TL;DR:

- Choosing the right mortgage insurance depends on assessing total costs over your ownership period and understanding cancellation rules.

- Proactively cancel PMI at 80% LTV, while FHA MIP lasts for 11 years or the full loan term, often making conventional loans more cost-efficient long-term.

Mortgage insurance is a lender protection policy that borrowers pay when their down payment falls below 20% of the home's purchase price. Knowing how to evaluate mortgage insurance options separates buyers who overpay for years from those who minimize costs and cancel coverage at the earliest legal opportunity. The three primary types — borrower-paid PMI, FHA mortgage insurance premium (MIP), and lender-paid mortgage insurance (LPMI) — differ significantly in cost structure, duration, and cancellation rules. Getting this decision right can save you thousands of dollars over your ownership period.

How to evaluate mortgage insurance options: types and key differences

The first step in any mortgage insurance comparison is understanding what you are actually buying. Each type protects the lender, not you, but each one costs you money in a different way and for a different length of time.

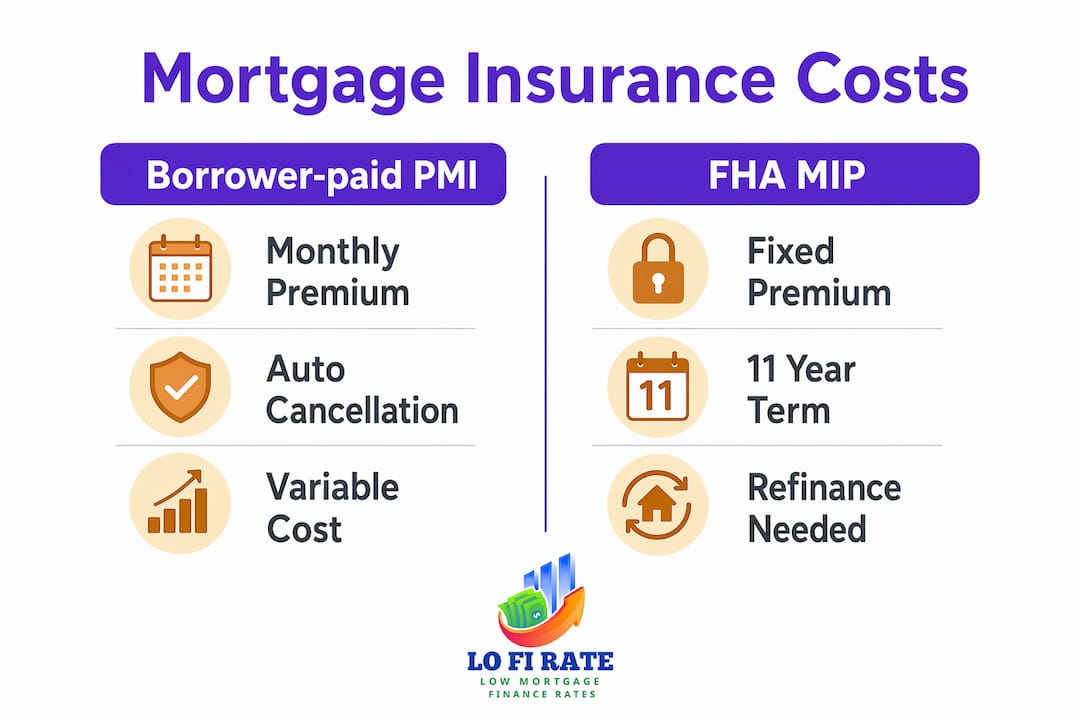

| Insurance Type | Payment Structure | Cancellation Path |

|---|---|---|

| Borrower-paid PMI | Monthly premium added to mortgage payment | Borrower request at 80% LTV; automatic at 78% LTV |

| FHA MIP | Upfront premium + annual premium paid monthly | 11 years (if original LTV ≤ 90%) or full loan life |

| Lender-paid (LPMI) | Built into a higher interest rate | No cancellation; requires refinancing |

Borrower-paid PMI is the most common option for conventional loans. PMI is canceled automatically at 78% loan-to-value (LTV) based on the original amortization schedule, or earlier if you submit a formal cancellation request at 80% LTV with supporting documentation. This flexibility makes it the most adaptable option for buyers who plan to stay in their home long enough to build equity.

FHA MIP works differently. Post-2013 FHA loans carry MIP for 11 years when the original LTV is 90% or below, and for the full life of the loan when the original LTV exceeds 90%. That means a buyer putting 3.5% down on an FHA loan will pay MIP for the entire 30-year term unless they refinance. FHA loans remain accessible for buyers with lower credit scores, but the long MIP duration is a real cost that demands careful evaluation.

