remain after cash out |

| Interest rate | Usually lower | Slightly higher due to increased risk |

Key considerations:

- Rate and term refinance works best when current rates are significantly lower than your existing rate or when you want to pay off your mortgage faster

- Cash out refinance suits homeowners needing funds for large expenses but increases debt and extends payoff timeline

- Both options require closing costs, so evaluate whether the benefit justifies the expense

Understanding these tradeoffs helps you select the right product for your financial situation. Review available loan options to compare terms and costs.

The role of wholesale mortgage brokers in refinancing

Licensed wholesale mortgage brokers offer a distinct advantage over retail lenders by shopping your loan across multiple wholesale lenders. This competition typically results in better rates and more flexible terms.

Wholesale brokers work differently than retail lenders:

- Retail lenders offer only their own loan products at their own pricing

- Wholesale brokers access wholesale rate sheets from dozens of lenders, creating competition for your business

- Brokers earn compensation from lenders, not from marking up your rate beyond the wholesale price

Brokers often secure rates 0.25% to 0.75% lower than retail lenders can offer. On a $300,000 mortgage, a 0.5% rate reduction saves you roughly $90 per month or $32,400 over 30 years.

Benefits of using wholesale brokers:

- Access to multiple lenders means better odds of approval if one lender declines

- Transparent pricing with less markup compared to retail channels

- Personalized service from licensed professionals who guide you through options

- Time savings because brokers handle shopping and paperwork coordination

Licensed wholesale brokers simplify the refinance process by doing the lender comparison work for you, ensuring you don't overpay or miss better options hidden in the market.

Pro Tip: Platforms like LoFiRate connect you with licensed wholesale brokers who shop low mortgage finance rates across multiple lenders, maximizing your savings potential without the hassle of contacting lenders individually.

Common misconceptions about refinancing and truths you need to know

Many homeowners hold assumptions about refinancing that lead to poor decisions or missed opportunities. Clearing up these myths helps you approach refinancing with realistic expectations.

-

Misconception: Refinancing always lowers your monthly payment. Truth: If you cash out equity or extend your loan term, your payment may increase even with a lower rate.

-

Misconception: Refinancing has no impact on your credit score. Truth: Hard inquiries and opening a new loan account cause a temporary 5 to 10 point dip, which recovers quickly with on time payments.

-

Misconception: Any rate reduction justifies refinancing. Truth: Small rate differences may not offset closing costs. A 0.25% rate drop on a short timeline rarely makes financial sense.

-

Misconception: Closing costs are negligible. Truth: Costs run 2% to 5% of the loan amount, meaning $6,000 to $15,000 on a $300,000 refinance. Ignoring these upfront expenses leads to false assumptions about immediate savings.

-

Misconception: All lenders offer the same rates. Truth: Retail lenders markup rates significantly compared to wholesale brokers who shop multiple lenders for competitive pricing.

-

Misconception: You can refinance anytime without consequence. Truth: Refinancing too soon after your original mortgage or previous refinance can trigger prepayment penalties or fail to meet lender seasoning requirements.

Understanding these truths empowers you to evaluate refinancing based on facts, not assumptions, and avoid costly mistakes.

How to evaluate if refinancing makes financial sense for you

Deciding whether to refinance requires analyzing your specific situation against objective criteria. A systematic evaluation prevents emotional decisions and ensures net financial benefit.

Calculate your break even period: Divide total closing costs by monthly savings. If refinancing costs $9,000 and saves $250 per month, your break even point is 36 months. You must stay in the home longer than that to profit.

Assess your eligibility: Check your credit score, current home equity, and debt to income ratio against lender requirements. A score below 620 or equity under 20% may limit your options or result in higher rates that negate savings.

Define your goals clearly:

- Do you want lower monthly payments for better cash flow?

- Are you aiming to pay off the mortgage faster and reduce total interest?

- Do you need cash for expenses like renovations or debt consolidation?

