Mortgage pre-approval confuses many first-time homebuyers who mistakenly believe it guarantees loan approval and secures their dream home. The reality is more nuanced. Pre-approval represents a lender's conditional commitment based on verified financial documents, but it's not a final approval. Understanding what pre-approval truly means, how it differs from pre-qualification, and why it matters can transform your homebuying journey from overwhelming to manageable. This guide breaks down the pre-approval process, clarifies common misconceptions, and shows you how to leverage it effectively when shopping for your first home.

Table of Contents

- Key takeaways

- Understanding what mortgage pre-approval means and involves

- Mortgage pre-approval versus pre-qualification: what you need to know

- Challenges first-time buyers face and how pre-approval helps clarify affordability

- Practical steps for first-time buyers to get pre-approved with confidence

- Get expert mortgage support at LO FI RATE

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Definition and purpose | Pre approval is a lender conditional commitment based on verified financial information that shows how much the lender is willing to lend, not a final loan approval. |

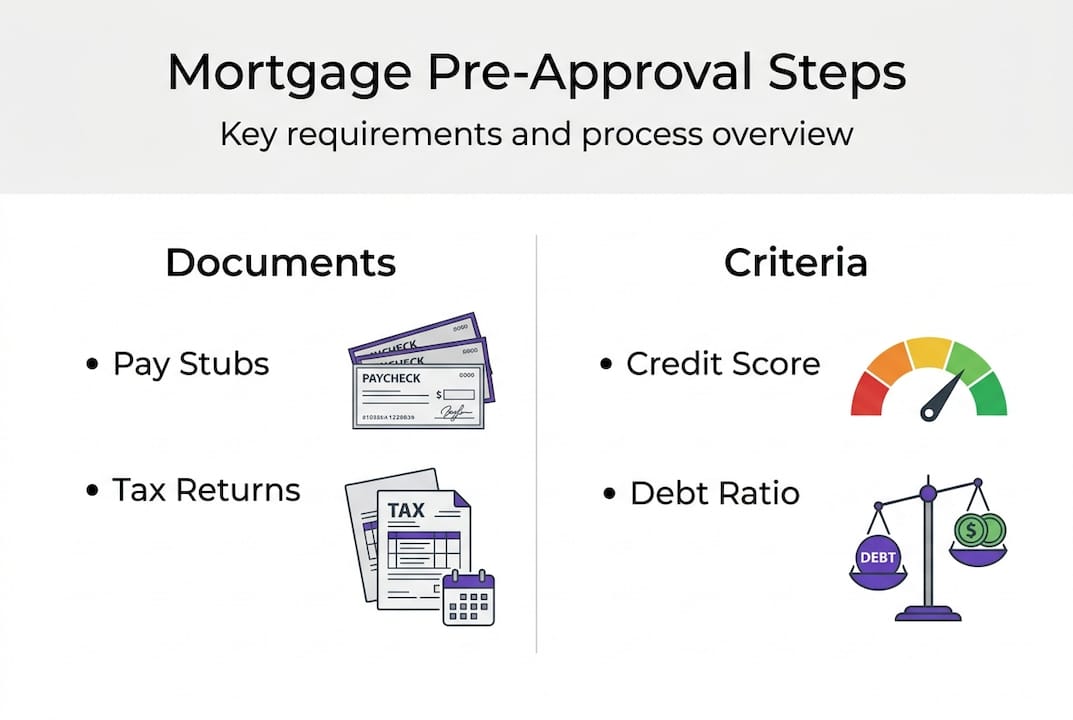

| Documentation requirements | You must submit pay stubs covering at least 30 days, W-2 forms from the past two years, federal tax returns for two years, and bank statements for the last two to three months, with self employed borrowers providing additional documents. |

| Credit inquiry impact | A hard credit inquiry accompanies the pre approval and can temporarily lower your score, though the impact usually fades within months. |

| Pre qualification vs approval | Pre qualification is an informal estimate based on self reported data with no verification, while pre approval uses verified documents and a hard check to issue a conditional commitment. |

| Not final guarantee | Final approval requires underwriting and confirmation that the property and your finances meet lender standards, so pre approval is not a guaranteed loan. |

Understanding what mortgage pre-approval means and involves

Mortgage pre-approval is a lender's conditional commitment based on verified financial information including income, assets, debts, and credit. Unlike casual estimates, pre-approval requires you to submit actual documentation proving your financial standing. Lenders examine your complete financial picture before issuing a pre-approval letter stating how much they're willing to lend.

The documentation requirements are substantial. You'll need recent pay stubs covering at least 30 days, W-2 forms from the past two years, federal tax returns for two years, and bank statements showing your savings and checking accounts for the last two to three months. Self-employed buyers face additional scrutiny, often needing profit and loss statements and business tax returns. These documents aren't optional suggestions but mandatory requirements that lenders verify independently.

