TL;DR:

- Mortgage points are prepaid interest that lower your mortgage interest rate and monthly payments.

- Buying points can save thousands over the loan’s lifespan if you stay in the home beyond the breakeven period.

- Strategic evaluation, including lender comparisons and personal plans, is essential to maximize benefits from points.

Most homebuyers fixate on the down payment as the biggest lever they can pull to reduce mortgage costs. But there's another tool hiding in plain sight: mortgage points. Paying points upfront can meaningfully reduce your interest rate and save you tens of thousands of dollars over the life of a loan. The catch? Most buyers skip past this option without ever understanding what they're giving up. This article breaks down exactly what mortgage points are, how the math works in real scenarios, when buying points actually makes sense, and how to use them strategically in today's market.

Table of Contents

- What are mortgage points?

- How much do mortgage points save? A real-world breakdown

- Are mortgage points right for you? Key pros, cons & tax facts

- How to get the most value from mortgage points in 2026

- A smarter way to think about mortgage points in 2026

- Ready to put mortgage points to work for you?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Upfront cost for lower rate | Mortgage points let you pay more at closing to reduce your long-term interest rate. |

| Savings depend on your timeline | Points make more sense if you plan to keep the mortgage for several years to break even on the upfront cost. |

| Tax deduction potential | Mortgage points may be tax-deductible, but rules vary for purchases versus refinances. |

| Compare, negotiate, calculate | Always compare lenders, negotiate point costs, and calculate your breakeven before deciding. |

What are mortgage points?

Mortgage points, sometimes called discount points, are essentially prepaid interest. You pay a fee at closing in exchange for a lower interest rate on your loan. Think of it like buying down your rate before the loan even starts.

Here's the basic structure:

- One point equals 1% of your loan amount. On a $400,000 loan, one point costs $4,000.

- Points lower your interest rate, though by how much depends on the lender and market conditions.

- You can buy fractions of a point, such as 0.5 or 0.25, so the upfront cost is flexible.

- Points appear on your official loan documents, specifically your Loan Estimate and Closing Disclosure, under the "loan costs" section.

As mortgage points work in practice, they are prepaid interest listed on the Loan Estimate and Closing Disclosure, and you can purchase them in fractions. A 0.5 point on a $400,000 loan would cost $2,000. The rate reduction you get per point varies by lender and market conditions, typically falling somewhere in the 0.125% to 0.25% range per point.

Think of mortgage points like a coupon you buy at the door. The more you pay upfront, the cheaper every item (your monthly payment) becomes for the duration of your shopping trip (your loan term). The question is always whether you'll shop long enough to make the coupon worth its price.

Points are different from origination fees, which some lenders also charge at closing. Origination fees compensate the lender for processing the loan. Points, by contrast, are purely about buying a lower rate. Make sure you check your Loan Estimate carefully and separate these two line items.

Understanding mortgage rates more broadly will help you see where points fit into the bigger picture. Rates move based on economic conditions, your credit score, your loan type, and lender pricing. Points sit on top of that system as an optional lever you can pull at closing.

One important nuance: not every lender prices points the same way. One lender might give you a 0.25% rate reduction for one point. Another might only offer 0.125%. This inconsistency is exactly why shopping lenders matters just as much as deciding whether to buy points at all.

How much do mortgage points save? A real-world breakdown

Numbers make this concept click. Let's use a $400,000 loan at a baseline interest rate of 7.0% on a 30-year fixed mortgage.

| Scenario | Points purchased | Upfront cost | Interest rate | Monthly payment | Monthly savings |

|---|---|---|---|---|---|

| No points | 0 | $0 | 7.00% | $2,661 | Baseline |

| 1 point | 1 | $4,000 | 6.75% | $2,594 | $67/month |

| 2 points | 2 | $8,000 | 6.50% | $2,528 | $133/month |

With one point, you spend $4,000 at closing to save $67 per month. To figure out your breakeven point, divide the upfront cost by the monthly savings. In this case: $4,000 divided by $67 equals roughly 60 months, or about 5 years. If you stay in the home (and keep that loan) for more than 5 years, you come out ahead.

Here's how to think through it step by step:

- Get the rate quote with and without points from your lender in writing.

- Calculate the monthly savings by subtracting the lower payment from the baseline.

- Divide the upfront cost by the monthly savings to find your breakeven in months.

- Compare that to how long you realistically plan to stay in the home.

- Factor in refinancing risk: if rates drop and you refinance before breakeven, you lose the upfront investment.

