TL;DR:

- Principal is the original loan amount, while interest is the fee charged on that amount for borrowing. Most payments initially go toward interest, with the balance shifting to principal over time through amortization. Making extra payments toward principal reduces total interest paid and shortens the loan term.

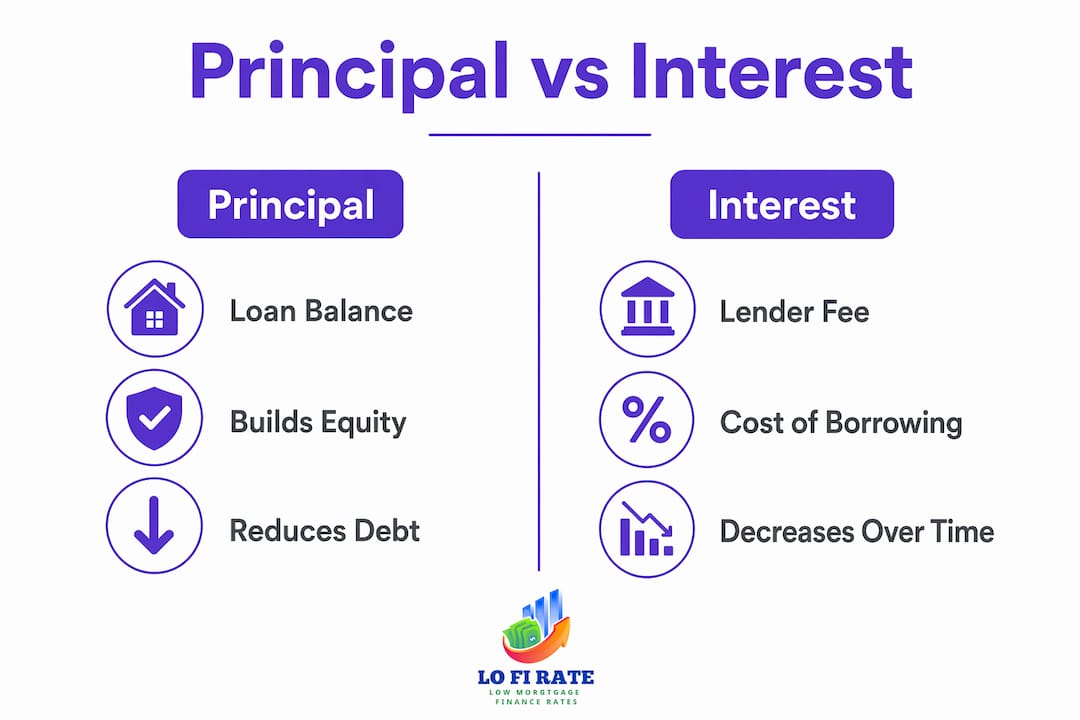

Principal is the original amount you borrow from a lender, and interest is the fee the lender charges for lending you that money. Together, these two components make up the core of every mortgage payment you make. Understanding what is principal vs interest is not just a terminology exercise. It determines how much your loan actually costs, how long it takes to pay off, and where every dollar of your monthly payment goes. Most homebuyers focus on the monthly payment amount without realizing how that figure is split between these two very different obligations.

What is principal vs interest in a mortgage payment?

Principal and interest are the two core components of a mortgage payment. The principal is the loan balance you must repay over time. The interest is the lender's charge for giving you access to that money, expressed as a percentage of the remaining balance.

Think of it this way: if you borrow $400,000 to buy a home, that $400,000 is your principal. Every month, the lender calculates interest on whatever balance remains unpaid. As you pay down the principal, the interest charge shrinks because it applies to a smaller number.

The differences between principal and interest go beyond definitions. Principal repayment builds your equity in the home. Interest payments do not. Every dollar of interest you pay is a cost, not an investment. That distinction shapes every smart mortgage decision you will ever make.

Your monthly payment also includes what lenders call PITI: Principal, Interest, Taxes, and Insurance. Taxes and insurance sit in a separate escrow account and do not reduce your loan balance. Confusing these four components is one of the most common mistakes homebuyers make when reading their mortgage statements.

How does amortization split your payments over time?

Amortization is the process of spreading your loan repayment across a fixed schedule of equal monthly payments. The math behind it means your early payments are heavily weighted toward interest, not principal. This surprises most homebuyers when they see their first mortgage statement.