Compare multiple loan offers: Work with wholesale brokers who shop rates across lenders. A 0.25% difference in rate can mean thousands in savings over the loan life.

Run the numbers: Calculate total interest paid over the life of both your current loan and the proposed refinance. Factor in closing costs. If the new loan saves less than $5,000 over your planned ownership period, refinancing may not be worth the effort.

Pro Tip: Avoid refinancing without a clear net financial benefit. Review refinance cost benefit analysis techniques and explore loan options that match your timeline and goals before committing.

Practical steps to refinance using licensed wholesale mortgage brokers

Once you've decided refinancing makes financial sense, follow these steps to navigate the process efficiently and secure the best terms.

-

Contact licensed wholesale mortgage brokers: Use platforms like LoFiRate to connect with licensed brokers in your state who access multiple lenders for competitive rate shopping.

-

Gather required documents: Prepare recent pay stubs, tax returns, bank statements, credit reports, current mortgage statement, and property information including recent appraisal or tax assessment.

-

Shop multiple refinance offers: Request loan estimates from at least three brokers or lenders. Compare interest rates, closing costs, loan terms, and total cost over the life of the loan.

-

Select the best loan product: Choose the refinance option that aligns with your goals, whether that's a rate and term refinance for lower payments or a cash out refinance for accessing equity. Ensure the break even period fits your timeline.

-

Complete the application: Submit your application with all required documentation. Expect the lender to order an appraisal and verify employment and income.

-

Review and sign closing documents: Carefully read the loan estimate and closing disclosure. Verify the interest rate, monthly payment, closing costs, and loan terms match what you agreed to.

-

Close the loan and track improvements: After closing, monitor your credit score recovery and confirm your new monthly payment fits your budget. Track your break even date to measure when refinancing delivers net savings.

Ready to start? Apply for refinance through licensed wholesale brokers who can help you access competitive rates and loan terms tailored to your situation.

Save more on your refinance with LoFiRate

Refinancing your mortgage can unlock significant savings, but only if you access competitive rates from multiple lenders. LoFiRate connects you with licensed wholesale mortgage brokers who shop dozens of lenders to find the best refinance terms for your situation.

Instead of accepting retail pricing from a single lender, wholesale brokers give you access to low mortgage finance rates that could save you thousands over the life of your loan. Whether you want to lower your monthly payment, shorten your loan term, or tap into home equity, LoFiRate helps you explore flexible loan options suited to your refinancing goals. The process is simple, transparent, and designed to help you avoid overpaying.

Start your refinance journey today by visiting LoFiRate to apply for refinance and connect with licensed brokers who work for you, not the lender.

Frequently asked questions

What are the eligibility requirements for refinancing a mortgage?

You typically need a credit score of at least 620, though better rates require 740 or higher. Lenders also look for a debt to income ratio below 43% and at least 20% home equity to avoid private mortgage insurance and secure the best terms.

How does refinancing affect my credit score?

Refinancing causes a temporary 5 to 10 point drop in your credit score due to hard inquiries and opening a new loan account. Your score usually recovers within a few months as you make on time payments on the new mortgage.

How do I know if refinancing is worth it for my situation?

Calculate your break even period by dividing total closing costs by monthly savings. If you plan to stay in the home longer than the break even point and the total interest savings exceed costs, refinancing makes financial sense. Factor in your goals like lower payments or faster payoff.

What is the difference between wholesale and retail mortgage brokers?

Retail lenders offer only their own loan products at their own pricing. Wholesale brokers access rate sheets from multiple lenders, creating competition that typically results in rates 0.25% to 0.75% lower than retail. Brokers shop for the best deal on your behalf.

How should I prepare to choose the right refinance loan?

Define your goals clearly, whether lowering monthly payments, shortening loan term, or accessing equity. Gather financial documents including pay stubs, tax returns, and credit reports. Shop offers from at least three wholesale brokers to compare rates, terms, and total costs before deciding.