TL;DR:

- Choosing a shorter mortgage term results in higher monthly payments but significantly reduces total interest paid. Longer terms lower monthly costs, offering more flexibility but increasing overall interest and building equity more slowly. Prepayment options and market conditions allow borrowers to adjust their repayment strategies over time.

Mortgage loan duration is the length of time you have to repay your home loan, and it directly controls both your monthly payment and the total interest you pay over the life of the loan. The two most common mortgage loan term options in the United States are the 15-year and 30-year fixed loans. Knowing how to select mortgage loan duration that fits your income, goals, and risk tolerance is one of the most consequential financial decisions you will make as a homebuyer. Tools from the Consumer Financial Protection Bureau (CFPB), SoFi, and Quicken Loans all offer calculators and guides to help you run the numbers before you commit.

How do different mortgage loan durations affect your monthly payments and total interest?

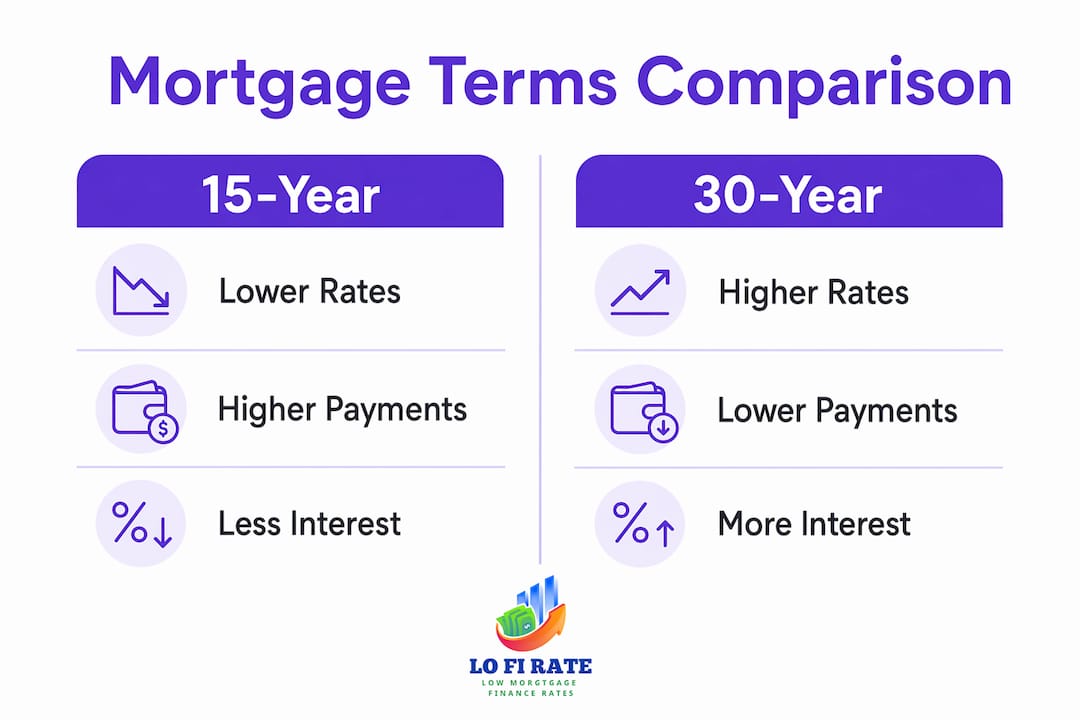

The core trade-off is simple: shorter terms mean higher monthly payments and far less total interest paid. Longer terms mean lower monthly payments and significantly more interest over time.

15-year mortgages carry interest rates up to 1 percentage point lower than 30-year loans. That rate gap compounds over time, meaning a borrower on a 15-year loan pays less interest per dollar borrowed and retires the debt in half the time.

To make this concrete, consider a $400,000 loan. On a 30-year term at 7%, your monthly principal and interest payment sits near $2,661. On a 15-year term at 6.25%, that payment climbs to roughly $3,430. The monthly difference is about $769, but the total interest saved over the life of the loan runs into the tens of thousands of dollars.

| Feature | 15-year fixed | 30-year fixed |

|---|---|---|

| Typical interest rate | Up to 1% lower | Standard market rate |

| Monthly payment | Higher | Lower |

| Total interest paid | Significantly less | Significantly more |

| Equity building speed | Faster | Slower |

| Payment flexibility | Less | More |

Pro Tip: Run both scenarios in the CFPB's mortgage calculator before you apply. Seeing the exact dollar difference in total interest paid often changes a borrower's decision entirely.