In the early years of a 30-year mortgage, the majority of each monthly payment covers interest because the outstanding principal balance is at its highest. As you pay down the balance month by month, the interest charge on that balance falls. More of each payment then goes toward principal. By the final years of the loan, the split flips almost entirely to principal repayment.

The table below shows how this shift looks across a typical 30-year mortgage.

| Loan year | Portion toward interest | Portion toward principal |

|---|---|---|

| Year 1 | High (majority of payment) | Low |

| Year 10 | Moderate | Growing |

| Year 20 | Declining | Majority |

| Year 30 | Minimal | Nearly all |

This structure is not accidental. Lenders design amortization schedules so they collect most of their interest income early in the loan term. That is why refinancing or selling a home in the first five to ten years often feels like you have made little progress on the actual balance. You have been paying mostly for the cost of borrowing, not the debt itself.

For a detailed mortgage payment breakdown with real numbers, the math becomes much clearer when you see it applied to specific loan amounts and rates.

Why does paying extra toward principal save you money?

Making additional principal-only payments reduces your outstanding balance faster and cuts the total interest you pay over the life of the loan. Because interest is calculated on the remaining balance, every dollar you knock off the principal today removes the interest that would have accrued on that dollar for every remaining month of the loan.

Paying a dollar off principal today eliminates the interest charge on that dollar for every subsequent month of the loan term. That compounding benefit grows the earlier in the loan you make the extra payment. A $200 extra payment in year two saves far more in total interest than the same $200 paid in year twenty-five.

The benefits of extra principal payments include:

- Shorter loan term. Reducing the balance faster means you reach payoff ahead of schedule.

- Lower total interest paid. Less balance outstanding means less interest accruing each month.

- Faster equity growth. A lower principal balance means a higher ownership stake in your home.

- Reduced financial risk. Lower debt gives you more flexibility if your income changes.

Before making extra payments, check your loan agreement. Some lenders have prepayment policies that affect how and when you can apply extra funds. Most standard mortgages today allow extra principal payments without penalty, but verifying this first protects you from surprises.

Pro Tip: Always specify "principal only" when making an extra payment. Contact your lender's online portal or write it on the memo line of a check. Without that designation, the lender may apply the extra amount toward next month's interest or escrow instead of reducing your balance.

For more ways to reduce what you owe over time, the smart ways to save on your mortgage guide covers practical strategies that go beyond extra payments.

What are the main interest calculation methods?

Not all loans calculate interest the same way. The method your lender uses directly affects how much benefit you get from extra principal payments. Knowing which method applies to your loan is one of the most overlooked steps in mortgage management.

Lenders calculate interest using two primary methods: daily simple interest and precomputed interest. Each works differently and produces different outcomes when you make extra payments.

- Identify your loan type. Check your loan agreement or closing disclosure for the phrase "simple interest" or "precomputed interest." This language tells you which method applies.

- Understand daily simple interest. This method calculates interest each day based on the current outstanding balance. Extra principal payments immediately reduce the balance and therefore reduce the next day's interest charge. Most standard mortgages use this method.

- Understand precomputed interest. This method calculates the total interest for the entire loan term upfront and builds it into the payment schedule. Loans using precomputed interest do not benefit as much from early principal payments because the interest is already fixed.

- Verify payment application rules. Ask your lender directly how extra payments are applied. Get the answer in writing or find it in your loan agreement. This step prevents your extra payment from going to the wrong place.

- Check for prepayment terms. Some loan agreements include rules about when and how you can make extra payments. Confirm there are no fees or restrictions before sending additional funds.

Understanding your loan's interest calculation method is the foundation of knowing whether your extra payments will actually save you money. Skipping this step is one of the most costly oversights a homebuyer can make.

Common mistakes borrowers make with principal and interest

The biggest mistake borrowers make is assuming every extra payment automatically reduces their principal. Extra payments not explicitly marked as principal-only are often credited toward next month's interest or escrow instead. The balance does not drop, and the interest savings never materialize.

A second common mistake is confusing the interest rate with the APR. The interest rate differs from the APR because the APR includes additional fees and points, giving a fuller picture of the true cost of borrowing. Comparing loans using only the interest rate can lead you to choose a loan that costs more overall.