LPMI removes the monthly insurance line item entirely. LPMI typically raises your interest rate by 0.125% to 0.375% for the life of the loan. That rate increase is permanent and cannot be canceled the way borrower-paid PMI can. For buyers focused on keeping monthly payments low in the short term, LPMI looks attractive. For anyone planning to own the home for more than five to seven years, the accumulated interest cost usually exceeds what borrower-paid PMI would have cost.

How to compare mortgage insurance costs and duration

Comparing initial monthly premiums is the wrong way to evaluate mortgage insurance. Total MI cost over your expected holding period is the number that actually matters. Two borrowers with identical monthly premiums can pay dramatically different totals depending on which type of insurance they carry and how long it lasts.

Use this framework to calculate your real cost:

| Scenario | 5-Year Total MI Cost | 10-Year Total MI Cost | Notes |

|---|---|---|---|

| Borrower-paid PMI (canceled at year 7) | Moderate | Ends before year 10 | Requires proactive cancellation request |

| FHA MIP (LTV > 90% at origination) | Moderate | High | Continues full loan life without refinancing |

| LPMI (rate increase 0.25%) | Low visible cost | High hidden cost | Rate premium accumulates indefinitely |

Your credit score, loan type, and down payment percentage all affect what you pay. A borrower with a 760 credit score putting 10% down on a conventional loan will pay lower PMI premiums than a borrower with a 680 score at the same down payment. FHA MIP rates are standardized and do not vary by credit score, which is one reason FHA loans attract borrowers with less-than-perfect credit.

Pro Tip: Build a simple spreadsheet with three columns: monthly MI cost, expected cancellation month, and total MI paid. Run this for each loan scenario you receive. The column that matters most is total MI paid, not the monthly figure.

Extra principal payments do not automatically accelerate your PMI cancellation date. Automatic PMI termination is tied to the original amortization schedule, not to how fast you actually pay down the loan. If you make extra payments and reach 80% LTV ahead of schedule, you must actively request cancellation with documentation. That one action can save you eight to fourteen months of unnecessary premiums.

What practical steps help you compare mortgage insurance accurately?

Accurate evaluation requires gathering real numbers from real loan offers, not estimates. Follow these steps to build a reliable comparison.

-

Request at least three loan estimates. Each estimate must disclose the MI payment method (monthly, upfront lump sum, or split premium). Reviewing mortgage insurance payment structures across multiple offers reveals how much flexibility you actually have.

-

Calculate your current and projected LTV. Divide your loan balance by the home's original purchase price. Track when you will hit 80% and 78% LTV on each loan's amortization schedule. This tells you exactly when cancellation becomes possible and automatic.

-

Ask each lender about their cancellation process. Some servicers require a formal written request, a current appraisal, and proof of on-time payments for the prior 12 months. Knowing the process upfront prevents delays when you are eligible. A list of questions to ask mortgage brokers about insurance terms is a useful starting point.

-

Factor in your expected ownership duration. If you plan to sell or refinance within three years, LPMI's lower monthly payment may make sense. If you plan to stay ten or more years, borrower-paid PMI with proactive cancellation almost always costs less. Borrower-paid PMI is financially advantageous for long-term owners compared to lender-paid alternatives.

-

Account for FHA refinancing costs. If you are evaluating an FHA loan and your original LTV exceeds 90%, plan for the possibility of refinancing into a conventional loan once you reach sufficient equity. Refinancing an FHA loan into a conventional product is often the only practical path to eliminating MIP early.

Pro Tip: When comparing a conventional loan with PMI against an FHA loan, add the total expected MIP to the FHA loan's total interest cost before deciding. The lower FHA rate does not always offset the longer insurance duration.

What common mistakes should you avoid when evaluating mortgage insurance?

Most borrowers make at least one of these errors. Each one costs real money.

-

Assuming equity alone cancels PMI. Reaching 20% equity does not trigger automatic cancellation. Delaying a formal PMI cancellation request can cost $900 to $2,400 in unnecessary premiums. Submit the written request as soon as you hit 80% LTV.

-

Treating FHA MIP like conventional PMI. FHA MIP cannot be canceled by reaching 20% equity. Under post-2013 rules, the annual MIP lasts 11 years or the full loan life. Expecting FHA MIP to behave like PMI leads to serious underestimation of total insurance costs.

-

Ignoring the LPMI interest rate tradeoff. LPMI looks cheap on a monthly basis. Over a 15-year or 30-year hold, the rate premium compounds into a cost that far exceeds what borrower-paid PMI would have totaled. Always calculate the full interest cost difference, not just the monthly payment difference.

