TL;DR:

- The interest rate reflects the yearly cost of borrowing the loan principal, while APR represents the total annual cost including fees and closing costs. Understanding the difference helps mortgage shoppers avoid choosing loans that appear cheaper but cost more over time. Comparing both metrics is essential for making informed decisions and finding the most cost-effective mortgage.

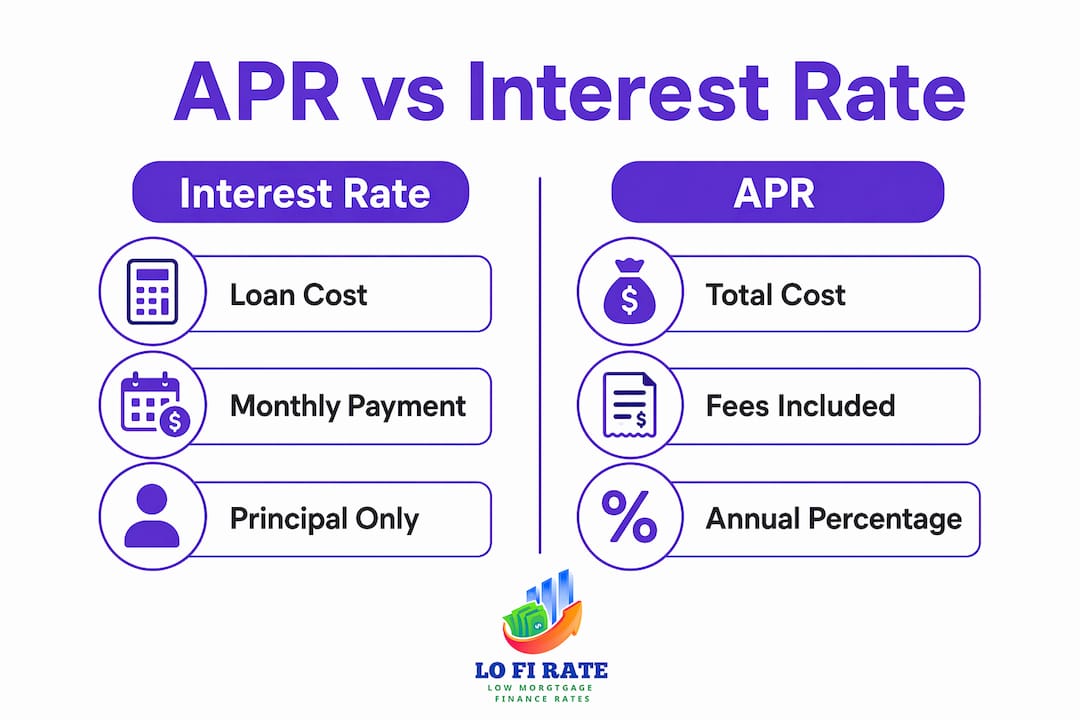

The difference between APR and interest rate is this: the interest rate reflects only the yearly cost of borrowing the loan principal, while APR represents the total annual cost of borrowing, including that interest rate plus lender fees and certain closing costs. For mortgage shoppers, confusing the two can lead to choosing a loan that looks cheaper on the surface but costs thousands more over time. Both numbers appear on every loan estimate, and both tell you something different. Understanding what each one measures is the first step toward comparing mortgage offers with confidence.

What is the difference between APR and interest rate?

The interest rate and APR measure two different things, even though lenders often display them side by side. The interest rate is a percentage applied to your loan principal. It determines how much interest you pay each month. The APR, or Annual Percentage Rate, wraps that interest rate together with lender fees, discount points, and certain closing costs into a single annual figure.

Here is a simple way to think about it. Imagine two lenders both offer you a 6.5% interest rate on a 30-year mortgage. Lender A charges $3,000 in origination fees. Lender B charges $800. Their interest rates look identical, but their APRs will differ because APR captures those fees. Lender A's APR will be noticeably higher, revealing the true cost gap between the two offers.

Federal law requires APR disclosure so that consumers understand the full cost of borrowing beyond the advertised interest rate. This regulation exists precisely because lenders could otherwise compete purely on headline rates while burying costs in fees. APR is the corrective lens that brings those hidden costs into focus.

One more important distinction: if a loan carries zero fees, the APR and interest rate will be identical. The gap between the two tells you exactly how much in fees the lender is rolling into the loan cost. That gap is a negotiating tool.

How does the interest rate affect your mortgage payment?

The interest rate is the number that directly controls your monthly payment size. Interest rate determines the cost of borrowed principal over time, and every monthly payment you make combines principal repayment with interest charges. A lower interest rate means a lower monthly payment, which affects your budget from day one.

