TL;DR:

- Mortgage statements detail where your monthly payments go and help you spot errors or savings opportunities.

- Reading each section carefully allows homeowners to understand their loan status, track progress, and avoid mistakes.

Your mortgage statement is a legally mandated financial document that tells you exactly where your money goes every month. Under the Truth in Lending Act and RESPA, servicers must provide clear, accurate billing statements detailing the amount due, due date, loan balance, and full payment allocation. Most homeowners glance at the total and move on. That habit costs them. A proper mortgage statement analysis guide gives you the tools to read every line, catch errors, and find real savings before they slip away.

What does a mortgage statement include?

Every mortgage statement follows a standard structure. Knowing what each section contains is the first step in understanding mortgage statements and using them to your advantage.

Account and contact information

The top of your statement lists your loan account number, servicer name, and contact details. This section also shows your property address and the name on the loan. Keep this information handy when you call your servicer about any issue.

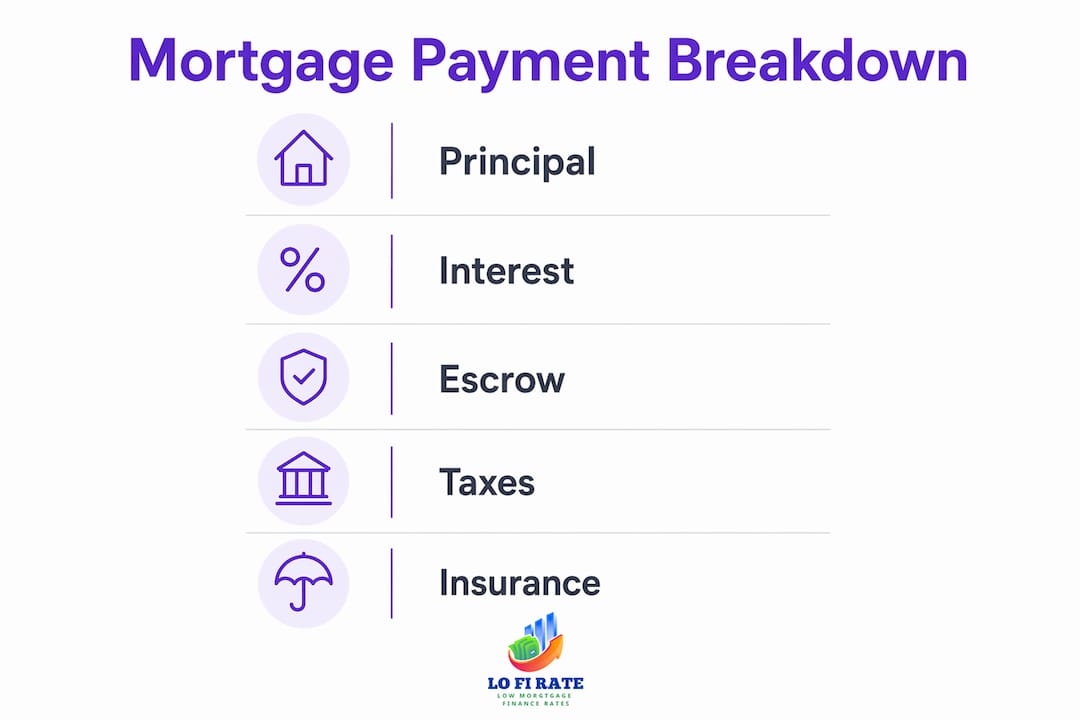

Payment breakdown

The payment breakdown is the most important section on the statement. It shows exactly how your monthly payment splits across four categories:

- Principal: The portion that reduces your actual loan balance

- Interest: The cost of borrowing, calculated on your remaining balance

- Escrow: Funds collected for property taxes and homeowner's insurance

- Fees: Any late charges, returned check fees, or other assessed costs

Early in a loan, interest consumes the largest share of each payment. A $2,000 monthly payment on a 30-year mortgage might send only $400 toward principal in year one. That ratio shifts gradually over time as your balance falls.

