TL;DR:

- Mortgage compliance ensures transparent, fair, and lawful loan processes for homebuyers.

- Key laws include TILA, RESPA, ECOA, HMDA, and the Fair Housing Act.

- Active borrower oversight helps prevent fees, delays, or discrimination in mortgage transactions.

Getting approved for a mortgage feels like crossing the finish line. But approval and compliance are two different things, and confusing them can cost you real money. Mortgage compliance protects homebuyers from predatory practices and ensures every step of your loan process is transparent. Many borrowers discover too late that their lender made a disclosure error, charged an unallowed fee, or skipped a required timeline. This guide walks you through what mortgage compliance means, which rules matter most, and exactly how to protect yourself before, during, and after closing.

Table of Contents

- What is mortgage compliance?

- Core rules and disclosures every homebuyer should know

- How lenders determine if you qualify: ATR and QM standards

- Fair lending and errors: What can go wrong and how to avoid it

- Practical tips: How homebuyers can safeguard their mortgage process

- Perspective: Why mortgage compliance is your secret weapon if you pay attention

- Next steps: Find a compliant lender for peace of mind

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Mortgage compliance basics | It means lenders must follow consumer protection laws for transparency and fairness. |

| Key rules and disclosures | You should always receive clear disclosures, such as the Loan Estimate and Closing Disclosure, on set timelines. |

| Fair lending protections | Laws prohibit discrimination and mandate lenders report data for transparency. |

| Common pitfalls to avoid | Watch for errors in your disclosures, document everything, and compare lenders to spot differences. |

| Empower your mortgage process | Understanding compliance can help you save money and avoid delays or surprises. |

What is mortgage compliance?

Mortgage compliance is the set of federal and state rules that lenders, brokers, and servicers must follow when originating and managing home loans. Think of it as the rulebook that keeps the mortgage industry honest. When lenders follow these rules, you get clear terms, predictable fees, and fair treatment. When they don't, you could face surprise costs, delays, or even a canceled closing.

Mortgage compliance refers to adherence to laws including the Truth in Lending Act (TILA), the Real Estate Settlement Procedures Act (RESPA), the Equal Credit Opportunity Act (ECOA), the Home Mortgage Disclosure Act (HMDA), and the Fair Housing Act. Each law covers a specific piece of the borrower protection puzzle.

Here's what these laws do for you as a borrower:

- TILA requires lenders to disclose the true cost of your loan, including the annual percentage rate (APR)

- RESPA bans kickbacks between lenders and settlement service providers that inflate your closing costs

- ECOA prohibits discrimination in lending based on race, sex, age, religion, or national origin

- HMDA requires lenders to report loan data publicly so regulators can spot discriminatory patterns

- Fair Housing Act extends anti-discrimination protections to the entire home purchase process

Compliance ensures clear terms, no surprises in fees, and fair access for everyone regardless of background or zip code.

Non-compliance isn't just a paperwork problem. Lenders can face fines, be forced to issue refunds, or lose their operating license entirely. When choosing the right mortgage lender, understanding these rules helps you ask the right questions. It also helps to understand mortgage origination explained so you know where compliance checkpoints fall in the process.

