TL;DR:

- A jumbo loan is a mortgage that exceeds the conforming loan limit set by the FHFA, typically requiring stricter approval criteria. Since Fannie Mae and Freddie Mac cannot purchase these loans, lenders hold full risk, leading to higher credit standards and manual underwriting processes. Borrowers should compare lenders and prepare thorough documentation to secure favorable rates and terms on high-value home financing.

A jumbo loan is a mortgage that exceeds the conforming loan limits set by the Federal Housing Finance Agency (FHFA), making it a non-conforming loan that Fannie Mae and Freddie Mac cannot purchase. For 2026, the baseline limit is $832,750 in most U.S. counties. Any mortgage above that threshold is a jumbo loan by definition. If you are buying a high-value home or refinancing a large balance, understanding what is a jumbo loan and how it works is the first step toward a smart financing decision.

How do jumbo loans differ from conventional conforming loans?

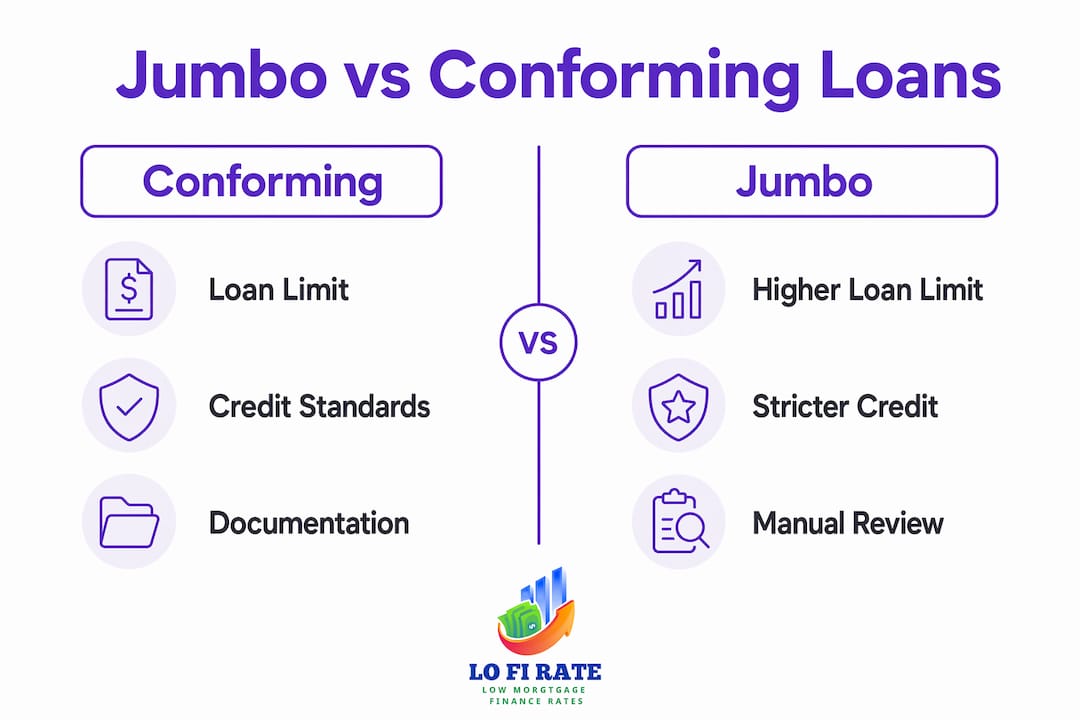

A jumbo mortgage operates under entirely different rules than a conventional conforming loan. The core difference is who bears the risk. Conforming loans can be sold to Fannie Mae or Freddie Mac, which transfers risk away from the original lender. Jumbo loans cannot be purchased by either government-sponsored enterprise, so the lender holds the full risk on its books.

That risk exposure changes everything about how lenders underwrite these loans. Credit standards are tighter, documentation requirements are more thorough, and reserve requirements are higher. A borrower who qualifies easily for a $700,000 conforming loan may face a very different process when applying for an $850,000 jumbo mortgage.

| Feature | Conforming loan | Jumbo loan |

|---|---|---|

| 2026 loan limit | Up to $832,750 (most counties) | Above $832,750 |

| Fannie Mae / Freddie Mac eligible | Yes | No |

| Minimum credit score (typical) | 620+ | 700+ |

| Typical down payment | 3%–5% | 10%–20% |

| Underwriting type | Automated | Often manual |

| Cash reserve requirement | Low to moderate | High |

The underwriting difference is significant. Conforming loans run through automated systems like Fannie Mae's Desktop Underwriter. Jumbo loans frequently go through manual underwriting, where a human reviewer examines every line of your financial picture. That process rewards borrowers who arrive with clean, organized files.