Lenders set your interest rate based on several factors:

- Credit score: Higher scores typically earn lower rates because they signal lower default risk.

- Loan type: Conventional, FHA, VA, and USDA loans each carry different rate structures.

- Loan term: A 15-year mortgage usually carries a lower rate than a 30-year mortgage.

- Market conditions: The Federal Reserve's benchmark rate and bond market movements push mortgage rates up or down across the industry.

- Down payment size: Larger down payments reduce lender risk and can lower your rate.

Fixed vs. variable interest rates

A fixed interest rate stays the same for the entire loan term. Your payment is predictable, which makes budgeting straightforward. An adjustable-rate mortgage, or ARM, starts with a fixed rate for an initial period (commonly 5 or 7 years) and then adjusts periodically based on a market index. ARMs can start lower than fixed rates, but they carry the risk of rising payments later. Knowing which type you are comparing matters when you look at both the interest rate and APR side by side. You can explore how these loan structures compare in this types of mortgage loans guide.

Pro Tip: When comparing fixed and adjustable mortgages, ask lenders to show you the worst-case payment scenario on an ARM. That number, combined with the APR, gives you a realistic picture of long-term cost.

What does APR include and why does it matter?

APR is a standardized metric that all lenders must calculate using federal rules. This standardization is what makes it useful for apples-to-apples comparisons of total borrowing costs across different lenders and loan products. Without it, comparing mortgage offers would require manually adding up every fee from every lender.

The fees typically included in APR for a mortgage are:

- Origination fees: Charged by the lender for processing the loan.

- Discount points: Prepaid interest you pay upfront to buy down your interest rate.

- Mortgage broker fees: Compensation paid to the broker arranging the loan.

- Certain closing costs: Including underwriting fees and processing charges.

Costs generally not included in APR are title insurance, appraisal fees, and prepaid homeowners insurance. Understanding which fees fall inside and outside APR helps you read a loan estimate accurately. For a full breakdown of what shows up where, this mortgage fees guide is worth reviewing.

Closing costs and discount points are included in the APR calculation but not in the interest rate, which is why APR is almost always higher than the stated interest rate on a mortgage. The wider that gap, the more fees the lender is charging. A narrow gap suggests a lean fee structure.

It is also worth noting that on credit cards, APR and interest rate are often the same because credit cards rarely carry separate upfront fees rolled into APR. Mortgages are different. The fee structures are larger and more varied, which is why the APR gap matters far more on a home loan than on a credit card.

Pro Tip: Ask every lender for a Loan Estimate form. Federal law requires lenders to provide this document within three business days of your application. It shows both the interest rate and APR in a standardized format, making direct comparison straightforward.

| Feature | Interest rate | APR |

|---|---|---|

| What it measures | Cost of borrowing principal | Total annual cost including fees |

| Includes lender fees | No | Yes |

| Affects monthly payment | Yes | No (used for comparison only) |

| Regulated by federal law | No | Yes |

| Typically higher number | No | Yes |

When does the APR vs. interest rate gap matter most?

The gap between APR and interest rate matters most when you are comparing loans with different fee structures or when your plans for the property affect how long you will hold the loan.

-

You plan to sell or refinance within 3–5 years. The APR calculation assumes you hold the loan for its full term. If you pay off the loan early, you may not recoup the upfront fees built into a low-rate, high-fee loan. In that scenario, a loan with a slightly higher interest rate but lower fees can cost less overall.

-

You are comparing loans with discount points. Discount points are prepaid interest that reduce your interest rate and lower monthly payments over time. Paying one point typically costs 1% of the loan amount. If you stay in the home long enough, the monthly savings outweigh the upfront cost. If you sell early, you lose that investment. APR reflects the cost of points, so a loan with points will show a smaller APR-to-interest-rate gap than you might expect.

-

You are choosing between lenders with very different fee structures. Two lenders can offer the same interest rate with APRs that differ by 0.3% or more. That difference represents real money. On a $400,000 loan, even a small APR difference compounds significantly over 30 years.

-

You are evaluating a no-closing-cost mortgage. These loans roll fees into the interest rate rather than charging them upfront. The interest rate will be higher, but the APR gap will be narrower. They can make sense if you plan to refinance within a few years.

Pro Tip: Calculate your break-even point on discount points. Divide the upfront cost of the points by the monthly savings they generate. If you plan to stay in the home longer than that break-even period, buying points makes financial sense.

How to compare mortgage offers using both APR and interest rate

Using both numbers together gives you a complete picture of any mortgage offer. Neither metric alone tells the full story.