Keep in mind that rate reductions per point vary by lender and market. The 0.25% reduction used above is not guaranteed. Some lenders in 2026 offer less per point, which stretches the breakeven further. This is why comparing mortgage rates across multiple lenders is essential before committing to points.

The breakeven point is your single most important number when evaluating mortgage points. If you can't confidently answer how long you'll stay in the home, buying points is a gamble, not a strategy.

Also worth noting: the more points you buy, the less benefit you get per point in many cases. Comparing lenders side by side helps you spot which lender offers the most rate reduction per dollar spent on points.

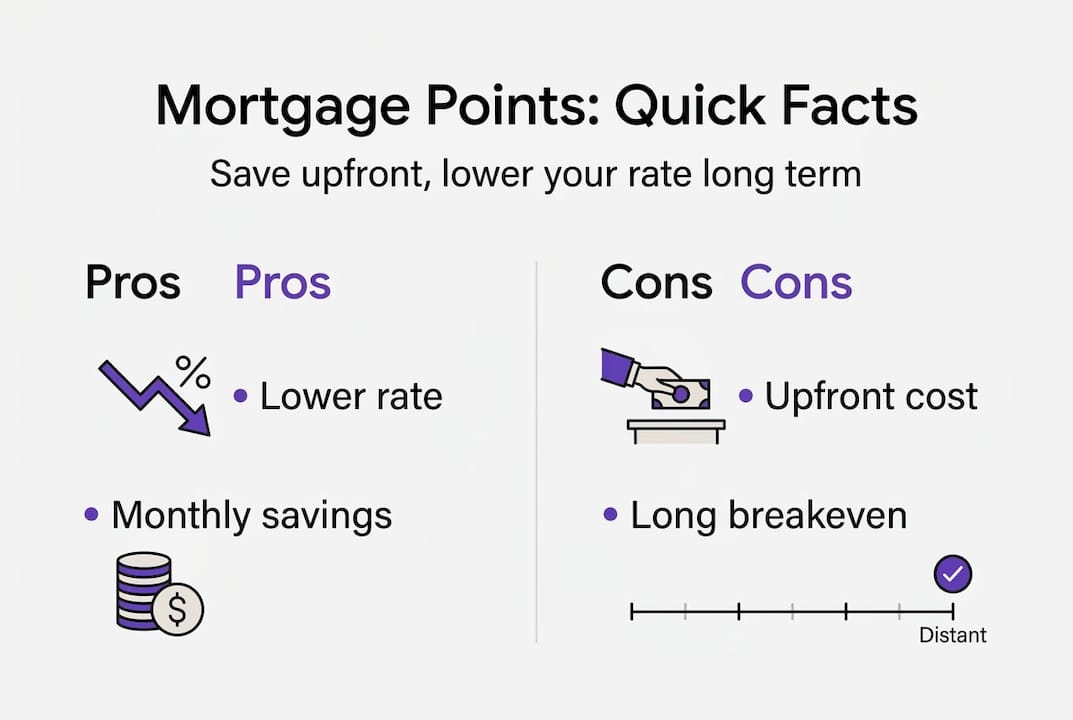

Are mortgage points right for you? Key pros, cons & tax facts

Let's get honest about both sides.

Advantages of buying points:

- Lower interest rate means a lower monthly payment for the life of the loan.

- Over 30 years, the savings can reach $20,000 to $40,000 or more on a larger loan.

- Points may qualify as a tax deduction, which partially offsets the upfront cost.

- A lower rate also reduces the total interest paid, building equity faster.

Drawbacks to consider:

- You need cash at closing, which competes with your down payment, reserves, and other costs.

- If you sell or refinance before hitting the breakeven, you lose money.

- Opportunity cost is real: that same cash invested elsewhere might earn more.

- Not every lender offers the same value per point, so the benefit isn't consistent.

Now for the tax piece. Points are tax-deductible as prepaid interest if you itemize your deductions. For a primary home purchase, points can often be deducted in full in the year you paid them, provided you meet certain IRS conditions. For refinances, the deduction is spread over the life of the loan.

| Situation | Deduction timing | Key IRS condition |

|---|---|---|

| Home purchase | Full deduction in year paid | Paid from own funds, not loan proceeds |

| Refinance | Amortized over loan life | Spread equally each year |

| Partial payoff/refinance | Remaining balance deductible at payoff | Applies when loan ends early |

According to IRS Publication 530, points qualify as prepaid interest deductions when they meet specific tests, including being calculated as a percentage of the principal and paid directly by the borrower. Always confirm your eligibility with a tax professional before planning your finances around this deduction.