Key distinctions borrowers should know:

- Luxury properties are harder to sell quickly in foreclosure, which increases lender risk and drives stricter requirements.

- Debt-to-income ratios for jumbo loans are typically capped lower than for conforming loans.

- Lenders may require 6–12 months of mortgage payments held in reserve after closing.

- Lenders set their own upper caps on jumbo loan size, ranging from $2 million to $5 million or more depending on the institution.

Pro Tip: Before you apply, check whether your target property falls under a conforming or jumbo threshold. A loan that is $1 over the limit triggers the full jumbo process, so a larger down payment could sometimes keep you in conforming territory.

What are the 2026 conforming loan limits?

The FHFA adjusts conforming loan limits each year based on home price data. For 2026, the high-cost area ceiling for a single-family home reaches $1,249,125. That means buyers in expensive markets like San Francisco, New York City, or Honolulu have a higher threshold before their mortgage becomes a jumbo loan.

Location determines your limit. A $900,000 mortgage in rural Ohio is a jumbo loan. That same $900,000 mortgage in Los Angeles County is not, because the local conforming limit exceeds that amount. Your property's county directly controls which limit applies, and buyers are often surprised to learn their loan type depends on a ZIP code.

| Property type | Baseline limit (most counties) | High-cost area limit |

|---|---|---|

| 1-unit (single-family) | $832,750 | $1,249,125 |

| 2-unit | $1,066,650 | $1,599,975 |

| 3-unit | $1,289,150 | $1,933,725 |

| 4-unit | $1,602,150 | $2,403,225 |

Multi-unit properties carry higher conforming limits. A borrower buying a duplex in a standard-cost county can borrow up to $1,066,650 before crossing into jumbo territory. This matters for investors and house-hackers who buy two to four-unit properties.

The FHFA publishes a full county-by-county lookup tool on its website. Checking your specific county before you shop for a home takes less than two minutes and can change your entire financing strategy. Understanding types of mortgage loans available in your market helps you see where jumbo fits relative to other options.

What does qualifying for a jumbo loan require?

Qualifying for a jumbo mortgage is more demanding than qualifying for a conventional loan. Lenders apply stricter standards because they carry the full credit risk. Borrowers need excellent credit, often a score of 700 or above, along with a low debt-to-income ratio and documented financial stability.

The qualification process typically involves these steps:

- Credit score review. Most lenders require a minimum score of 700. Some require 720 or higher for larger loan amounts. A single late payment in the past 12 months can complicate approval.

- Debt-to-income ratio check. Lenders generally want your total monthly debt payments to stay below 43% of gross monthly income. Many prefer 38% or lower for jumbo loans.

- Down payment verification. Wells Fargo requires as little as 10.01% down for jumbo loans, but 20% is the industry standard. A larger down payment reduces lender risk and often improves your rate.

- Cash reserve documentation. Lenders want to see liquid assets covering 6–12 months of principal, interest, taxes, and insurance after closing. These reserves prove you can weather financial disruption.

- Income documentation. Expect to provide two years of tax returns, W-2s or 1099s, recent pay stubs, and bank statements. Self-employed borrowers typically face additional scrutiny.

- Appraisal. High-value homes often require two independent appraisals to confirm market value, since comparable sales data can be thin in luxury markets.

Manual underwriting is common in jumbo approvals. A well-organized file with consistent income history, clearly sourced assets, and no unexplained large deposits moves through underwriting faster and with fewer conditions. Approval depends as much on documentation quality as on the loan amount itself.

Pro Tip: Prepare an "underwriter-ready" package before you apply. This means a cover letter explaining any income gaps, a 24-month history of all bank accounts, and a written explanation for any large deposits. Lenders reward borrowers who make their job easier.

Reviewing a mortgage qualification guide before you start the process gives you a clear picture of what lenders expect at each stage.

What are the costs, rates, and benefits of jumbo loans?

Jumbo loan interest rates have shifted considerably over the past decade. Jumbo mortgage rates now often match or undercut conventional conforming rates, reversing the historical pattern where jumbo loans always cost more. This happens because jumbo borrowers tend to have strong credit profiles, making them lower default risks despite the larger loan size.

That said, rates vary more widely across lenders for jumbo loans than for conforming loans. Because no secondary market standardizes pricing, each lender prices jumbo risk independently. Shopping three to five lenders can produce meaningfully different rate quotes on the same loan amount.

Key cost and benefit factors for jumbo borrowers:

- Closing costs are typically higher in dollar terms because many fees scale with loan size. Origination fees, title insurance, and appraisal costs all run larger on a $1.2 million loan than on a $500,000 loan.

