TL;DR:

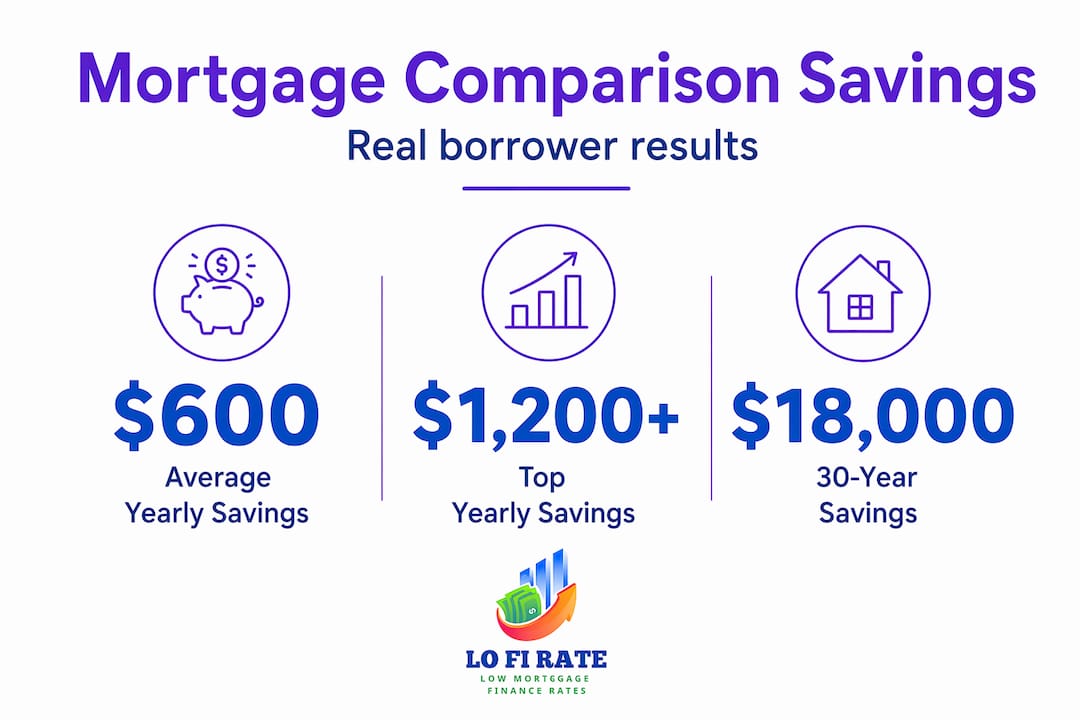

- Shopping around for multiple mortgage lenders can save borrowers $600 to $1,200 annually by uncovering better rates and lower fees. Comparing standardized Loan Estimates reveals true total costs, including fees and cash-to-close, beyond just interest rates. Using multiple quotes and negotiating with lenders based on documented offers significantly impacts long-term savings.

Most homebuyers accept the first mortgage offer they receive and move on, assuming it's a fair deal. It almost certainly isn't the best one. Research from the Consumer Financial Protection Bureau shows that shopping multiple lenders can save borrowers between $600 and $1,200 per year on their mortgage. Over a 30-year loan, that math becomes startling. This article breaks down exactly why one offer leaves money on the table, how much you can realistically save, and what to actually compare when reviewing lender offers side by side.

Table of Contents

- Why one offer rarely reveals your best deal

- How much can you really save by comparing offers?