Key figures at a glance

| Statement Field | What It Tells You |

|---|---|

| Current loan balance | Total principal still owed |

| Payment amount due | Minimum required payment this cycle |

| Principal paid | Amount reducing your debt this month |

| Interest charged | Cost of borrowing for this period |

| Escrow balance | Funds held for taxes and insurance |

| Outstanding fees | Any unpaid charges added to your account |

Escrow account details

Escrow accounts collect a portion of your monthly payment to cover property taxes and insurance when those bills come due. Your statement shows the current escrow balance and any recent disbursements. A low escrow balance after a large tax payment is normal, but a negative balance signals a shortage you will need to cover.

Delinquency notices

Borrowers more than 45 days delinquent receive detailed notices on their statements covering delinquency length, foreclosure risks, payment history, and available counseling contacts. This regulatory requirement exists to protect borrowers before a situation becomes irreversible.

How do you read each section of a mortgage statement?

Reading a statement accurately requires more than scanning numbers. Each figure connects to others, and misreading one can lead to wrong conclusions about your loan.

-

Start with the payment due date and amount. Confirm the due date matches your expectations. Verify the total matches your loan agreement, especially if you have an adjustable-rate mortgage where the rate resets periodically.

-

Compare your current balance to last month's statement. Your balance should drop by the principal portion of your last payment. If it did not, a payment may have been misapplied or a fee was added.

-

Check the principal vs. interest split. Your mortgage payment breakdown shows this clearly. Early payments are interest-heavy by design. This is called amortization, and it is how fixed-rate loans are structured under standard lending practice.

-

Review the escrow balance. Servicers conduct annual escrow analyses, adjusting your monthly escrow amount when taxes or insurance premiums change. Your statement will notify you of any adjustment before it takes effect.

-

Distinguish your loan balance from your payoff amount. The loan balance is what you owe today. The payoff amount is slightly higher because it includes accrued interest through the date you would pay it off. Never use the loan balance figure when planning a full payoff.

Pro Tip: Request a payoff quote directly from your servicer if you are considering selling, refinancing, or paying off your loan. The statement balance alone will not give you the accurate final figure.

Fixed-rate loans keep your principal and interest payment constant for the loan's life. Adjustable-rate mortgages (ARMs) can change your payment at each adjustment period. If you have an ARM, your statement will show the current interest rate and the next scheduled adjustment date.

How do you track progress and spot saving opportunities?

Your statement is not just a bill. It is a progress report on one of the largest financial commitments of your life.

Mortgage statements include recent payment history and year-to-date totals to track your loan payoff progress. That data helps you confirm on-time payments and assess whether paying down principal early makes financial sense.

Paying an extra $100 toward principal each month on a 30-year loan can shave years off your payoff timeline and save a significant amount in total interest. Your statement shows the current balance, so you can calculate the impact of extra payments using any standard amortization calculator.

Escrow adjustments deserve close attention. When your property taxes rise or your insurance premium increases, your servicer raises your monthly escrow contribution. Reviewing these changes on your statement lets you budget ahead rather than absorb a surprise payment increase mid-year.

Your year-to-date interest total on the statement is also useful at tax time. Mortgage interest is deductible for many homeowners under IRS rules. Keeping your statements organized means you have documentation ready when you file.

Pro Tip: If your statement shows a consistent drop in your escrow balance each month, ask your servicer for an escrow analysis. You may be underfunding it, which leads to a shortage notice and a required lump-sum catch-up payment.

Refinancing decisions also start with your statement. If your current interest rate is significantly above prevailing wholesale rates, the gap between what you pay and what you could pay is visible right there in your interest line. Lofirate connects homeowners with licensed wholesale mortgage brokers who can assess whether refinancing makes financial sense for your specific loan.

For homeowners who also own investment properties, analyzing rental property deals follows similar principles: understanding where cash flows and where costs accumulate is the foundation of every sound financial decision.

What should you do when you find errors on your statement?

Mortgage statement errors are more common than most homeowners expect. Misapplied payments, incorrect late fees, and escrow calculation mistakes all appear on real statements.

Common errors to look for include:

- Misapplied payments: Your payment was received but credited to fees or interest instead of principal

- Incorrect late fees: A fee assessed when your payment was actually on time

- Escrow errors: Taxes or insurance paid at the wrong amount or to the wrong account

- Unauthorized charges: Fees for services you did not request or authorize

- Balance discrepancies: Your balance did not decrease by the correct principal amount

Under RESPA, you have a federal right to send your servicer a formal written Notice of Error. This document requires the servicer to investigate and respond within legally defined timelines. A phone call does not carry the same legal weight. Written disputes create a documented record that protects you if the error is not corrected.