Pro Tip: Don't count on the mortgage points tax deduction until a tax advisor confirms you qualify and that itemizing actually beats the standard deduction for your situation. Many borrowers assume they'll get the write-off and are surprised when the numbers don't add up.

Using a mortgage shopping checklist before you close can help you evaluate whether points fit your full financial picture. And if you're refinancing, read up on refinance tips to understand how points work differently in that context.

How to get the most value from mortgage points in 2026

In 2026's elevated rate environment, more borrowers are turning to points to lock in long-term savings. That demand has made it even more important to approach points strategically rather than reactively.

Here's a practical approach:

- Request rate sheets from multiple lenders. Ask specifically for pricing at various point levels so you can see the cost-per-rate-reduction comparison.

- Calculate your breakeven for each scenario, not just the no-points baseline. Sometimes 0.5 points beats 1 full point on a cost-per-savings basis.

- Weigh your cash alternatives. If you're at 18% down, using $4,000 for one point might make less sense than putting it toward the 20% threshold to eliminate PMI.

- Ask about lender credits, which are the opposite of points: you accept a higher rate in exchange for cash back at closing to cover fees.

- Negotiate. Lenders price points based on rate sheets that shift daily. Timing your lock and asking for flexibility can yield real savings.

As noted in smart mortgage strategies, in high-rate environments like 2026, points usage rises as borrowers seek to lock in savings, but the value per point decreases as you buy more. Don't over-invest in points past the point of diminishing returns.

Opportunity cost is a real consideration: money tied up in points is money not growing elsewhere. Compare your APR including points versus the no-points APR before deciding.

Pro Tip: Always compare loan offers using APR, not just the interest rate. APR folds in the cost of points, making it easier to compare two loans that appear similar on the surface.

Lender competition in 2026 is also a lever worth using. When lenders compete for your business, point pricing becomes negotiable. Wholesale brokers have access to multiple lender rate sheets simultaneously, which means they can surface the best point-to-rate tradeoff without you having to call a dozen lenders yourself. Before signing anything, review key broker questions to make sure you're getting the full picture.

A smarter way to think about mortgage points in 2026

Here's what most mortgage advice gets wrong about points: it frames the decision as binary. Buy them or don't. That framing misses the real opportunity.

The savvier approach is to treat points as one of several negotiation levers, not a fixed checkbox. In a competitive lending environment, you can sometimes negotiate a partial point reduction while also negotiating on rate, fees, or lender credits. The goal isn't the lowest rate in isolation. It's the best total cost structure for your specific situation and timeline.

Your breakeven isn't everyone's breakeven. A buyer who moves every five years should think about points very differently than someone who plans to stay for 20 years. A borrower with strong cash reserves approaches it differently than someone stretching to close. These aren't just financial distinctions. They reflect real life priorities.

The conventional wisdom says "buy points if you're staying long-term." That's true but incomplete. What it doesn't say is that working with mortgage brokers who have access to wholesale pricing can change the math entirely. If a broker gets you a lower base rate to begin with, the number of points needed to reach your target rate drops. Sometimes, the best use of your closing cash isn't points at all. It's finding a broker who gives you the pricing advantage retail lenders don't.

Ready to put mortgage points to work for you?

Understanding points is one thing. Applying them to your actual loan scenario is where the real savings happen.

At LoFiRate, we connect homebuyers and homeowners with licensed wholesale mortgage brokers who can show you exactly how points would perform with your loan amount, rate, and timeline. Unlike retail lenders limited to their own pricing, wholesale brokers shop multiple lenders to find the most competitive rate and point structure for your needs. Explore your loan options or get matched through our broker matching service for a no-obligation consultation. See what a second opinion on your mortgage can actually save you.

Frequently asked questions

How much does one mortgage point lower my rate?

One point typically lowers your rate by 0.125% to 0.25%, but the exact reduction varies by lender and current market conditions.

Are mortgage points tax-deductible?

Yes, points can be deducted as prepaid interest if you itemize. For home purchases, they are often fully deductible in the year paid, while refinance points are spread over the loan term.

When do mortgage points make sense financially?

Points make sense when your breakeven period, found by dividing upfront cost by monthly savings, is shorter than how long you plan to keep the loan. Always compare APR including points before deciding.

Can I buy partial points or only whole points?

You can buy points in fractions, such as 0.5 or 0.25 points, so you have flexibility in how much you pay upfront for a rate reduction.