TL;DR:

- Discount points are prepaid fees to lower your mortgage interest rate, typically costing 1% of the loan and reducing rates by about 0.125% to 0.25%. They can save you money over time but only if you stay in your home long enough to recoup the upfront cost. Buying points makes sense for long-term homeowners who can afford the initial expense and plan to hold the property beyond the break-even period.

Discount points are prepaid interest fees that homebuyers pay at closing to permanently lower their mortgage interest rate. Each point costs 1% of the loan amount and reduces the rate by approximately 0.125% to 0.25%. On a $300,000 loan, one point costs $3,000. On a $600,000 loan, that same point costs $6,000. The result is a lower monthly payment and less total interest paid over the life of the loan. Understanding what are discount points, and whether buying them makes sense for your situation, is one of the most financially significant decisions you will make at the closing table.

What are discount points and how do they work?

Discount points, also called mortgage points, are a form of prepaid interest. You pay them upfront at closing in exchange for a reduced interest rate on your loan. The industry term is "discount points," and lenders list them on your Loan Estimate under closing costs.

One point equals 1% of your loan principal. Paying one point on a $400,000 mortgage costs $4,000 at closing. That payment buys down your rate by roughly 0.25%, though the exact reduction depends on the lender and loan type. Fractional points are also common. You might pay 0.5 points or 1.5 points depending on how much you want to reduce the rate.

The key distinction is between discount points and origination fees. Origination fees are what lenders charge to process your loan. They do not reduce your interest rate. Discount points are specifically purchased to lower the rate. Both appear on your Loan Estimate, so read the line items carefully before assuming any fee is buying you a better rate.

How do discount points lower your monthly payment?

The math behind mortgage points is straightforward. A lower interest rate means a smaller monthly payment, and that savings compounds over a 30-year loan term.

Here is a concrete example using a $400,000 loan at a 7.0% rate on a 30-year fixed mortgage:

- Base payment at 7.0%: approximately $2,661 per month.

- Pay one point ($4,000) to reduce the rate to 6.75%.

- New payment at 6.75%: approximately $2,594 per month.

- Monthly savings: roughly $67 per month.

- Annual savings: approximately $804 per year.

The upfront cost is real and immediate. The savings accumulate slowly over time. That gap between what you pay now and what you save later is the core tension every homebuyer must resolve.

Lenders do set limits on how many points you can purchase. Most cap the rate reduction at a level that still keeps the loan profitable for them. Buying three or four points is possible with some lenders, but the rate reduction per point varies significantly based on market conditions, loan type, and your credit profile. The common 0.25% per point is a rule of thumb, not a guarantee.

Pro Tip: Ask your lender for a side-by-side comparison showing your rate and payment with zero points, one point, and two points. That single document makes the trade-off concrete and easy to evaluate.

