TL;DR:

- APR reflects the true cost of a mortgage by including interest, fees, and points, unlike the interest rate alone. It enables borrowers to compare loan offers accurately, but must be considered alongside cash-to-close and monthly payments for best results. Relying solely on APR can be misleading, so evaluating the full financial picture and expected time in the home is essential before making a decision.

Most homebuyers fixate on the interest rate when shopping for a mortgage, assuming it represents what the loan actually costs. It doesn't. Understanding what is APR in mortgages is one of the most useful things you can do before signing anything, because APR folds in fees, points, and other charges that your interest rate conveniently leaves out. Two loans with identical interest rates can cost thousands of dollars more or less over time based on APR alone. If you're buying your first home or thinking about refinancing, this guide will show you exactly how APR works and how to use it to your advantage.

Table of Contents

- What is APR and how is it calculated?

- Breaking down APR components: interest, fees, and points

- How APR helps you compare mortgage offers effectively

- APR differences in fixed-rate and adjustable-rate mortgages

- Practical tips for using APR in your mortgage decisions

- Why relying solely on APR can mislead and what to do instead

- Find your best wholesale mortgage rates with LoFiRate

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| APR includes interest and fees | APR shows the total annual cost of your mortgage by combining interest rate with fees. |

| Regulated APR calculation | Mortgage APR is computed using standardized methods defined by federal Regulation Z. |

| Compare APR, not just rate | Using APR helps you compare loan costs more accurately than relying on interest rate alone. |

| Loan fees affect APR | Origination fees, points, and closing costs raise APR and impact your total mortgage expense. |

| APR differs by loan type | Fixed-rate mortgages have predictable APRs; adjustable-rate loan APRs can vary with interest changes. |

What is APR and how is it calculated?

APR stands for Annual Percentage Rate. It's the true annualized cost of borrowing, expressed as a percentage that includes both your interest rate and certain finance charges rolled in. The interest rate tells you what you'll pay to borrow the principal. APR tells you what the loan actually costs you per year when fees are included.

Here's how lenders calculate it:

- Add up all finance charges included in the loan: origination fees, underwriting fees, prepaid interest, mortgage points, and any other lender fees the law requires to be counted.

- Spread those charges over the loan term. A $5,000 origination fee on a 30-year loan is distributed across 360 monthly payments.

- Express the total as an annual rate, which is why APR is almost always higher than your note rate.

The math behind this isn't arbitrary. Regulation Z APR calculations are governed by the Truth in Lending Act, and lenders are legally required to compute and disclose APR using the standardized methods in Appendix J for closed-end credit transactions. That standardization is the point. It forces every lender to use the same math, which makes their offers comparable on paper.

This is also why lenders who offer "no-fee" loans sometimes have higher rates. They bake their profit into the rate instead of the fees. The APR may end up similar either way, which is exactly why reading transparent mortgage pricing is critical before you commit.

