TL;DR:

- Knowing your full savings target, including down payment, closing costs, and buffer, is essential before buying a house. Automating transfers into a high-yield savings account ensures consistent progress without sacrificing your living standards. First-time buyers can benefit from assistance programs and careful planning to reduce their savings timeline and costs.

Saving for a house feels like running toward a finish line that keeps moving. Prices climb, rent eats your paycheck, and that down payment number looks impossibly large. But here is the truth: knowing exactly how to save for a house, with a clear target and the right system, changes everything. This guide breaks the entire process into concrete steps. You will learn what to actually save for, how to calculate your number, which accounts to use, which programs can reduce your burden, and how to stay on track without gutting your quality of life.

Table of Contents

- Key takeaways

- How to save for a house: understanding what you actually need

- Setting up a savings plan that actually works

- Strategies to accelerate your savings

- First-time buyer programs that reduce your savings target

- Tracking progress and avoiding costly mistakes

- My honest take on saving for a home

- Your mortgage rate matters as much as your down payment

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Know your full savings target | Budget for the down payment, closing costs, emergency fund, and a buffer for moving and repairs. |

| Automate before you spend | Set up automatic transfers on payday so saving happens without relying on willpower. |

| Use the right savings account | A high-yield savings account earning around 4% keeps your money safe, liquid, and growing. |

| Apply for assistance programs | Federal, state, and local programs can dramatically reduce your out-of-pocket requirement. |

| Track and adjust monthly | Review your progress every month and increase contributions when income rises. |

How to save for a house: understanding what you actually need

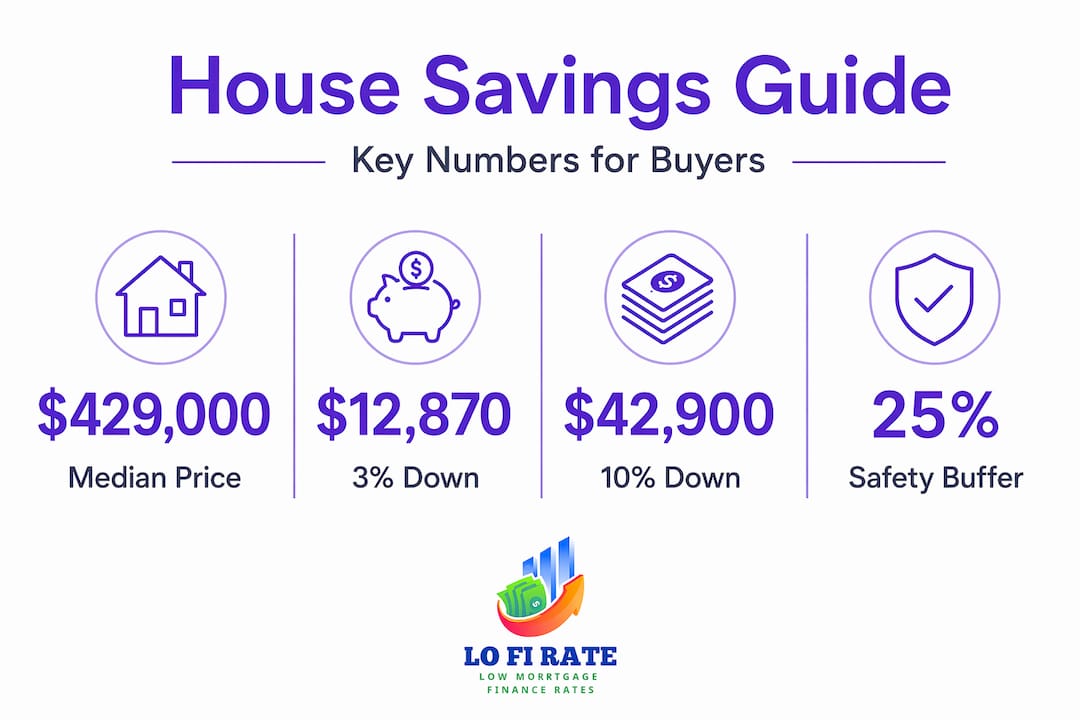

Most first-time buyers fixate on the down payment and forget everything else. That mistake creates a nasty surprise at the closing table. Before you save a single dollar, you need to know your real target.

The median US home price in 2026 sits at $429,000. A 3% down payment on that home is $12,870. A 10% down payment is $42,900. But the down payment is only the beginning. Closing costs run 3% to 5% of the purchase price, which translates to roughly $11,600 to $19,300 on that same $429,000 home. Most buyers who think they are ready get blindsided by this number.

Here is a simple framework for calculating your full savings target:

| Cost component | Estimated range (on $429K home) |

|---|---|

| Down payment (3%) | $12,870 |

| Down payment (10%) | $42,900 |

| Closing costs (3%–5%) | $11,600–$19,300 |

| Moving and initial repairs | $3,000–$8,000 |

| Emergency buffer (25% extra) | Varies by total |

Experts recommend padding your savings goal by 25% to cover moving costs, early repairs, furniture, and the unpredictable expenses that hit in the first six months of homeownership. If your raw target is $40,000, aim for $50,000. That cushion is not pessimism. It is the difference between a smooth transition and a financial crisis.