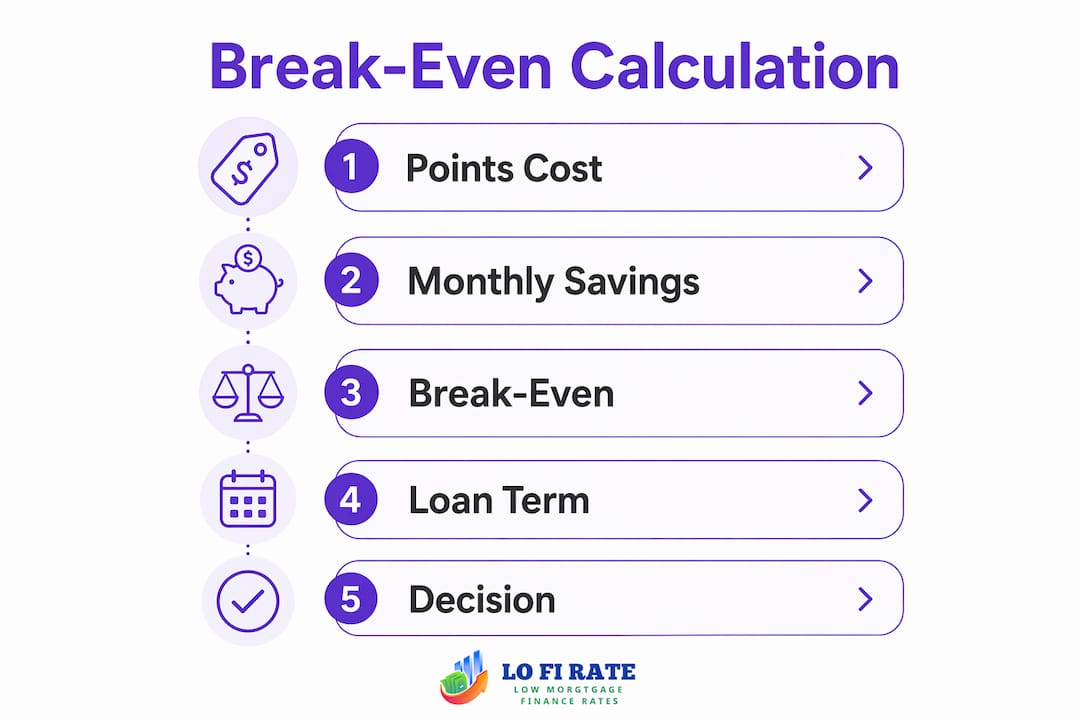

How to calculate the break-even point

The break-even point is the number of months it takes for your monthly savings to recover the upfront cost of the points. The formula is simple: divide the total cost of the points by the monthly savings.

Using the example above, paying $4,000 for points that save $67 per month produces a break-even of approximately 60 months, or five years. If you stay in the home longer than five years, you come out ahead. If you sell or refinance before that, you lose money on the points.

The break-even calculation from the research pool confirms this dynamic directly. Paying $3,000 for points that save $48 per month results in a break-even of approximately 63 months. That is just over five years. The implication is clear: points reward patience and long-term ownership.

| Scenario | Points cost | Monthly savings | Break-even period |

|---|---|---|---|

| $300,000 loan, 1 point | $3,000 | $48/month | ~63 months (5.25 years) |

| $400,000 loan, 1 point | $4,000 | $67/month | ~60 months (5 years) |

| $600,000 loan, 1 point | $6,000 | $100/month | ~60 months (5 years) |

Two factors complicate the break-even math. First, if your down payment is under 20%, you are likely paying private mortgage insurance. PMI costs can offset the interest savings from points, making the purchase less effective than it appears. Second, the cash you spend on points is cash you no longer have for repairs, emergencies, or investments. That opportunity cost is real even if it does not show up in the monthly payment comparison.

Pro Tip: Use a mortgage payment calculator to model your specific loan amount, rate, and points cost before committing. Generic examples are useful for learning; your actual numbers are what matter.

How do discount points compare to lender credits?

Discount points and lender credits sit on opposite ends of the same trade-off. Points increase upfront costs to lower your rate. Lender credits reduce your upfront costs but increase your rate. Neither is universally better. The right choice depends on how long you plan to stay in the home and how much cash you have at closing.

| Feature | Discount points | Lender credits | Origination fees |

|---|---|---|---|

| Effect on closing costs | Increases | Decreases | Increases |

| Effect on interest rate | Lowers | Raises | None |

| Best for | Long-term owners | Short-term owners or cash-limited buyers | Covers lender processing costs |

| Payback period | 5+ years typically | Immediate relief | No payback; sunk cost |

Origination fees occupy a separate category. They compensate the lender for underwriting and processing your loan. They do not buy down your rate. Confusing origination fees with discount points is a common mistake that leads homebuyers to believe they are getting a rate reduction when they are not.

One underappreciated use of discount points is loan qualification. Buying points to reduce monthly payments can lower your debt-to-income ratio enough to meet a lender's qualification threshold. If your DTI is slightly above the limit, paying a point or two to reduce the payment may be the difference between approval and denial.

When should homebuyers consider buying discount points?

Buying discount points makes the most financial sense in specific situations. The decision is not one-size-fits-all, and generic rules of thumb often mislead buyers.

Situations where buying points typically makes sense:

- You plan to stay in the home for at least five to seven years, giving you time to pass the break-even point.

- You have enough cash after closing to cover an emergency fund, repairs, and moving costs without stress.

- Current mortgage rates are high and you expect to hold the loan long-term rather than refinance soon.

- Your DTI ratio is close to the lender's limit and a lower monthly payment would help you qualify.

- You are buying a forever home or a property you intend to hold as a long-term rental.