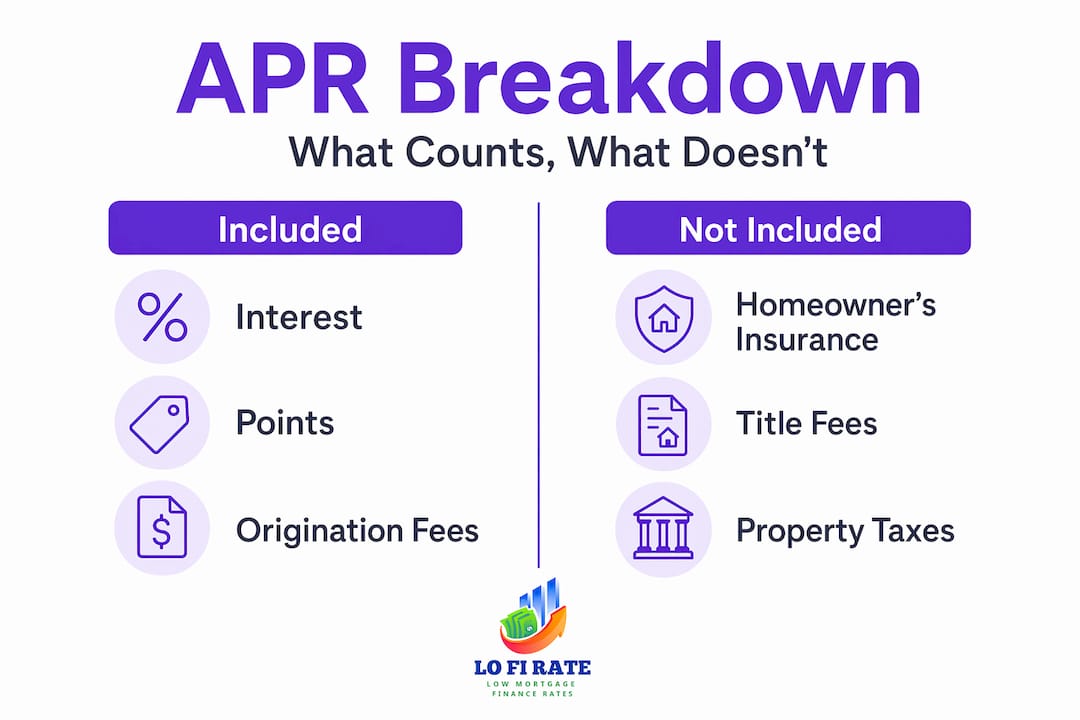

Breaking down APR components: interest, fees, and points

Understanding APR components clarifies why two loans with the same interest rate can have different total costs. The interest rate is just the starting point. Here's what else feeds into APR:

- Origination fees: Charged by the lender for processing your loan. Even a 1% origination fee on a $400,000 mortgage adds $4,000 upfront, which raises the APR when annualized.

- Discount points: Prepaid interest you buy to lower your rate. One point equals 1% of the loan amount. Paying two points on a $400,000 loan costs $8,000 upfront, which increases APR even though your monthly payment goes down.

- Underwriting and processing fees: These are lender charges for reviewing and approving your application. They go into the APR calculation too.

- Mortgage broker fees: If applicable, broker compensation is a finance charge that influences APR.

- Prepaid interest: The interest that accrues between your closing date and the end of that month is factored in.

Finance charges as an annual rate — which is exactly how APR is expressed — reflect both interest and those upfront costs spread over your loan life. Meanwhile, loan fees impact your cash at closing and influence total cost, which is why you need to look at them together, not in isolation.

Understanding which costs are counted in APR (and which aren't, like homeowner's insurance or title insurance) is key. A deeper look at mortgage fees explained can help you sort which costs belong in the APR calculation and which ones are separate expenses you'll still need to budget for.

Pro Tip: When you receive a Loan Estimate, the APR appears on page 3. If the APR is more than 0.125% higher than the interest rate, there are meaningful fees built into that loan. That gap is your first signal to start asking questions.

How APR helps you compare mortgage offers effectively

With a clear understanding of APR's role in comparing loans, let's examine specific scenarios involving fixed and adjustable rate mortgages. APR was designed to make this comparison fair. According to standardized APR disclosure rules, lenders must calculate APR using the same methodology for the same type of loan, so a 30-year fixed from one lender is directly comparable to a 30-year fixed from another.

Here's what a side-by-side comparison might look like:

| Loan option | Interest rate | Points paid | Origination fee | APR |

|---|---|---|---|---|

| Lender A | 6.50% | 1 point ($4,000) | $1,500 | 6.82% |

| Lender B | 6.75% | 0 points | $800 | 6.89% |

| Lender C | 6.625% | 0.5 points ($2,000) | $1,000 | 6.81% |

Lender A has the lowest interest rate, but it costs you $4,000 upfront in points. Lender C has a lower APR than both. None of this is obvious from the rate alone.

Here's what to do when comparing mortgage offers:

- Request a Loan Estimate from at least three lenders on the same day (rates move daily)

- Compare APR alongside cash required at closing

- Calculate the breakeven point on any points paid, meaning how long before your lower payment recoups the upfront cost

- Note the loan term — a 25-year loan will show a higher APR than a 30-year loan with the same fees, because those fees are spread over fewer payments

Points affect finance charges and APR, so you should never evaluate them separately. A lender who quotes you a great rate and buries two points in the fine print is not giving you a deal. That's exactly why comparing lenders consistently saves borrowers thousands of dollars.

APR differences in fixed-rate and adjustable-rate mortgages

Fixed-rate and adjustable-rate mortgages (ARMs) handle APR very differently, and that difference matters depending on how long you plan to stay in the home.

For a fixed-rate mortgage, APR is straightforward. The rate never changes, the fees are known at closing, and the APR reflects the real cost over the full loan term. You can trust that number.

For an adjustable-rate mortgage (ARM), APR is more complicated. ARM APR calculations incorporate estimated future interest rate changes, which means the disclosed APR is partly based on projections, not certainties. Lenders use assumptions about index rates and adjustment caps to compute it, but those assumptions may not match what actually happens.

