TL;DR:

- FHA and conventional loans cater to different borrower profiles, affecting costs, eligibility, and property use choices. Borrowers should compare loan estimates, mortgage insurance policies, and long-term costs to select the best option based on credit score, down payment, and property type. Making an informed decision requires evaluating both short-term affordability and future refinance opportunities to minimize total mortgage costs.

FHA and conventional loans are the two primary mortgage pathways available to American homebuyers, each designed to serve a distinct borrower profile based on credit strength, down payment size, and property use. Understanding the role of FHA and conventional loans is not a formality. It is the decision that determines your monthly payment, your insurance costs, and how quickly you build equity. First-time buyers especially face this choice without a clear framework, and the wrong pick can cost thousands over the life of the loan.

What is the role of FHA and conventional loans in home financing?

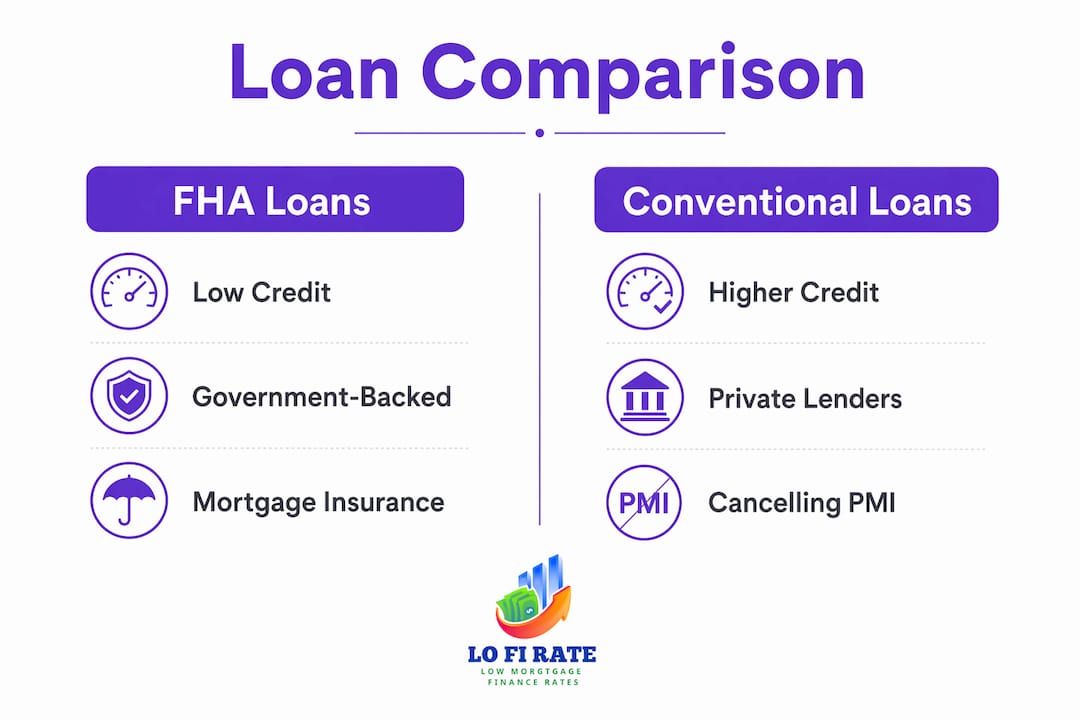

FHA loans are government-backed mortgages insured by the Federal Housing Administration, a division of the U.S. Department of Housing and Urban Development. Because the federal government absorbs the lender's risk if a borrower defaults, lenders can extend credit to buyers who would not qualify under stricter private standards. Conventional loans, by contrast, carry no government guarantee. They are funded and backed by private lenders, which means the lender takes on full default risk and compensates by requiring stronger borrower qualifications.

Both loan types exist to solve different access problems in the housing market. FHA loans opened homeownership to buyers with limited savings and imperfect credit histories. Conventional loans reward borrowers who have built strong financial profiles with lower long-term costs and more flexible property use. Neither is universally better. The right choice depends entirely on where you stand financially today and where you plan to be in five to ten years.

Conventional loans typically cost less than FHA loans over the life of the mortgage, but they are harder to qualify for due to stricter credit and down payment requirements. That cost gap is the central tension every borrower must resolve before signing a loan application.

How do FHA and conventional loans differ in eligibility?

The qualification gap between these two loan types is significant, and it starts with credit scores.