- What should you actually compare? Key parts of a Loan Estimate

- How to shop smart: Minimize hassle and protect your credit

- The real reason most people skip this step—and what it costs them

- Get the best deal on your mortgage with LoFiRate

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Multiple offers mean savings | Comparing lender offers can save you hundreds or thousands of dollars on your mortgage. |

| Look beyond the rate | Focus on total loan cost, including fees, not just the advertised interest rate. |

| Smart timing protects credit | Requesting multiple quotes within a short period keeps your credit score safe. |

| Standardized forms make comparison easy | Loan Estimates let you compare different lenders side by side with clear terms. |

| Negotiation power increases | Multiple offers put you in control, giving you leverage with lenders for a better deal. |

Why one offer rarely reveals your best deal

When you walk into your bank or click "apply" on the first lender's website, you're getting one data point. That single number tells you almost nothing about whether it's competitive. Lenders price loans differently. They weigh your credit score, debt-to-income ratio, and loan size through their own internal models, which means two lenders can look at the exact same borrower and come back with meaningfully different offers.

Here's what makes this especially frustrating: the difference between offers isn't always visible in the headline interest rate. A lender might advertise a lower rate but pack the offer with origination fees, discount points, or higher third-party service charges. Another might show a slightly higher rate but charge you $3,000 less at the closing table. Without a side-by-side look, you'd never catch it.

The standardized Loan Estimate form was designed to fix exactly this problem. Every lender is required to provide it within three business days of receiving your application. It includes:

- The interest rate and APR (annual percentage rate)

- Estimated monthly payment

- Loan term and loan type (fixed vs. adjustable)

- Origination charges and lender fees

- Third-party service fees (appraisal, title, etc.)

- Total cash to close

- Prepayment penalties or balloon payment disclosures

As the CFPB points out, reviewing multiple offers lets you evaluate the true total cost of a loan, not just the interest rate. That distinction matters enormously because two loans with the same rate can cost very different amounts depending on the fees folded in.

"If you only compare interest rates without looking at fees and cash to close, you're essentially comparing the cover price of two books while ignoring how many pages you're paying for."

Your existing bank or credit union may feel like the obvious first stop. Familiar faces, existing relationships, maybe a loyalty discount. But loyalty rarely translates into the lowest mortgage rate. Retail lenders price loans based on their own cost structures and profit margins. They're not incentivized to tell you that a competitor down the street would charge you less. That's why it pays to explore your mortgage savings potential before committing to any single offer.

Using home buying decision tools alongside your Loan Estimates gives you an even clearer picture of your full financial picture before signing anything.

How much can you really save by comparing offers?

Let's put hard numbers on this. The CFPB cites Freddie Mac research showing that borrowers who get multiple lender quotes can save between $600 and $1,200 annually. Investopedia confirms that shopping around aggressively can lower your interest rate by up to 28 basis points (0.28%) for some borrowers, and the annual savings typically land in that same $600 to $1,200 range.

Here's what 0.28% actually looks like on a real loan:

| Loan Amount | Rate (Lender A) | Rate (Lender B) | Monthly Difference | Annual Savings | 30-Year Savings |

|---|---|---|---|---|---|

| $300,000 | 7.00% | 6.72% | ~$56 | ~$672 | ~$20,160 |

| $400,000 | 7.00% | 6.72% | ~$74 | ~$888 | ~$26,640 |

| $500,000 | 7.00% | 6.72% | ~$92 | ~$1,104 | ~$33,120 |

These are real differences that come from reviewing multiple mortgage quotes rather than accepting the first offer. The higher your loan balance, the more dramatic the impact.

The savings don't stop at the interest rate. Upfront fees vary significantly between lenders. Origination fees alone can range from $500 to $3,000 or more on the same loan. Processing fees, underwriting fees, and even the cost of required services like appraisals can differ from lender to lender. A thorough review of the closing costs breakdown in each offer shows you the full financial picture.

Statistic: Freddie Mac data shows that getting five quotes instead of one can lower your rate by an average of 0.17% to 0.20%. Even two quotes are better than one.

Pro Tip: Don't evaluate lender offers separately and try to remember which is better. Place all Loan Estimates side by side in a spreadsheet or printed on a table. Your eyes will catch discrepancies that memory alone will miss.