Common errors to avoid:

- Sending extra money without a designation. Always label extra payments as principal-only through your lender's portal or payment form.

- Ignoring the escrow portion. Taxes and insurance fluctuate annually. A change in your escrow amount can raise your total monthly payment even if your principal and interest stay the same.

- Making late payments. On daily simple interest loans, a late payment means more days of interest accrue before the payment is applied. This increases your interest cost for that month.

- Assuming all loans work the same. Precomputed interest loans and simple interest loans respond very differently to extra payments. Treating them the same leads to wasted effort.

Pro Tip: Log into your lender's online portal after making any extra payment. Confirm the payment was applied to principal, not to a future payment or escrow. This takes two minutes and can save you from months of misdirected payments.

For a full breakdown of mortgage terminology explained, including how escrow, PITI, and amortization all connect, that resource covers the complete picture in plain language.

Key Takeaways

Understanding the split between principal and interest is the single most important step toward controlling the total cost of your mortgage.

| Point | Details |

|---|---|

| Principal builds equity | Every dollar applied to principal reduces your loan balance and increases your ownership stake. |

| Interest front-loads costs | Early mortgage payments are mostly interest; the shift toward principal grows over time through amortization. |

| Label extra payments clearly | Unmarked extra payments may go to interest or escrow, not principal. Always designate them as principal-only. |

| Loan type changes the math | Daily simple interest loans benefit more from extra payments than precomputed interest loans. |

| APR shows the full cost | The interest rate alone does not capture fees and points. Use APR to compare loans accurately. |

What I have learned from watching borrowers manage their mortgages

Most homebuyers spend more time choosing a paint color than reading their amortization schedule. That is not a criticism. Mortgage documents are long and written for lawyers, not homeowners. But the cost of that gap is real and measurable.

The insight that changes how most people think about their mortgage is this: you are renting money. Every month you carry a balance, you pay rent on it in the form of interest. The faster you reduce the balance, the less rent you owe. That framing makes extra principal payments feel less like sacrifice and more like getting out of a lease early.

What I have seen consistently is that borrowers who review their mortgage statement monthly, even briefly, catch problems faster. They notice when an extra payment was misapplied. They see when their escrow adjustment raised their payment. They understand why their balance is not dropping as fast as they expected. That awareness is worth more than any single financial tip.

The other thing worth saying directly: the difference between a loan that costs you $180,000 in interest and one that costs $220,000 is often not the rate. It is how you manage the principal. Checking whether your loan uses daily simple interest, designating extra payments correctly, and making even one extra payment per year adds up to a meaningful difference over a 30-year term. The math is not complicated. The discipline is.

— LoFi

How Lofirate helps you find the right mortgage structure

Knowing how principal and interest work is only useful if you have a loan structured to take advantage of that knowledge. The rate you start with determines how much of every payment goes to interest from day one.

Lofirate connects homebuyers and homeowners with licensed wholesale mortgage brokers who shop multiple lenders to find competitive rate options. Retail lenders offer only their own pricing. Wholesale brokers access a wider market, which often means a lower starting rate and less interest paid over the life of the loan. Whether you are purchasing a home or refinancing, you can request a broker consultation through Lofirate with no obligation. A lower rate means more of every payment goes to principal from the start. That is the most effective way to put what you have learned here to work.

FAQ

What is the difference between principal and interest?

Principal is the original amount you borrowed. Interest is the fee the lender charges for lending you that money, calculated as a percentage of the remaining balance.

Why do early mortgage payments mostly cover interest?

Early payments cover mostly interest because the outstanding principal balance is at its highest point. As the balance falls through amortization, the interest portion of each payment shrinks.

How does a principal-only payment work?

A principal-only payment is an extra payment designated specifically to reduce your loan balance, not cover interest or escrow. You must label it as principal-only through your lender's portal or payment form.

Does the interest calculation method matter for extra payments?

Yes. Daily simple interest loans benefit immediately from extra principal payments because interest recalculates on the new lower balance. Precomputed interest loans do not respond the same way.

What is PITI and how does it relate to principal and interest?

PITI stands for Principal, Interest, Taxes, and Insurance. Taxes and insurance sit in a separate escrow account and do not reduce your loan balance. Only the principal and interest portions of your payment affect what you owe on the loan.