The right mortgage duration comparison is not just about the monthly number. It is about what that payment costs you in flexibility, savings, and financial security over the next decade or more.

What financial factors should guide your choice of mortgage loan duration?

Your income, existing debt, savings cushion, and how long you plan to own the home all shape the ideal loan term for your situation.

Financial experts recommend that total housing costs stay within 28% of your gross monthly income. That figure includes your mortgage payment, property taxes, and homeowner's insurance. If a 15-year payment pushes you past that threshold, a longer term is the safer starting point.

Before choosing a shorter term, ask yourself these questions:

- Do you have three to six months of living expenses saved? A higher mortgage payment shrinks your buffer against job loss or medical costs.

- Do you carry high-interest debt? Paying off credit card balances at 20% interest beats accelerating a mortgage at 6%.

- How stable is your income? Freelancers and commission-based earners benefit from the lower required payment of a 30-year loan.

- How long do you plan to stay? Loan term choice depends on how long you intend to keep the property. If you plan to sell in seven years, a 30-year term with extra payments often makes more sense than locking into a 15-year obligation.

- What are your retirement savings looking like? If you are behind on retirement contributions, the cash flow from a longer term may be better deployed in a 401(k) or IRA.

Pro Tip: Use a mortgage payment breakdown tool to model your exact numbers. Plug in your gross income, current debts, and target home price to see which term keeps you inside the 28% guideline.

The best loan length for a mortgage is the one that leaves you financially stable, not just technically affordable.

How can prepayment options and refinancing affect your mortgage loan duration strategy?

Choosing a loan term does not lock you in permanently. Two tools give you real flexibility: extra principal payments and refinancing.

Most conventional U.S. mortgages do not carry prepayment penalties, which means you can pay more than your required monthly amount at any time. That freedom lets you choose a 30-year term for payment security and still pay the loan off faster when your cash flow allows.

Here is how to use prepayment and refinancing strategically:

- Start with a 30-year term. Lock in the lower required payment as your baseline. This protects you if income drops or expenses spike.

- Make extra principal payments when cash flow allows. Even one extra payment per year can shorten a 30-year loan by several years and save thousands in interest.

- Track your equity and rate environment. When you have built meaningful equity and market rates drop, refinancing into a 15-year loan at a lower rate can lock in the shorter timeline without the original payment risk.

- Avoid refinancing too frequently. Closing costs typically run 2%–3% of the loan balance. Refinancing every two years erodes the savings you are trying to capture.

This approach, sometimes called smart ways to save on your mortgage, gives you the discipline of a shorter term without the financial rigidity.

What are the less common mortgage term options and when are they suitable?

The 15-year and 30-year loans dominate the market, but several other mortgage loan term options exist for buyers with specific needs.

10-year fixed loans carry the lowest interest rates and the fastest payoff. They suit high-income buyers who want to own their home outright before retirement. The monthly payment is the highest of any fixed option, so qualifying requires strong income.

20-year fixed loans split the difference between 15 and 30 years. The payment is more manageable than a 15-year loan, and the total interest is far less than a 30-year. This term works well for buyers who refinanced from a 30-year loan and want to reset without extending back to a full 30-year clock.

25-year fixed loans are less common in the U.S. market but appear occasionally through portfolio lenders. They offer modest payment relief compared to a 20-year term.

40-year mortgages carry the lowest monthly payments but the highest total interest of any fixed option, and they are harder to qualify for. They are not widely available and are generally a last resort for buyers who cannot afford a standard 30-year payment.

Adjustable-rate mortgages (ARMs) typically carry 30-year terms with a fixed initial period, such as 5, 7, or 10 years, after which the rate adjusts annually. ARMs make total interest unpredictable. They suit buyers who are confident they will sell or refinance before the fixed period ends.

For buyers interested in non-traditional mortgage options, understanding how the amortization period interacts with the loan term is critical. With ARMs especially, distinguishing loan term from amortization period clarifies how quickly you build equity and when refinancing makes sense.

How do opportunity cost and investment returns influence your loan term decision?

Choosing a shorter mortgage term is not automatically the best financial move. The math depends on what you would do with the extra cash if you chose a longer term instead.

When the interest rate difference between a 15-year and 30-year loan is small, investing the extra cash may outperform paying down the mortgage early. The CFPB notes that if the rate differential is less than 0.5%, investing the difference can be the wiser financial move.