Here's what this means in practice:

- An ARM with a 6.00% start rate might show a higher APR than a fixed-rate loan at 6.50% once projected adjustments are factored in

- The disclosed APR for an ARM may understate the actual cost if rates rise sharply after the fixed period ends

- A short-term ARM (like a 5/1) might carry a lower APR than a fixed-rate mortgage APR if you plan to sell or refinance before adjustments kick in

Pro Tip: If you're considering an ARM, ask the lender for the worst-case payment scenario based on the loan's rate caps. Then compare that against the fixed-rate APR to see which risk you're actually taking on.

Practical tips for using APR in your mortgage decisions

With these tips, you can confidently navigate offers and make informed mortgage choices. APR is a powerful tool, but only if you know how to use it in a real shopping process.

- Pull your Loan Estimates on the same day. Mortgage rates change daily, so comparing Loan Estimates from different dates isn't a fair comparison. Request them within 24 hours of each other.

- Check page 3 of the Loan Estimate. That's where APR, total interest paid, and total payments appear. These numbers give you the full picture fast.

- Compare APR and total cash to close together. A low APR with $10,000 in upfront costs might not beat a slightly higher APR with $3,000 in closing costs, depending on how long you plan to stay.

- Get at least three competing offers. Standardized APR disclosures protect borrowers from hidden charges and enable side-by-side comparisons, but only if you actually have multiple offers to compare.

- Ask about every fee. Some lenders add fees that don't affect APR but still cost you money at closing, like title fees or settlement charges. Use the mortgage shopping checklist to make sure you're not missing anything.

Still not sure whether your current offer is competitive? Consider getting a second opinion on your mortgage before committing. Borrowers who shop two or more lenders routinely find better pricing than those who accept the first offer.

Pro Tip: If you're refinancing, run a break-even analysis on the APR difference. If refinancing saves you $150 per month but costs $4,500 in fees, you need 30 months just to recoup the cost. A lower APR only helps you if you stay in the loan long enough to benefit.

Why relying solely on APR can mislead and what to do instead

Here's the uncomfortable truth most mortgage articles won't tell you: APR is essential, but using it as your only metric can lead you to the wrong loan.

The problem starts with what APR excludes. Ongoing loan fees that may change over time are not always captured in the APR figure. Private mortgage insurance, escrow adjustments, and variable servicing fees won't show up in the number your lender discloses. For some borrowers, those costs are significant.

There's also a time horizon issue. APR assumes you hold the loan to term. If you sell in seven years, the fee amortization math changes completely. A loan with a higher APR but lower closing costs might cost you less in total if you move before year ten. The loan with the "better" APR could actually be the more expensive choice for your specific situation.

A more grounded approach to reading real loan costs means looking at three numbers together: APR, monthly payment, and total cash to close. Then factor in your expected time in the home. APR earns its place as a comparison tool, but it's not a substitute for working through the actual numbers. The best way to compare mortgage rates effectively is to build a simple spreadsheet with all three variables for each offer. It takes 20 minutes and can save you real money.

Find your best wholesale mortgage rates with LoFiRate

Now that you understand how APR works, you're in a stronger position to shop. But knowing what to look for and having access to competitive offers are two different things.

Most borrowers shop retail lenders and compare what they're shown. Wholesale mortgage brokers operate differently. They work with multiple lenders and access pricing that isn't available to the public directly. That means you could get a lower rate, fewer points, and a more favorable APR simply by going through a different channel. LoFiRate connects you with licensed wholesale brokers in your state who can shop multiple lenders on your behalf through mortgage broker matching services. There's no obligation and no cost to explore your options. You can review loan options at LoFiRate and request a consultation today.

Frequently asked questions

What does APR stand for in mortgages?

APR stands for Annual Percentage Rate, representing the total yearly cost of your mortgage. It includes interest and certain finance charges expressed as a single annualized percentage.

Why is the APR higher than the interest rate on my mortgage?

APR is higher because it folds in upfront fees and points alongside interest. APR includes origination fees, points, and closing costs that the base interest rate does not reflect.

Can APR change after I finalize my mortgage?

For a fixed-rate mortgage, APR is locked in at closing and does not change. APR changes only if ongoing loan fees vary over time, which is rare for standard fixed loans.

Should I choose a loan with the lowest APR?

Lowest APR is a strong starting point but not the only factor. Use APR alongside cash-to-close and monthly payment to evaluate which loan truly fits your budget and timeline.

How does APR differ between fixed-rate and adjustable-rate mortgages?

Fixed-rate APR is based on known, stable costs throughout the loan. APR for ARMs includes estimated rate adjustments, which makes it less predictable and harder to use as a direct comparison against fixed-rate offers.