Lenders evaluate what the industry calls the four Cs: capacity, capital, collateral, and credit. Capacity refers to your ability to repay based on income and employment stability. Capital means your savings, investments, and down payment funds. Collateral represents the property's value securing the loan. Credit encompasses your borrowing history, payment patterns, and overall creditworthiness. Each factor influences whether you receive pre-approval and at what interest rate.

The home loan application process includes a hard credit inquiry that temporarily impacts your credit score. This differs from soft inquiries used for pre-qualification. The hard pull appears on your credit report and may lower your score by a few points, though the effect typically diminishes within months. Multiple mortgage inquiries within a 45-day window usually count as a single inquiry, allowing you to shop rates without excessive score damage.

Pro Tip: Gather all required documents before contacting lenders to speed up the pre-approval process and demonstrate your seriousness as a buyer.

| Document category | Specific items needed | Purpose |

|---|---|---|

| Income verification | Pay stubs, W-2s, tax returns | Proves earning capacity and employment stability |

| Asset documentation | Bank statements, investment accounts | Confirms down payment funds and reserves |

| Debt obligations | Credit report, loan statements | Calculates debt-to-income ratio |

| Identity proof | Driver's license, Social Security number | Verifies borrower identity and eligibility |

Mortgage pre-approval versus pre-qualification: what you need to know

Pre-qualification represents an informal estimate based on self-reported financial information without document verification. You provide basic details about your income, debts, and assets, and the lender offers a rough estimate of what you might afford. No credit check occurs, and no verification happens. It's essentially an educated guess that carries minimal weight with sellers or real estate agents.

Pre-approval involves a formal application with verified documents and a hard credit check. The lender reviews your actual financial records, confirms employment, and assesses your creditworthiness through official channels. This process results in a conditional commitment letter specifying the loan amount, interest rate range, and loan type you qualify for. Sellers and agents recognize pre-approval as a serious step indicating you're a qualified buyer.

Despite its strength, pre-approval remains conditional and not guaranteed. Some sources call it a secret weapon for offers, while others warn it must still pass full underwriting. Final approval requires the lender to verify the specific property meets their standards, confirm your financial situation hasn't changed, and complete detailed underwriting. Job loss, new debts, or property issues can derail even solid pre-approvals.

| Feature | Pre-qualification | Pre-approval |

|---|---|---|

| Documentation | Self-reported information | Verified documents required |

| Credit check | Soft inquiry or none | Hard credit inquiry |

| Reliability | Rough estimate only | Conditional commitment |

| Seller perception | Minimal credibility | Strong buying signal |

| Processing time | Minutes to hours | Days to week |

First-time buyers often assume pre-approval guarantees loan funding, but it doesn't. They believe the pre-approved amount represents what they should spend, when it actually shows the maximum they could borrow. Many think pre-approval lasts indefinitely, yet it expires after 60 to 90 days. Understanding these distinctions prevents disappointment and helps you navigate the mortgage qualification guide more effectively.

Pro Tip: Request pre-approval rather than pre-qualification when you're ready to make offers, as sellers prioritize buyers with verified financing over those with casual estimates.

Challenges first-time buyers face and how pre-approval helps clarify affordability

Overall mortgage approval stands at 75.2%, while first-time buyer denial rates reach 14.1%. These statistics reveal that roughly one in seven first-time buyers faces rejection despite applying for financing. The gap between expectation and reality often stems from unrealistic affordability assumptions or undiscovered credit issues. Pre-approval exposes these problems early, giving you time to address them before finding your dream home.

First-time buyers typically make down payments averaging 7% rather than the traditional 20% many assume is mandatory. The median income for first-time buyers sits around $82,000, with typical credit scores near 728. These benchmarks help you gauge where you stand relative to successful buyers. If your credit score falls significantly below 728 or your income seems marginal for your target price range, pre-approval reveals whether you need to adjust expectations or improve your financial profile.

Debt-to-income ratios matter enormously in pre-approval decisions. Lenders typically prefer ratios below 43%, meaning your total monthly debt payments shouldn't exceed 43% of your gross monthly income. This includes your projected mortgage payment, property taxes, insurance, credit cards, car loans, and student loans. Pre-approval calculations show exactly how your existing debts limit your borrowing capacity, often surprising buyers who underestimated their debt burden.

Loan-to-value ratios determine how much lenders will finance relative to the property's value. Higher down payments mean lower loan-to-value ratios and often better interest rates. Pre-approval clarifies the connection between your available down payment and the home prices you can realistically afford. This prevents the heartbreak of falling in love with homes beyond your financial reach.

Pre-approval transforms vague homebuying dreams into concrete numbers and realistic timelines. Instead of guessing what you can afford, you know your maximum loan amount, approximate interest rate, and required down payment. This knowledge helps you search efficiently, focusing on properties within your verified price range. It also strengthens your negotiating position since sellers recognize pre-approved buyers as serious contenders less likely to face financing obstacles.

With 14.1% of first-time buyers facing mortgage denial, pre-approval serves as an early warning system that identifies potential obstacles before you invest time and emotion in properties you cannot ultimately finance.