The logic works like this. If your 30-year rate is 7% and your 15-year rate is 6.5%, the gap is only 0.5 percentage points. Historically, a diversified stock portfolio has returned more than that over long periods. Paying the lower 30-year payment and investing the difference could leave you with more net wealth than the borrower who chose the 15-year term.

This calculation flips when the rate gap is larger, when you are close to retirement, or when you have low risk tolerance. A guaranteed 1% interest savings is a different proposition than a potential market return that could go negative in a bad year. Opportunity cost analysis is key. The right answer depends on your investment discipline, tax situation, and how close you are to needing the money.

Understanding current mortgage rate trends also matters here. When rates are high, the gap between 15-year and 30-year rates tends to narrow, which shifts the math toward investing rather than accelerating payoff.

Key Takeaways

The best mortgage loan duration balances your monthly payment affordability with total interest costs, and no single term is right for every borrower.

| Point | Details |

|---|---|

| Shorter terms save more interest | 15-year loans carry rates up to 1% lower and build equity faster than 30-year loans. |

| Stay within the 28% income rule | Total housing costs should not exceed 28% of gross monthly income for financial stability. |

| Prepayment adds flexibility | Most U.S. mortgages have no prepayment penalties, so extra payments can shorten any term. |

| Opportunity cost matters | When the rate gap is small, investing extra cash may outperform paying down the mortgage early. |

| Alternative terms exist | 10, 20, 40-year, and ARM options suit specific buyer profiles but come with trade-offs. |

The case for choosing longer and paying faster

The conventional wisdom says choose the shortest term you can afford. My experience working with homebuyers tells a different story. The borrowers who get into the most financial trouble are not the ones who chose a 30-year loan. They are the ones who stretched into a 15-year payment and then had no room to breathe when life happened.

A 30-year mortgage with a disciplined extra payment strategy gives you the best of both worlds. You get the lower required payment as a safety net, and you get the interest savings when you apply extra principal. The key word is disciplined. If you know you will spend the difference rather than invest or prepay it, the forced savings of a 15-year term may serve you better.

The other thing most articles skip is the rate environment. When 30-year rates are elevated, the spread between 15-year and 30-year loans often narrows. That changes the math on whether a shorter term is worth the payment sacrifice. Always run the numbers for the specific rates you are being quoted, not the general rule.

My honest advice: choose the term that lets you sleep at night, keep your emergency fund intact, and still make progress on retirement savings. A mortgage is a tool. Use it on your terms.

— LoFi

How Lofirate connects you to the right loan term and rate

Choosing between a 15-year and 30-year mortgage is only half the decision. The rate you get on that term determines the real cost. Retail lenders offer only their own pricing, which means you may be leaving money on the table without knowing it.

Lofirate connects homebuyers and homeowners with licensed wholesale mortgage brokers who shop multiple lenders to find competitive rates across all loan term options. Whether you are buying your first home or refinancing to a shorter term, a broker matched through Lofirate can show you side-by-side pricing on 15-year, 20-year, and 30-year loans. The consultation is free and carries no obligation. Visit Lofirate's broker matching service to get a second opinion on your mortgage options before you sign anything.

FAQ

What is the most common mortgage loan duration in the U.S.?

The 30-year fixed mortgage is the most widely used loan term in the United States. It offers the lowest required monthly payment among standard fixed options.

Is a 15-year or 30-year mortgage better?

A 15-year mortgage saves more total interest and builds equity faster, but the higher monthly payment requires stronger income. A 30-year mortgage offers more cash flow flexibility and suits borrowers with tighter budgets or other financial priorities.

Can I pay off a 30-year mortgage early?

Most conventional U.S. mortgages carry no prepayment penalties, so you can make extra principal payments at any time. Consistent extra payments can shorten a 30-year loan by several years and reduce total interest significantly.

What is an ARM and how does it affect loan duration?

An adjustable-rate mortgage typically carries a 30-year term with a fixed rate for an initial period of 5, 7, or 10 years, then adjusts annually. The total interest becomes unpredictable after the fixed period ends, which adds risk for borrowers who do not sell or refinance before the adjustment begins.

How do I know which mortgage term I can afford?

Financial experts recommend keeping total housing costs, including your mortgage payment, taxes, and insurance, within 28% of your gross monthly income. Use a mortgage calculator to test different term lengths against your actual income before applying.