The compounding effect of even a modest rate improvement is remarkable. A $400,000 loan at 7.00% costs roughly $2,661 per month in principal and interest. The same loan at 6.72% costs about $2,587. That's $74 per month, $888 per year, and $26,640 over 30 years. That's a meaningful financial outcome that comes from one phone call or one additional application.

What should you actually compare? Key parts of a Loan Estimate

The Loan Estimate's standardized structure is your greatest asset in this process. Every lender uses the same format, which means your job is to look at the same line items across multiple documents and flag the differences.

Here's where to focus your attention:

Page 1: The basics

- Interest rate: The rate your loan will actually use to calculate interest

- APR: A broader cost measure that includes fees. If the APR is much higher than the interest rate, fees are baked in

- Monthly principal and interest payment

- Estimated total monthly payment (including taxes and insurance)

Page 2: The real cost comparison

- Section A: Origination charges (what the lender charges you directly)

- Section B: Services you cannot shop for (set by the lender)

- Section C: Services you can shop for (you have some control here)

- Cash to close: The total you'll need at the closing table

Here's a simple comparison framework:

| What to compare | Why it matters | Red flag to watch |

|---|---|---|

| Interest rate | Drives your monthly cost | Teaser rates with high fees |

| APR | Reflects true annualized cost | APR much higher than rate |

| Origination fees | Direct lender profit | Vague or bundled "processing" fees |

| Cash to close | Your out-of-pocket on day one | Wide variation with no explanation |

| Loan type/term | Must match for fair comparison | ARM vs. fixed, 15 vs. 30 year |

| Points paid | Prepaid interest to buy a lower rate | 1 point costs 1% of loan amount |

To make a fair comparison, follow these steps:

- Request Loan Estimates for the exact same loan type, term, and loan amount from each lender.

- Compare interest rates and APRs first. A significant gap between them signals high fees.

- Review Section A (origination charges) carefully. This is where lenders most commonly differ.

- Add up all lender fees and compare totals, not individual line items.

- Check if either offer includes discount points. A lower rate might come with points you'd need to pay upfront.

- Compare cash-to-close figures. This is what you'll actually need on closing day.

You can explore loan shopping explained for a deeper walkthrough of each section, and reviewing guidance on choosing the right mortgage lender will help you evaluate lender reputation alongside cost.

Pro Tip: Use the CFPB's free compare home listings and loan comparison worksheets as a template. They give you a structured checklist for reviewing each section of multiple Loan Estimates without missing anything.

Small fees that look insignificant can compound into serious costs. A $400 difference in title insurance, a $250 higher appraisal fee, and a $600 difference in origination costs add up to $1,250 out of your pocket at closing. Track every line.

How to shop smart: Minimize hassle and protect your credit

One reason buyers hesitate to compare mortgage offers is fear of credit damage. Multiple lenders pulling your credit report feels risky. The good news: it's not as damaging as you think. Applying within a short window of about 14 to 15 days generally means most credit scoring models count all the inquiries as a single pull. Your score might dip slightly, but the long-term savings from comparison far outweigh a short-term credit fluctuation.

Here's how to shop smartly and efficiently:

- Start with a narrow window. Kick off all applications within the same two-week period. Request Loan Estimates from at least three lenders.

- Keep a comparison tracker. Use a simple spreadsheet with column headers for each lender and row entries for each Loan Estimate line item. This makes it easy to spot where they diverge.

- Ask each lender the same questions. "What's your total origination fee?" and "Are any discount points included in this rate?" Those two questions will surface most of the hidden costs.

- Let lenders compete. Once you have multiple Loan Estimates, tell each lender what the others offered. Most lenders will negotiate rather than lose your business, especially on fees.

- Watch the lock period. Make sure each rate quote reflects the same lock period (30 days, 45 days, or 60 days). Longer locks cost more, and mixing them makes comparison unreliable.