Pro Tip: Separate your house savings goal into three buckets from day one: down payment, closing costs, and buffer. Tracking them individually prevents you from feeling "close enough" when you have only saved for one.

Also plan for a 3 to 6 month emergency fund that lives completely apart from your home savings. Emptying your savings on purchase day and then facing a broken furnace a month later is one of the most common first-time buyer mistakes. You can read more about what goes into closing cost breakdowns to make sure your estimate is accurate before you lock in a savings target.

Setting up a savings plan that actually works

Once you know your target, turn it into a monthly number. This is where most people stall because the total feels enormous. The fix is simple math and the right infrastructure.

Start with your timeline. How long are you willing to save before you want to buy? Two years is aggressive. Four to five years is realistic for most markets. Take your total savings target and divide it by the number of months in your timeline.

Say your goal is $55,000 and you have three years (36 months). You need to save roughly $1,530 per month. If that number exceeds what your current budget allows, either extend your timeline or increase your income. There is no magic around it, but there are tools that make it far more consistent.

Where to keep your savings

Do not keep your house fund in your regular checking account. The money will quietly disappear into daily spending. Open a dedicated account and treat it as off-limits.

High-yield savings accounts currently earn around 4% annually, are FDIC-insured, and let you access the money within a few days when you need it. That combination of safety and liquidity makes them the right choice for any home purchase within one to three years. Here is how a few common vehicles compare:

- High-yield savings account (HYSA): Best for timelines under three years. Liquid, insured, earning 4%+. No risk.

- Certificates of deposit (CDs): Slightly higher rates for locking money away 6 to 24 months. Good if you will not need access mid-term.

- I-Bonds: Inflation-indexed, government-backed, and currently competitive. One-year lockup with a penalty for withdrawing within five years. Fits a three-plus year timeline.

- Brokerage or stock accounts: Too volatile for a near-term purchase. Avoid these for your down payment funds entirely.

Pro Tip: Name your high-yield savings account something specific, like "House Fund 2028." It sounds trivial, but research on savings behavior consistently shows that labeled accounts reduce the temptation to raid them.

The single most effective habit you can build is automating your transfers. Automated savings on payday consistently outperform manual saving because they remove the decision entirely. Set the transfer to hit the day your paycheck lands. You spend what is left. No willpower required.

Strategies to accelerate your savings

Getting to your target faster is not about cutting every pleasure from your life. That approach almost always fails within a few months. Sustainable saving focuses on reducing a few high-impact categories and finding ways to earn more, not suffering more.

Here is a ranked approach:

-

Target the big three expenses. Groceries, car insurance, and energy bills are the three spending categories where most households overspend relative to what they actually need. Grocery costs drop significantly with a weekly meal plan and a switch from branded to store-label staples. Car insurance rates are not fixed: shopping your policy annually often surfaces savings of $300 to $600 per year. Energy bills respond to simple changes like adjusting your thermostat schedule and switching to LED lighting throughout your home.

-

Audit subscriptions ruthlessly. Most people carry seven to ten recurring subscriptions and actively use three or four. Cancel anything you have not used in the past 30 days. Pause streaming services and rotate them quarterly rather than carrying all of them simultaneously.

-

Direct every windfall to the house fund. The average tax refund runs about $3,100. Two refunds could cover 12% to 25% of an FHA loan down payment. Treat refunds, bonuses, gifts, and any other irregular income as house money by default, not fun money.

-

Apply the 1% rule to every raise. When your income increases, increase your monthly savings contribution by at least 1% of your gross pay. If you earn $5,000 per month and get a raise, bump your savings by $50. You will never feel the loss, but over a few years, it compounds into a meaningful difference.

-

Add a side income stream and earmark it entirely. Freelancing, delivery work, tutoring, or selling unused items online can generate $300 to $800 per month. Routing all of that directly to your house fund without touching your main budget turns a three-year goal into a two-year one.

Pro Tip: Before cutting lifestyle spending, calculate what one year of your current Netflix subscription, gym membership, and daily coffee costs in total. When that number becomes concrete, the decision to pause or cut gets much easier.

First-time buyer programs that reduce your savings target

One of the least used levers available to first-time buyers is assistance programs. Many people assume they do not qualify or that the paperwork is too complicated. The reality is that these programs exist specifically for people in your position.

On the federal level, FHA loans allow a down payment as low as 3.5% with a credit score of 580 or higher. The typical first-time buyer now puts down about 9%, not 20%, and many use FHA financing to get there. VA loans and USDA loans offer zero-down options for eligible veterans and rural buyers respectively.