FHA loan eligibility:

- Credit scores as low as 500 are accepted, though scores below 580 require a 10% down payment

- Borrowers with scores of 580 or higher qualify with just 3.5% down

- Debt-to-income (DTI) ratios up to 57% are sometimes approved with compensating factors

- The property must be your primary residence. FHA loans cannot be used for investment properties or vacation homes

Conventional loan eligibility:

- Most lenders require a minimum credit score of 620, though better rates appear above 740

- Down payments can be as low as 3% through programs like Fannie Mae's HomeReady or Freddie Mac's Home Possible

- DTI ratios are generally capped at 45% to 50%, with less flexibility for exceptions

- Conventional loans can finance primary residences, second homes, and investment properties

The property use distinction is one of the most overlooked differences in any FHA vs conventional loans comparison. If you plan to rent out a unit or purchase a vacation property, FHA financing is simply off the table. For first-time buyers purchasing a primary residence with limited savings, FHA's lower credit threshold and 3.5% down payment make it the more accessible path. For buyers with a 680 credit score and 10% saved, running the numbers on both options is worth the time before committing.

Pro Tip: Check your credit score before applying. A score of 580 versus 620 can shift you from FHA territory into conventional eligibility, which changes your insurance costs dramatically.

How does mortgage insurance work differently for each loan?

Mortgage insurance is where the true cost difference between these two loan types becomes clear. The structure, duration, and removal rules are fundamentally different, and most borrowers do not fully understand this until they are already locked in.

| Feature | FHA Loan (MIP) | Conventional Loan (PMI) |

|---|---|---|

| Upfront premium | 1.75% of loan amount at closing | None |

| Annual premium | 0.45% to 1.05% of loan balance | 0.20% to 2.00% depending on credit/LTV |

| Duration | 11 years or life of loan depending on LTV | Cancels automatically at 22% equity |

| Removal method | Automatic at 11 years (if original LTV ≤ 90%) or refinance required | Request cancellation at 20% equity or wait for automatic removal |

| Applies to | All FHA loans regardless of down payment | Only when down payment is under 20% |

FHA mortgage insurance premiums follow specific rules tied to your original loan-to-value ratio. If your original LTV was 90% or less, MIP cancels after 11 years. If you put down less than 10%, MIP stays for the life of the loan, which on a 30-year mortgage means 30 years of insurance payments. This is the detail that catches the most borrowers off guard.

Conventional PMI, by contrast, cancels automatically when your loan balance reaches 78% of the original purchase price. You can also request removal at 80%. That flexibility makes conventional loans significantly cheaper over time for borrowers who build equity steadily. The total monthly payment comparison must always include insurance costs, because FHA's lower interest rate can be fully offset by persistent MIP charges. Learn more about how mortgage insurance impacts rates before you finalize your loan choice.

Pro Tip: If you take an FHA loan and later build 20% equity, refinancing into a conventional loan is the standard method to eliminate MIP. Factor the cost of that future refinance into your total loan comparison today.

How do costs and interest rates compare between loan types?

Interest rates favor FHA loans on paper, but the full picture is more nuanced. Bankrate data from May 2026 shows the average 30-year FHA APR at 6.51% versus 6.63% for conventional loans. That 0.12 percentage point difference sounds small, but on a $350,000 loan it translates to roughly $28 less per month in interest alone.

| Cost Factor | FHA Loan | Conventional Loan |

|---|---|---|

| Average 30-year APR (May 2026) | 6.51% | 6.63% |

| Upfront MIP | 1.75% of loan | None |

| Ongoing insurance | Required for most borrowers | Cancels at 20% equity |

| Loan limits | Lower, varies by county | Higher, up to $806,500 in most areas |

| Appraisal standards | Stricter safety and condition requirements | Standard market value appraisal |

The appraisal process is another practical cost factor. FHA appraisals verify both market value and safety standards, which means a home with peeling paint, a broken handrail, or an aging roof can fail FHA appraisal and require repairs before closing. Sellers in competitive markets sometimes reject FHA offers for this reason, which reduces your negotiating position. Conventional appraisals focus on market value without the same condition checklist.

FHA loan limits are also lower than conventional loan limits, which matters in high-cost markets. If you need a loan above the FHA ceiling for your county, a conventional loan is your only conforming option. Understanding total mortgage fees across both loan types gives you a cleaner picture of true borrowing costs.

How do you decide which loan fits your situation?

Choosing between FHA and conventional financing comes down to four concrete factors. Work through each one before you speak to a lender.

-

Check your credit score. Borrowers with scores above 620 and a down payment of 10% or more should run conventional loan numbers first. Borrowers with scores above 620 and sizable down payments are often financially better off with a conventional loan because PMI cancels while FHA MIP may not.

-

Calculate your available down payment. If you have less than 5% saved and your credit score is under 620, FHA is likely your most accessible path. If you have 10% or more, conventional PMI costs drop sharply and the long-term math often favors going conventional.

-

Consider the property type. Investment properties and second homes require conventional financing. If you are buying a multi-unit property and plan to live in one unit, FHA allows up to four units as long as one is your primary residence.