Practical steps for first-time buyers to get pre-approved with confidence

Getting pre-approved requires systematic preparation and honest financial disclosure. Follow these steps to maximize your chances of securing strong pre-approval that accurately reflects your borrowing capacity.

-

Check your credit reports from all three bureaus and dispute any errors at least 60 days before applying. Mistakes happen frequently, and corrections take time to process through the system.

-

Gather required documents including pay stubs, tax returns, and W-2s that are current and complete. Missing or outdated paperwork delays the process and may result in conditional approvals requiring additional verification.

-

Calculate your debt-to-income ratio before applying to understand where you stand. Add all monthly debt payments and divide by your gross monthly income to see if you fall within acceptable ranges.

-

Research multiple lenders and compare their pre-approval requirements, interest rate ranges, and loan programs suited for first-time buyers. Don't assume all lenders offer identical terms or evaluate applications using the same criteria.

-

Submit complete applications to your chosen lenders within a concentrated timeframe to minimize credit score impact from multiple hard inquiries. Most scoring models treat inquiries within 45 days as a single event.

-

Review your pre-approval letter carefully, noting the loan amount, interest rate estimate, loan type, and expiration date. Ask questions about any terms or conditions you don't fully understand.

-

Maintain your financial status throughout the homebuying process by avoiding new debts, large purchases, or job changes that could invalidate your pre-approval. Lenders verify your finances again before closing.

Accurate financial disclosure matters more than presenting an idealized version of your situation. Lenders verify everything, and discrepancies raise red flags that can derail your application. If you have irregular income, employment gaps, or credit issues, explain them upfront rather than hoping they go unnoticed. Transparency builds trust and often leads to better outcomes than attempted concealment.

Pro Tip: Time your pre-approval to begin 90 days before you plan to start seriously shopping for homes, giving you maximum validity period without rushing your search or facing expired letters during negotiations.

Communicate regularly with your lender throughout the pre-approval process. Ask about specific underwriting criteria they emphasize, how they calculate debt-to-income ratios, and what circumstances might change your pre-approval status. Understanding their perspective helps you avoid actions that could jeopardize your financing. Questions to ask mortgage brokers should cover rate locks, fee structures, loan program options, and timeline expectations.

Get expert mortgage support at LO FI RATE

Navigating mortgage pre-approval and the broader homebuying process becomes significantly easier with expert guidance and access to competitive rates. LO FI RATE connects first-time buyers with licensed wholesale mortgage brokers who shop multiple lenders to find optimal rate options rather than limiting you to a single lender's pricing. This wholesale approach often reveals savings that retail lenders cannot match.

Whether you're just beginning to explore pre-approval or ready to compare loan options tailored for first-time buyers, the platform provides transparent, no-obligation consultations with licensed professionals in your state. Instead of navigating complex mortgage markets alone, you gain access to brokers who understand current mortgage rate trends for buyers and can explain how different loan programs impact your specific situation. The focus remains on simplicity, compliance, and helping you avoid overpaying for financing.

Frequently asked questions

Is mortgage pre-approval a loan guarantee?

No, pre-approval is conditional and not a final guarantee. Lenders must still complete full underwriting, verify the property meets their standards, and confirm your financial situation hasn't changed before issuing final approval. Job loss, new debts, or property appraisal issues can prevent closing even with strong pre-approval. Terms and rates may also adjust during final review based on updated information or market conditions.

What documents do I need for mortgage pre-approval?

You need pay stubs covering at least 30 days, W-2 forms from the past two years, federal tax returns for two years, and bank statements for two to three months. Self-employed buyers require additional documentation including profit and loss statements and business tax returns. Lenders may request supplementary materials like employment verification letters, explanations for credit issues, or documentation of other income sources depending on your specific financial situation.

How long does a mortgage pre-approval last?

Most pre-approvals remain valid for 60 to 90 days from the issue date. After expiration, you must reapply and provide updated financial documents for the lender to issue a new pre-approval letter. Significant changes to your financial situation during the validity period, such as job changes, new debts, or major purchases, may require earlier renewal or reassessment even before the expiration date.

Does mortgage pre-approval affect my credit score?

Yes, pre-approval requires a hard credit inquiry that may temporarily lower your score by a few points. The impact typically diminishes within several months as the inquiry ages. Multiple mortgage inquiries within a 45-day window usually count as a single inquiry under most credit scoring models, allowing you to shop rates with different lenders without compounding the score impact. Avoid applying for other new credit during your home search to minimize additional score effects.

Why is mortgage pre-approval important for first-time buyers?

Pre-approval clarifies your realistic budget and prevents wasting time on homes you cannot afford. It strengthens your offer credibility with sellers who prioritize buyers with verified financing over those without documentation. The process also identifies potential credit issues, debt problems, or documentation gaps early, giving you time to resolve them before finding a property. Pre-approved buyers often negotiate more effectively and close faster than those starting the financing process after making offers.