Situations where buying points is usually a poor choice:

- You plan to sell within three to five years. Selling before the break-even period means you lose money on the points.

- You expect to refinance within a few years, which resets the loan and eliminates the rate you paid to buy down.

- Your cash reserves are thin. Spending $6,000 on points when you have $8,000 in savings leaves you financially exposed.

- You are putting down less than 20% and will pay PMI. The insurance cost can neutralize the savings from points.

The Consumer Financial Protection Bureau notes that rate reductions vary by lender, loan type, market, and borrower credit profile. No fixed standard applies. That means the only way to know the true value of points on your loan is to get a written Loan Estimate and compare scenarios side by side. Relying on averages or rules of thumb without your specific numbers is a mistake that costs real money.

Mortgage rate trends in 2026 also affect the calculus. When rates are elevated, the absolute dollar savings from a rate reduction are larger, which can shorten the break-even period and make points more attractive.

Key Takeaways

Discount points are a financial trade-off: you pay more upfront to pay less each month, and the decision only makes sense if you stay in the home long enough to recover the cost.

| Point | Details |

|---|---|

| Cost per point | One point costs 1% of the loan and typically reduces the rate by 0.125%–0.25%. |

| Break-even math | Divide the total points cost by monthly savings to find how long until you profit. |

| Long-term owners benefit most | Buyers staying five or more years are the strongest candidates for buying points. |

| PMI can offset savings | A down payment under 20% adds PMI costs that may cancel out the interest savings. |

| Points vs. lender credits | Points lower your rate at higher upfront cost; lender credits do the opposite. |

The part most buyers get wrong about discount points

Most homebuyers treat discount points as a simple yes-or-no question. They hear "buy points to get a lower rate" and either dismiss it as too expensive or assume it is always a good deal. Both reactions miss the point entirely.

The real question is not whether points are good or bad. The question is whether your break-even timeline aligns with your ownership plan. I have seen buyers pay $9,000 in points on a home they sold 18 months later. That is not a mortgage strategy. That is a $9,000 mistake.

The other thing buyers consistently underestimate is the cash-after-closing problem. Spending your reserves on points to save $70 a month sounds appealing until the water heater fails in month three. Points are only a good investment when your financial cushion is intact after paying them.

My honest advice: demand a written Loan Estimate showing your loan with and without points before you decide anything. If a lender cannot or will not produce that comparison, find one who will. The loan options available to you depend heavily on which lenders you actually compare. Wholesale mortgage brokers, in particular, can shop multiple lenders and show you how points are priced across different loan products, which gives you real data instead of a single lender's pitch.

Points are a tool. Used correctly, they save you tens of thousands of dollars over a long loan term. Used carelessly, they drain your cash for a benefit you never collect.

— LoFi

How Lofirate helps you find the right mortgage rate

Paying discount points is only worth it if you start with a competitive base rate. If your lender's rate is already above market, buying points just brings you closer to where you should have started.

Lofirate connects homebuyers and homeowners with licensed wholesale mortgage brokers who shop multiple lenders to find competitive pricing. Retail lenders offer only their own rates. Wholesale brokers give you access to a wider market, which means a better starting point before you even consider buying points. Visit Lofirate's broker matching service for a no-obligation consultation and see what your loan actually costs across multiple lenders. A lower base rate changes every calculation in this article in your favor.

FAQ

What are discount points on a mortgage?

Discount points are upfront fees paid at closing to reduce your mortgage interest rate. One point costs 1% of the loan amount and typically lowers the rate by 0.125% to 0.25%.

Are discount points the same as origination fees?

No. Origination fees compensate the lender for processing your loan and do not reduce your interest rate. Discount points are specifically purchased to buy down the rate.

How do I know if buying points is worth it?

Divide the total cost of the points by your monthly payment savings. If the result in months is less than how long you plan to stay in the home, buying points is likely worth it.

Can discount points help me qualify for a mortgage?

Yes. Buying points reduces your monthly payment, which lowers your debt-to-income ratio. A lower DTI can help you meet a lender's qualification threshold when you are close to the limit.

What happens if I refinance before the break-even point?

You lose the money you paid for points. Refinancing resets your loan terms, so the rate you bought down no longer applies. Points are only profitable if you hold the loan past the break-even period.