State and local governments offer additional help:

- Down payment assistance grants that do not need to be repaid

- Forgivable loans that disappear after you stay in the home for a set number of years

- Below-market mortgage rates reserved exclusively for first-time buyers

- Closing cost assistance that directly reduces your cash needed at settlement

The proposed Homeownership Savings Act would create a tax-advantaged account where first-time buyers can contribute $2,500 to $3,000 per year and deduct those contributions, up to a lifetime limit of $40,000. This legislation is still pending, but worth monitoring because it could significantly reduce the tax burden of your saving period.

To find programs in your state, start with your state housing finance agency's website. You can also explore an overview of first-time buyer programs to match yourself with programs designed for your specific situation. Do not skip this step. It could cut your savings target by tens of thousands of dollars.

Tracking progress and avoiding costly mistakes

Reaching your savings target is only part of the job. You also need to protect what you have built and prepare for the purchase process itself.

Review your house fund balance monthly, not just occasionally. Compare where you are against your monthly target. If you fall behind two months in a row, that is a signal to revisit your budget or timeline rather than hope things improve on their own. Small adjustments made early prevent large gaps later.

Watch for these common pitfalls:

- Dipping into the house fund for non-emergencies. Once you treat it as a backup account, the habit sticks and the balance stalls. Keep it at a separate bank if needed to add friction.

- Investing house savings in volatile assets. The stock market is not appropriate for money you plan to use within three years. A 20% market drop the year before you buy could delay your purchase by 12 to 18 months.

- Ignoring your credit score. Your credit score directly determines your mortgage rate. Every quarter, check your report for errors and work to keep your credit utilization below 30%. A 720 score versus a 640 score can cost you tens of thousands of dollars over the life of a loan.

- Skipping mortgage pre-approval. Get pre-approved before you start seriously shopping. Pre-approval clarifies your real budget, signals seriousness to sellers, and reveals any credit issues you need to fix before closing.

Pro Tip: Create a simple spreadsheet with three columns: your target balance for each month, your actual balance, and the gap. Seeing that gap shrink month by month is more motivating than any budgeting app feature.

For a deeper look at preparing financially for purchase, including how wholesale mortgage access can reduce your long-term costs, Lofirate has a practical guide worth reading before you start the offer process.

My honest take on saving for a home

I have watched a lot of people attempt the extreme-sacrifice approach to home saving. They cancel everything, eat rice and beans every night, and refuse any social spending for 18 months. Most of them burn out and abandon the goal entirely. A few succeed, but they resent the process.

What I have found actually works is a much quieter system. Automate the savings before you see the money, reduce two or three genuinely wasteful expenses, and then live your life reasonably. The home fund grows in the background while you stay sane in the foreground.

The biggest shift I have seen come from assistance programs. People who spend three minutes researching their state's down payment assistance options often discover they qualify for $10,000 to $20,000 in help they had no idea existed. That changes the math completely and often cuts years off the savings timeline.

My advice on the mortgage side is equally simple: do not accept the first rate you are offered. Retail lenders have a pricing spread built in that benefits them, not you. Wholesale broker access, through a platform like Lofirate, lets you see what the market actually offers without the markup. The difference on a $400,000 loan over 30 years can be significant.

The goal is not to punish yourself into homeownership. It is to build a system that delivers you there without burning you out along the way.

— LoFi

Your mortgage rate matters as much as your down payment

You can do everything right with your savings strategy and still overpay by thousands if you accept the wrong mortgage rate. Lofirate connects first-time buyers with licensed wholesale mortgage brokers who shop multiple lenders on your behalf, so you are not locked into a single bank's retail pricing. Whether you are exploring loan options suited to your financial situation or looking for a second opinion before you sign, Lofirate makes that process simple and obligation-free. When your down payment is ready, make sure your rate is just as competitive. Visit Lofirate to get matched with a broker in your state and see what you actually qualify for.

FAQ

How much should I save for a house down payment?

The minimum down payment depends on your loan type: 3.5% for FHA loans, 3% for some conventional loans, and 0% for VA and USDA loans. Most first-time buyers put down around 9% of the purchase price.

What is the best savings account for a house down payment?

A high-yield savings account is the best option for most buyers, offering around 4% interest with full FDIC insurance and same-week liquidity when you need the funds at closing.

How long does it take to save for a house?

Saving timelines typically range from two to six years depending on your income, local home prices, and how much assistance you qualify for. Automating contributions and directing windfalls to your fund shortens the timeline meaningfully.

Are there programs that help first-time buyers with the down payment?

Yes. FHA loans, state housing grants, forgivable down payment assistance loans, and potentially the proposed Homeownership Savings Act all reduce what you need to save out of pocket. Research your state housing finance agency for local options.

Should I keep my down payment savings invested in stocks?

No. Avoid volatile investments for money you plan to use within three years. A market downturn right before your purchase could delay your timeline significantly. Use a high-yield savings account or short-term CDs instead.