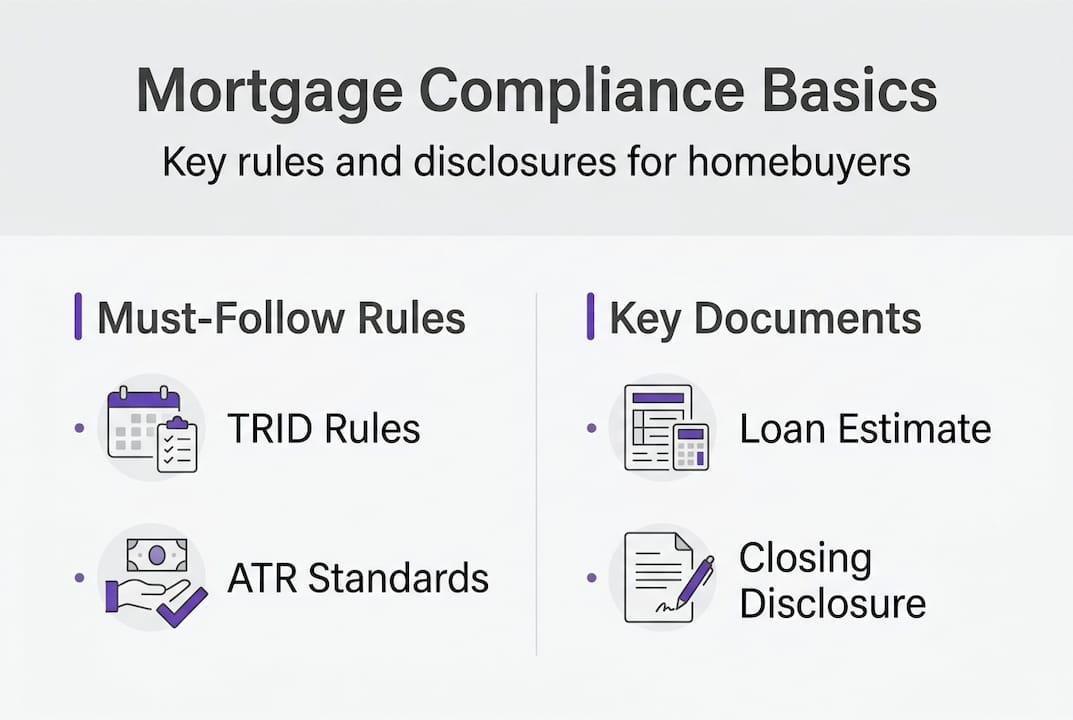

Core rules and disclosures every homebuyer should know

The most important compliance framework you'll encounter is called TRID, which stands for the TILA-RESPA Integrated Disclosure rule. It governs two critical documents: the Loan Estimate and the Closing Disclosure.

According to TRID disclosure rules, the Loan Estimate must arrive within 3 business days of your application, and the Closing Disclosure must reach you at least 3 business days before closing. These aren't suggestions. They're legal requirements.

| Disclosure | Timing | What it covers |

|---|---|---|

| Loan Estimate | Within 3 business days of application | Estimated rate, monthly payment, closing costs |

| Closing Disclosure | At least 3 days before closing | Final loan terms, actual fees, cash to close |

Not all fees are treated equally under TRID. Some have zero tolerance for increases (like lender origination charges), while others have a 10% tolerance (like title services you didn't choose). Knowing this helps you catch overcharges before they stick.

Here's how the compliance timeline flows from start to finish:

- Submit your application and receive a written acknowledgment

- Receive your Loan Estimate within 3 business days

- Lock your rate and confirm your intent to proceed in writing

- Underwriting review with all required income and asset documents

- Receive your Closing Disclosure at least 3 days before closing

- Review and compare both documents for any changes or discrepancies

- Close with confidence that all terms match what was disclosed

Pro Tip: Always compare at least 3 Loan Estimates from different lenders. Small differences in fees and rate can add up to thousands over the life of your loan. Navigating mortgage compliance becomes much easier when you know what to look for on each form. You can also explore mortgage rate transparency to understand how pricing should be disclosed.

Note that TRID does not apply to every loan type. HELOCs, reverse mortgages, and some mobile home loans follow different disclosure rules.

How lenders determine if you qualify: ATR and QM standards

Beyond disclosures, lenders must verify that you can actually repay the loan. This is called the Ability-to-Repay rule, or ATR. It was created after the 2008 housing crisis, when lenders approved borrowers with no income verification and disastrous results followed.

ATR/QM rules require verification of your income, assets, employment history, credit history, monthly debt payments, and debt-to-income (DTI) ratio. Most lenders require a DTI at or below 43% to 50%, though overlays vary by lender and loan type.

| ATR factor | What lenders check |

|---|---|

| Income | Pay stubs, W-2s, tax returns, self-employment records |

| Assets | Bank statements, retirement accounts, gift letters |

| Debts | Credit report, student loans, car payments, existing mortgages |

| Employment | Two-year history, current employer verification |

| DTI ratio | Total monthly debts divided by gross monthly income |

A Qualified Mortgage (QM) is a loan that meets strict ATR standards and offers lenders a legal safe harbor. QM loans cannot include risky features like negative amortization, interest-only periods, or balloon payments. For borrowers, a QM loan generally means more predictable terms and stronger legal protections.

Here's what you need to prepare for ATR compliance:

- Two years of tax returns and W-2s or 1099s

- Recent pay stubs (typically the last 30 days)

- Two to three months of bank statements

- Documentation for any large deposits or gifts

- A complete list of all monthly debt obligations

Pro Tip: Keep records of all income sources and large deposits going back at least 60 days. Unexplained deposits can trigger underwriting questions that delay your closing by days or even weeks. For a full breakdown, review the mortgage qualification steps before you apply.

Fair lending and errors: What can go wrong and how to avoid it

Even when you do everything right, lender errors can derail your mortgage. Fair lending laws exist to prevent discrimination and ensure equal access, but violations still happen at alarming rates.

Fair lending laws prohibit discrimination based on race, sex, national origin, religion, disability, familial status, and other protected characteristics. HMDA reporting helps regulators track whether lenders are serving all communities fairly. When patterns of bias appear in the data, enforcement follows.