-

Forgetting that extra payments do not move the automatic termination date. Automatic PMI termination is based on the original amortization schedule. Extra principal payments build equity faster, but they do not change the scheduled termination date. You must request early cancellation to benefit from those extra payments.

-

Overlooking appraisal and documentation costs. Some servicers require a new appraisal to confirm current property value before approving a cancellation request. Budget $300 to $600 for this cost when planning your cancellation timeline. It is still far cheaper than months of unnecessary premiums.

Key takeaways

Evaluating mortgage insurance options requires comparing total MI cost over your ownership period, not just monthly premiums, because cancellation rules and duration vary sharply across PMI, FHA MIP, and LPMI.

| Point | Details |

|---|---|

| PMI cancellation requires action | Submit a written request at 80% LTV; automatic termination only occurs at 78% LTV. |

| FHA MIP duration is fixed at origination | MIP lasts 11 years or loan life based on original LTV; equity alone cannot cancel it. |

| LPMI costs more long-term | A permanent rate increase accumulates more total cost than borrower-paid PMI for long-term owners. |

| Total cost beats monthly premium | Calculate expected MI payments over 5, 10, and 15 years to compare options accurately. |

| Extra payments need a cancellation request | Prepaying principal builds equity but does not move the automatic PMI termination date forward. |

What I have learned from watching borrowers choose the wrong insurance type

Most borrowers focus on the monthly payment when they should be focused on the exit. The question is not "how much does mortgage insurance cost per month?" The real question is "how long will I be paying this, and what does it take to stop?"

I have seen buyers choose FHA loans for the lower down payment requirement without fully pricing in the MIP duration. When the original LTV exceeds 90%, that insurance runs for the life of the loan. A buyer who puts 3.5% down and stays in the home for 15 years can pay tens of thousands in MIP that a conventional borrower with PMI would have canceled years earlier. The FHA loan is not a bad product. It is a product that demands a clear-eyed assessment of total insurance cost, not just the monthly number.

LPMI is the other trap I see regularly. The pitch is simple: no monthly MI payment, lower payment overall. What gets buried is the rate increase. That 0.25% rate premium on a $400,000 loan adds up to real money over a decade. And unlike PMI, you cannot cancel it. You are locked in until you refinance, which costs money too.

My honest recommendation is this: if you plan to own the home for more than five years and qualify for a conventional loan, borrower-paid PMI with a proactive cancellation plan almost always wins. Build the cancellation request into your calendar the day you close. Know your servicer's requirements. Get the appraisal done when you are ready. That discipline turns mortgage insurance from a long-term cost into a short-term one.

— LoFi

Find the right mortgage insurance structure with Lofirate

Choosing between PMI, FHA MIP, and LPMI is easier when you can compare real loan offers side by side. Lofirate connects you with licensed wholesale mortgage brokers who shop multiple lenders to find competitive pricing across all three insurance structures.

Wholesale brokers have access to loan options that retail lenders do not offer directly, which means you get a broader view of what your mortgage insurance costs could actually be. Whether you are buying your first home or refinancing to remove FHA MIP, a no-obligation consultation through Lofirate's broker matching gives you the data you need to make a confident decision. Explore your loan options at Lofirate and request a second opinion before you commit to any single lender's offer.

FAQ

What is the difference between PMI and FHA MIP?

PMI applies to conventional loans and can be canceled when you reach 80% LTV with a formal request or automatically at 78% LTV. FHA MIP applies to FHA loans and lasts 11 years or the full loan life depending on your original LTV, with no equity-based cancellation option.

Can I cancel mortgage insurance early by making extra payments?

Extra principal payments build equity faster but do not move the automatic PMI termination date, which is tied to the original amortization schedule. To benefit from extra payments, you must submit a formal cancellation request to your servicer once you reach 80% LTV.

When does LPMI make financial sense?

LPMI makes the most sense for borrowers who plan to sell or refinance within three to five years, since the higher interest rate has less time to accumulate. For long-term owners, borrower-paid PMI with proactive cancellation is typically the lower-cost option.

How do I remove FHA mortgage insurance?

Under post-2013 FHA rules, the only reliable way to eliminate MIP early is to refinance into a conventional loan once you have sufficient equity and meet credit qualification requirements. Reaching 20% equity on an FHA loan does not trigger cancellation on its own.

What questions should I ask lenders about mortgage insurance?

Ask each lender to disclose the MI payment method, the estimated cancellation date, the servicer's cancellation process and documentation requirements, and the total MI cost over your expected ownership period. Comparing these answers across at least three loan estimates gives you the clearest picture of your true costs.