- Private mortgage insurance (PMI) is generally not required on jumbo loans, even with less than 20% down. Lenders use higher down payment requirements instead of PMI to manage risk.

- Tax considerations changed after the Tax Cuts and Jobs Act of 2017. The mortgage interest deduction is now capped at interest paid on the first $750,000 of mortgage debt for loans originated after december 15, 2017. Borrowers financing above that threshold should consult a tax advisor.

- Financing flexibility is a real benefit. A jumbo loan lets you purchase a high-value home with a single mortgage rather than combining a conforming loan with a second lien, which simplifies your payment structure.

- Lender variability is a risk. Because jumbo loans are portfolio products held by individual lenders, terms, rates, and requirements differ significantly from one institution to the next. Comparing lenders before committing is not optional. It is the single most effective way to reduce your total borrowing cost.

Key takeaways

A jumbo loan is defined as any mortgage exceeding the FHFA conforming loan limit for that year and county, requiring stricter credit, larger down payments, and manual underwriting because Fannie Mae and Freddie Mac cannot buy these loans.

| Point | Details |

|---|---|

| 2026 jumbo threshold | Loans above $832,750 in most counties qualify as jumbo; high-cost areas reach $1,249,125. |

| No GSE backing | Fannie Mae and Freddie Mac cannot purchase jumbo loans, so lenders hold full credit risk. |

| Credit and income standards | Borrowers typically need a 700+ credit score, low debt-to-income ratio, and 6–12 months of reserves. |

| Down payment expectations | Industry standard is 20% down, though some lenders accept as little as 10.01%. |

| Rate competitiveness | Jumbo rates now often match or beat conforming rates, but vary widely across lenders. |

The part most buyers miss about jumbo loans

Most articles on jumbo loans focus on the threshold number. That is the wrong place to focus. The real issue is lender variability. Because jumbo loans never touch Fannie Mae or Freddie Mac, every lender prices and underwrites them differently. I have seen two borrowers with nearly identical profiles receive rate quotes that differed by more than half a percentage point on the same loan amount. On a $1.2 million mortgage, that gap costs tens of thousands of dollars over the life of the loan.

The second thing buyers underestimate is how much documentation preparation matters. Jumbo underwriting is personal. A human reviewer reads your file. If your income looks inconsistent across your tax returns and bank statements, you will get conditions and delays. If your file tells a clean, consistent story, you close faster and often at better terms.

My honest advice: treat jumbo loan shopping like a negotiation, not an application. Get quotes from at least three lenders, including wholesale brokers who access multiple lenders at once. Retail banks price for their own margins. Wholesale channels price for competition. That difference is real and measurable.

The buyers who overpay on jumbo loans are almost always the ones who went with the first lender they spoke to. The ones who save are the ones who treated rate comparison as a non-negotiable step in the process.

— LoFi

How Lofirate helps jumbo loan borrowers find better rates

Financing a high-value home means every fraction of a percentage point on your rate matters. Lofirate connects borrowers with licensed wholesale mortgage brokers who shop multiple lenders at once, rather than offering a single retail rate from one institution.

Wholesale brokers have access to lender pricing that retail bank branches do not advertise. For jumbo borrowers, that access can translate to a meaningfully lower rate on a large loan balance. Lofirate does not lend money or quote rates directly. It matches you with a licensed broker in your state for a no-obligation consultation. Whether you are purchasing a luxury home or refinancing an existing jumbo mortgage, explore your loan options or connect with a broker through Lofirate to see what competitive wholesale pricing looks like for your situation.

FAQ

What is a jumbo loan in simple terms?

A jumbo loan is a mortgage that exceeds the FHFA conforming loan limit for your county, which is $832,750 in most U.S. counties for 2026. Because it exceeds that limit, it cannot be sold to Fannie Mae or Freddie Mac.

What credit score do you need for a jumbo mortgage?

Most lenders require a credit score of at least 700 for jumbo loan approval, with some requiring 720 or higher for larger balances. Strong credit signals lower default risk on a loan the lender must hold in its own portfolio.

How much do you need to put down on a jumbo loan?

The industry standard down payment for a jumbo loan is 20%, though some lenders accept as little as 10.01% down. A larger down payment reduces lender risk and can improve your interest rate.

Are jumbo loan rates higher than conventional rates?

Jumbo mortgage rates historically ran higher than conforming rates, but they now frequently match or beat conventional loan rates. Rates vary significantly across lenders, so comparing multiple quotes is the most reliable way to find the best pricing.

Does every county have the same jumbo loan threshold?

No. The FHFA sets county-specific conforming loan limits, with high-cost areas like San Francisco and Honolulu reaching $1,249,125 for a single-family home in 2026. A loan that is jumbo in one county may be conforming in another.