The numbers are striking. Penalties for non-compliance across the mortgage industry have reached $19.7 billion in enforcement actions as of January 2026. That's not a rounding error. It reflects how seriously regulators treat these violations.

Even small errors, like mismatched forms or wrong application dates, can trigger large fines for lenders and frustrating delays for borrowers.

Common compliance errors that affect buyers include:

- Late disclosures: Loan Estimate or Closing Disclosure delivered outside required windows

- Fee misclassification: Charging a zero-tolerance fee above the disclosed amount

- Undocumented changes: Altering loan terms without a valid change-of-circumstance on file

- HMDA reporting errors: Incorrect or missing data that obscures lending patterns

- Redlining indicators: Patterns of denial or steering based on neighborhood demographics

You can protect yourself by reviewing every disclosure carefully and asking your lender to explain any line item you don't recognize. Understanding mortgage competition benefits also helps you recognize when something feels off. If you suspect discrimination or a compliance violation, report it to the Consumer Financial Protection Bureau (CFPB). Knowing the right questions for mortgage brokers can also help you surface issues before they become problems.

Practical tips: How homebuyers can safeguard their mortgage process

Knowing the rules is one thing. Using them to protect yourself is another. Here's a practical framework you can follow from application to closing.

- Request multiple Loan Estimates: Compare at least three from different lenders or brokers. Differences in fees and rates are often significant.

- Check your timelines: Confirm your Loan Estimate arrived within 3 business days and your Closing Disclosure at least 3 days before closing.

- Compare both disclosures side by side: Any fee that increased beyond the tolerance limit must be explained and corrected before you sign.

- Document every interaction: Save emails, text messages, and notes from phone calls. Dates and details matter if a dispute arises.

- Review for fair lending red flags: If you feel you were steered toward a higher-cost loan or denied without clear reason, ask for a written explanation.

- Use the CFPB mortgage toolkit: It walks you through every stage of the process with plain-language guidance and comparison worksheets.

Pro Tip: Never feel pressured to sign incomplete or mismatched forms. A compliant lender will welcome your questions. One that discourages them is a red flag worth taking seriously.

If you spot a problem, act quickly. Compliance windows are time-sensitive, and waiting too long can limit your options. Use the mortgage shopping checklist to stay organized, and revisit your mortgage pre-approval tips to make sure your documentation is airtight from the start.

Perspective: Why mortgage compliance is your secret weapon if you pay attention

Most buyers treat compliance like fine print. They assume someone else is checking the boxes, and they just need to show up and sign. That's a costly assumption.

Borrowers who actively engage with compliance requirements consistently get better outcomes. They catch fee overcharges before closing. They push back on disclosure delays that signal disorganized lenders. They ask the questions that reveal whether a lender is cutting corners. That kind of attention is not paranoia. It's leverage.

Here's the part most articles skip: compliance knowledge levels the playing field. A lender who knows you understand TRID tolerances and ATR documentation requirements will be more careful with your file. They know you'll notice mistakes. That alone changes how your loan is handled.

As regulatory technology grows, some lenders rely on automated systems to flag issues. But software doesn't catch everything, especially the nuanced, real-world errors that affect individual borrowers. Your own review is still the best filter. Navigating compliance proactively means you're not just protected. You're in control.

Next steps: Find a compliant lender for peace of mind

If reading this made you realize you want more support during your mortgage process, you're not alone. Most borrowers don't have a compliance expert in their corner. That's exactly the gap LoFiRate was built to fill.

LoFiRate connects you with licensed wholesale mortgage brokers who understand compliance inside and out. Instead of navigating retail lenders who only offer their own pricing, you get access to brokers who shop multiple lenders and explain every step clearly. Explore mortgage broker services to see how the process works, or browse available loan options to compare what's available in your state. No pressure, no obligation. Just a clearer, more protected path to your next home.

Frequently asked questions

What happens if my lender doesn't follow mortgage compliance rules?

Lenders may face fines, be required to issue refunds, or lose their license to operate, and your loan closing could be delayed or canceled as a result.

Which disclosures should I always receive during the mortgage process?

You should always receive a Loan Estimate within 3 business days of applying and a Closing Disclosure at least 3 days before your scheduled closing date.

How do mortgage compliance rules protect homebuyers?

Compliance ensures clear terms, fair access to credit, and protection from hidden fees or discriminatory practices throughout the mortgage process.

What documents do lenders check for ATR/QM compliance?

They verify your income, assets, and DTI ratio, along with employment history and credit obligations, to confirm you can repay the loan.

Can homebuyers report mortgage compliance violations?

Yes, you can report violations or unfair lending practices directly to the Consumer Financial Protection Bureau (CFPB) through their online complaint system.