Borrowers have a federal right under RESPA to file a Notice of Error or a Request for Information. The servicer must acknowledge the notice within five business days and resolve it within 30 to 45 business days, depending on the type of error.

Send your dispute letter by certified mail with return receipt. Keep a copy of everything. If the servicer fails to respond within the legal timeline, you have grounds to escalate to the Consumer Financial Protection Bureau (CFPB).

Pro Tip: Never dispute a mortgage error by phone alone. Always follow up any call with a written letter sent to the servicer's designated error resolution address, which is listed on your statement or servicer website.

Understanding mortgage fees that appear on statements helps you identify which charges are legitimate and which warrant a dispute. Not every fee is an error, but every fee deserves scrutiny.

Key Takeaways

Reading your mortgage statement carefully every month is the single most effective habit for protecting your loan and finding real savings.

| Point | Details |

|---|---|

| Know your payment split | Identify how much goes to principal, interest, and escrow each month. |

| Watch your escrow balance | Annual escrow reviews can raise your payment; review notices before they take effect. |

| Use year-to-date totals | Statement summaries support tax deductions and early payoff planning. |

| Dispute errors in writing | A RESPA Notice of Error carries legal weight that a phone call does not. |

| Compare balance to payoff | Your loan balance and payoff amount differ; always request a payoff quote before acting. |

What I have learned from reading mortgage statements closely

Most homeowners treat their mortgage statement like a utility bill. They check the total, confirm the due date, and file it away. That approach leaves real money on the table.

The detail that surprises people most is the escrow section. Servicers adjust escrow contributions every year, and those adjustments can add $50 to $150 to your monthly payment with minimal explanation. Homeowners who read their statements catch these changes early. Those who do not often discover a shortage notice months later, along with a demand for a lump-sum payment.

The second thing I have seen repeatedly is the value of the payment history section. That section is your proof of timely payments. If a servicer ever claims a payment was late, your statement is the first place you look. Borrowers who keep their statements have documentation. Those who discard them are working from memory in a dispute.

The error dispute process under RESPA is genuinely powerful, and most borrowers do not know it exists. A written Notice of Error puts the servicer on a legal clock. That changes the dynamic entirely compared to a phone call that gets logged as a "customer inquiry."

My honest advice: set aside ten minutes each month to read your statement line by line. Compare it to last month's. Note any changes. Ask questions in writing when something does not add up. That habit alone will save you more than most financial tips ever will.

— LoFi

How Lofirate helps you act on what your statement reveals

Your mortgage statement tells you what you are paying. Lofirate helps you find out if you are paying too much.

Lofirate connects homeowners and buyers with licensed wholesale mortgage brokers who shop multiple lenders to find competitive rate options. If your statement shows an interest rate that no longer reflects the market, a broker consultation through Lofirate's services gives you a clear picture of your refinancing options with no obligation. Wholesale brokers access pricing that retail lenders do not offer directly to consumers. That difference can translate to a meaningfully lower rate and a smaller interest line on every future statement. Visit Lofirate to request a free broker match and get a second opinion on your current loan.

FAQ

What is a mortgage statement?

A mortgage statement is a monthly billing document your servicer sends that details your payment due, loan balance, and how your payment splits across principal, interest, and escrow. Federal law under RESPA and the Truth in Lending Act requires servicers to provide accurate statements.

Why does my mortgage balance not drop by my full payment amount?

Most of each payment covers interest, not principal, especially early in the loan. Only the principal portion reduces your balance. Your statement's payment breakdown shows exactly how much went to each category.

What should I do if my mortgage statement shows an error?

Send a written Notice of Error to your servicer's designated address. Under RESPA, the servicer must acknowledge and resolve the dispute within legally defined timelines. A phone call alone does not carry the same legal protection.

Why did my monthly mortgage payment increase?

An increase usually comes from an escrow adjustment. Servicers review escrow accounts annually and raise contributions when property taxes or insurance premiums go up. Your statement will include a notice explaining the change.

Do all mortgage loans come with monthly statements?

Not all loans require periodic statements. Exemptions include small servicers handling fewer than 5,000 loans, reverse mortgages, home equity lines of credit, and loans in active bankruptcy. Borrowers in these situations may receive payment coupons instead.