- Use APR to compare total costs across lenders. When two lenders offer different interest rates and fee structures, APR is the single number that accounts for both. A loan with a 6.8% interest rate and a 6.85% APR has very low fees. A loan with a 6.5% interest rate and a 7.1% APR is loaded with costs.

- Use the interest rate to project your monthly payment. Your monthly mortgage payment is calculated from the interest rate, not the APR. Use the interest rate when running payment scenarios in a mortgage calculator.

- Watch for a large APR-to-interest-rate gap. A gap larger than 0.5% on a conventional mortgage is worth questioning. Ask the lender to itemize every fee included in the APR calculation.

- Compare loans with the same term length. APR comparisons are only valid between loans with the same term. Comparing a 15-year APR to a 30-year APR produces a misleading result.

- Factor in your timeline. As discussed, short-term holders benefit from low fees even at a higher rate. Long-term holders benefit from lower rates even with higher upfront fees.

Comparing mortgage offers side by side using both metrics is the most reliable way to identify which loan actually saves you money. Many borrowers skip this step and focus only on the advertised interest rate, which is exactly what some lenders count on. Experts emphasize APR's importance for comparing true loan costs beyond just advertised interest rates.

Key takeaways

APR is the more complete measure of mortgage cost because it includes the interest rate plus lender fees, making it the right tool for comparing offers across lenders.

| Point | Details |

|---|---|

| APR includes fees, interest rate does not | Use APR to compare total loan costs across different lenders and fee structures. |

| Interest rate drives your monthly payment | Use the interest rate when calculating what you will owe each month. |

| The APR gap reveals lender fees | A wider gap between APR and interest rate signals higher fees rolled into the loan. |

| Short-term holders should prioritize low fees | If you plan to sell or refinance within 5 years, lower upfront fees often matter more than a lower rate. |

| Always compare loans with the same term | APR comparisons are only valid between loans with identical term lengths. |

My take on what most borrowers get wrong

Most borrowers walk into a mortgage comparison focused entirely on the interest rate. That instinct is understandable. The interest rate is the number lenders advertise, and it directly controls the monthly payment you see in your budget. But in my experience working with homebuyers, the interest rate alone is one of the most misleading numbers in the mortgage process.

Here is what I have seen repeatedly: a borrower gets excited about a 6.25% rate from a retail lender, only to discover after signing that the APR was 6.9%. That gap represents thousands of dollars in fees that were never clearly explained upfront. A wholesale broker offering 6.5% with an APR of 6.6% would have been the cheaper loan by a significant margin over 30 years.

The APR-to-interest-rate gap is the single most underused tool in mortgage shopping. When you see a large gap, do not accept a vague explanation. Ask the lender to walk through every fee line by line. If they hesitate, that tells you something. Transparent lenders welcome that conversation because they know their numbers hold up.

One more thing: do not let a lender rush you past the Loan Estimate. That document exists to protect you. Read the APR, compare it to the interest rate, and ask what is driving the difference. That one habit will save more money than almost any other step in the mortgage process. Use the mortgage shopping checklist to make sure you are asking the right questions at every stage.

— LoFi

See how Lofirate helps you compare real mortgage offers

Understanding APR vs. interest rate is only useful if you have multiple real offers to compare. Most retail lenders show you one set of numbers and call it competitive. Lofirate works differently.

Lofirate connects you with licensed wholesale mortgage brokers who shop multiple lenders on your behalf. That means you see side-by-side offers with different interest rates, fee structures, and APRs, giving you the data you need to make an informed decision. There is no obligation and no pressure. Whether you are purchasing a home or refinancing, request a broker consultation through Lofirate and find out what your mortgage actually costs across the full range of available options. You can also explore the full range of broker matching services to see how the process works.

FAQ

What is the main difference between APR and interest rate?

The interest rate is the yearly cost of borrowing the loan principal expressed as a percentage. APR includes that interest rate plus lender fees and certain closing costs, making it a broader measure of total borrowing cost.

Which number should I focus on when comparing mortgages?

Use APR to compare total costs across lenders and use the interest rate to estimate your monthly payment. Both numbers together give you a complete picture of any mortgage offer.

Why is APR almost always higher than the interest rate on a mortgage?

APR is higher because it includes lender fees, origination charges, and discount points on top of the interest rate. The only time APR equals the interest rate is when a loan carries zero fees.

Does a lower APR always mean a cheaper mortgage?

Not always. APR assumes you hold the loan for its full term. If you sell or refinance within a few years, a loan with a slightly higher rate but lower upfront fees may cost less in total.

What fees are included in APR for a mortgage?

APR typically includes origination fees, discount points, mortgage broker fees, and certain underwriting charges. Costs like title insurance, appraisal fees, and prepaid homeowners insurance are generally excluded from the APR calculation.