Review a mortgage shopping checklist before you start reaching out to lenders. Having a plan keeps the process from feeling overwhelming. Use mortgage affordability calculators to understand what monthly payment you can comfortably carry before comparing rates.

Pro Tip: When a lender offers to "match" a competitor's rate, ask them to also match the fees. Rate-matching without fee-matching is a partial win at best.

Negotiating with competing offers in hand is one of the most powerful positions you can be in as a buyer. Lenders know their margins. When you show up with a written Loan Estimate from a competitor, you're not guessing at what's fair. You have documented evidence. That changes the conversation entirely.

The real reason most people skip this step—and what it costs them

Here's an uncomfortable truth: most buyers skip offer comparison not because it's difficult, but because it feels socially awkward. They've built a relationship with a loan officer, they feel loyal to their bank, or they're afraid of seeming difficult. The mortgage industry has quietly benefited from this psychology for decades.

There's also analysis paralysis at play. When buyers hear "compare multiple offers," they imagine weeks of paperwork and stress layered on top of an already exhausting home purchase. But the actual effort is modest. Three applications in two weeks, two hours reviewing documents, one or two follow-up calls. That's roughly a $10,000 return on a few hours of work when you factor in the lifetime savings.

The market environment makes this more urgent than ever. Rate volatility in 2025 and into 2026 means that two lenders pricing on the same day can be 0.25% to 0.50% apart, not just a rounding difference. Lenders adjust pricing frequently based on their pipeline volume, secondary market conditions, and internal funding costs. Even if one lender gave you a great deal six months ago, they may not be the most competitive today.

Technology has genuinely changed the comparison game. Technology and mortgage shopping have converged in ways that make it faster than ever to request quotes, receive Loan Estimates digitally, and compare offers without leaving your couch. The friction that once justified skipping this step no longer exists.

The buyers who walk away with the best mortgage rates aren't necessarily the wealthiest or most financially sophisticated. They're the ones who asked twice, compared carefully, and didn't mistake comfort for value. One extra application can change your financial trajectory for the next 30 years.

Get the best deal on your mortgage with LoFiRate

Comparing multiple lender offers is the single most powerful thing you can do to lower your mortgage costs. But managing multiple lender relationships, reviewing Loan Estimates line by line, and negotiating effectively takes time most buyers don't have.

That's where LoFiRate comes in. LoFiRate connects you with licensed wholesale mortgage brokers who already work with multiple lenders on your behalf, meaning you get the benefit of comparison without the legwork. Wholesale brokers access pricing that retail lenders rarely offer directly to the public, giving you a built-in advantage from the start. Explore the full range of loan options available through wholesale broker access, and review the mortgage broker matching services that connect you with the right expert for your situation. Whether you're purchasing your first home or refinancing an existing loan, getting a second opinion costs nothing and could save you thousands.

Frequently asked questions

Does comparing loan offers hurt my credit score?

If you request multiple Loan Estimates within a short window of about 14 to 15 days, most scoring models treat them as a single credit inquiry, so your credit score is generally not harmed in any meaningful way.

What is a Loan Estimate and why is it important?

A Loan Estimate is a standardized document required from every lender that outlines your interest rate, fees, and loan terms in a consistent format, making it straightforward to compare offers side by side.

Is it really possible to save thousands by shopping for mortgage offers?

Yes. Borrowers who compare quotes can save $600 to $1,200 per year, and on larger loans the lifetime savings from even a 0.28% rate improvement can exceed $25,000 to $30,000.

What should I watch out for when comparing Loan Estimates?

Always confirm you're comparing the same loan type, term, and points structure. The standardized Loan Estimate format helps, but fees and cash-to-close figures can still vary significantly even when rates look nearly identical.

Can I negotiate with lenders using other offers?

Absolutely. The CFPB explicitly encourages comparing and negotiating offers, and presenting a written competing Loan Estimate gives you concrete leverage to request lower fees or a better rate from your preferred lender.