-

Think about your five-year plan. If you plan to sell or refinance within five years, the upfront FHA MIP of 1.75% may not be worth paying. Conventional loans carry no upfront insurance premium, which reduces your break-even timeline.

-

Request Loan Estimates from at least three lenders. The CFPB recommends comparing official Loan Estimates rather than advertised rates because the true cost of each loan only appears in the standardized three-page document every lender is required to provide. Many borrowers skip multiple lender comparisons and cost themselves thousands as a result.

For a broader view of your options, the types of mortgage loans available in 2026 include programs beyond FHA and conventional that may fit specific buyer profiles. First-time buyers should also review homebuyer programs designed for first-timers before assuming FHA is the only low-barrier entry point.

Pro Tip: Ask each lender to quote you both an FHA and a conventional scenario side by side. The difference in total monthly payment, including insurance, often surprises borrowers who assumed one option was clearly cheaper.

Key takeaways

Choosing between FHA and conventional loans requires comparing credit score thresholds, mortgage insurance duration, total monthly costs, and property use rules before committing to either program.

| Point | Details |

|---|---|

| FHA access vs. conventional cost | FHA loans accept lower credit scores but carry persistent MIP that can last the life of the loan. |

| PMI cancels, MIP may not | Conventional PMI cancels at 20% equity; FHA MIP requires refinancing to remove if original LTV exceeded 90%. |

| Interest rates favor FHA slightly | FHA APR averaged 6.51% vs. 6.63% conventional in May 2026, but insurance costs often close that gap. |

| Property use limits FHA | FHA loans are restricted to primary residences; conventional loans cover investment and vacation properties. |

| Compare Loan Estimates, not ads | Official Loan Estimates from multiple lenders reveal true costs that advertised rates never show. |

What I've learned watching borrowers choose the wrong loan

Most borrowers who end up frustrated with their mortgage made the same mistake: they chose a loan type based on a single variable, usually the interest rate or the down payment requirement, without modeling the full cost over their expected ownership period.

I have seen buyers with 660 credit scores take FHA loans because the rate was slightly lower, only to realize three years later that their MIP will never cancel. They are now facing a refinance they did not plan for, with closing costs that erase the savings they thought they were getting. The math was never in their favor. They just did not run it.

The other pattern I see constantly is borrowers who assume FHA is the only option because their down payment is small. That is not always true. Some conventional programs allow 3% down, and if your credit score is above 680, the PMI rate on a conventional loan can be lower than FHA's MIP from day one. The second opinion mortgage approach exists precisely because the first quote you receive is rarely the best one.

Refinancing out of FHA into conventional is a legitimate strategy, but it works best when you plan for it upfront. If you know you will have 20% equity within four years based on your market and payment schedule, taking an FHA loan today and refinancing later can make sense. If you have no clear equity timeline, you may be paying MIP indefinitely.

The most underused tool in this entire process is the official Loan Estimate. Every lender must provide one within three business days of your application. It shows your rate, all fees, and your projected monthly payment including insurance. Request it from at least three lenders before you decide anything.

— LoFi

Find the right loan with Lofirate

Lofirate connects you with licensed wholesale mortgage brokers who can quote both FHA and conventional loan options across multiple lenders, not just one. Retail lenders show you their own pricing. Wholesale brokers shop the market on your behalf, which is how borrowers find rates and terms that a single bank visit cannot match. Whether you are a first-time buyer weighing your options or a homeowner considering a refinance to eliminate FHA mortgage insurance, Lofirate's broker matching service gives you a transparent, no-obligation starting point. You can also explore the full range of available loan options to see which programs fit your credit profile and goals before committing to any lender.

FAQ

What is the minimum credit score for an FHA loan?

FHA loans accept credit scores as low as 500, though borrowers with scores between 500 and 579 must put down at least 10%. Borrowers with scores of 580 or higher qualify with a 3.5% down payment.

Can FHA mortgage insurance be removed?

FHA MIP cancels automatically after 11 years only if your original loan-to-value ratio was 90% or less. If you put down less than 10%, MIP lasts for the life of the loan and requires refinancing into a conventional loan to remove it.

Which loan is better for first-time buyers?

FHA loans are more accessible for first-time buyers with lower credit scores or limited savings. Buyers with credit scores above 620 and at least 10% down should compare conventional loan costs directly, since PMI cancels and long-term costs are often lower.

Do conventional loans require mortgage insurance?

Conventional loans require private mortgage insurance (PMI) only when the down payment is below 20%. PMI cancels automatically when the loan balance reaches 78% of the original purchase price, making it a temporary cost rather than a permanent one.

How do I compare FHA and conventional loan offers accurately?

Request an official Loan Estimate from at least three lenders for each loan type you qualify for. The Loan Estimate includes the interest rate, all fees, and the projected monthly payment with insurance, giving you a true apples-to-apples comparison that advertised rates cannot provide.