TL;DR:

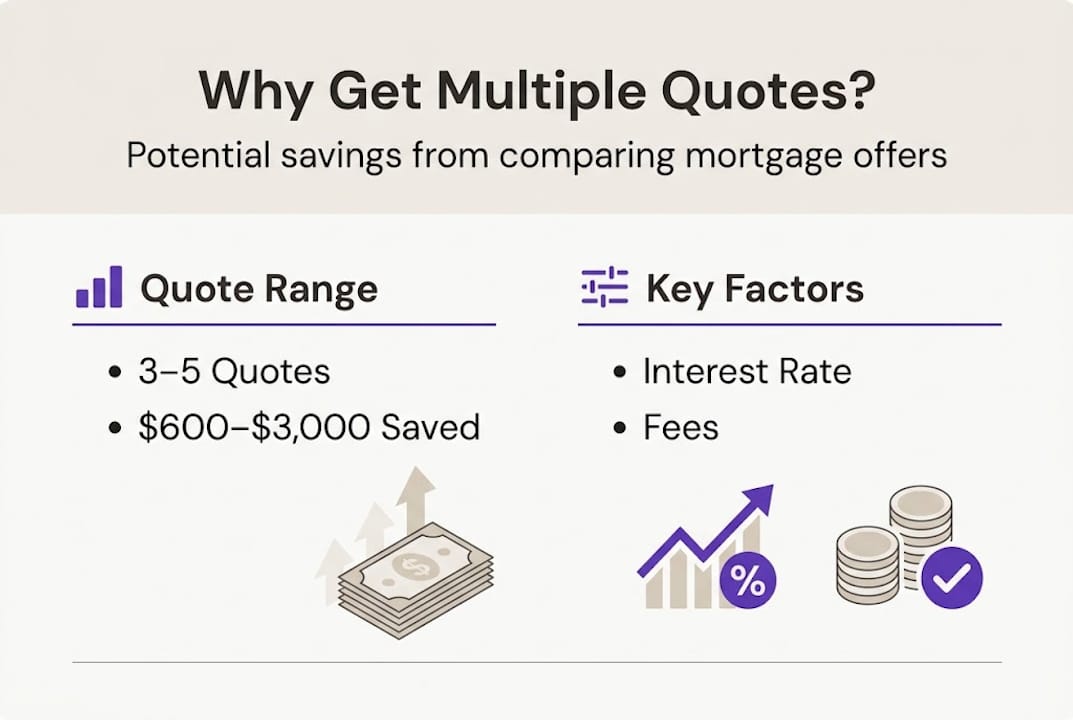

- Comparing multiple mortgage quotes can save homeowners between $600 and $3000 over the loan term.

- Being organized and obtaining official Loan Estimates enables effective comparison and negotiation.

- Borrowers hold leverage to negotiate better rates and fees by sharing competing offers with lenders.

Most homebuyers accept their first mortgage offer without question, and that single decision can quietly cost them thousands of dollars over the life of their loan. Comparing quotes isn't just a good idea, it's one of the most impactful financial moves you can make before signing anything. Multiple mortgage quotes can save you $600 to $3,000 or more, according to data from Freddie Mac and the CFPB. This guide walks you through why a second opinion matters, what you need to prepare, and how to compare offers without falling into the traps most buyers never see coming.

Table of Contents

- Why getting a second mortgage opinion matters

- What you need before seeking a second opinion

- Step-by-step: How to get and compare mortgage offers

- Verifying, negotiating, and choosing your best offer

- The overlooked power of borrower leverage

- Get matched with top mortgage offers

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Multiple quotes save money | Comparing at least three Loan Estimates can help you save thousands over your loan’s lifetime. |

| Preparation is key | Organize your financial documents before seeking second opinions to streamline the process. |

| Don’t accept first offers | Even small rate differences from a second opinion can create major savings on your mortgage. |

| Negotiation works | Bringing multiple offers gives you leverage to negotiate better mortgage terms. |

Why getting a second mortgage opinion matters

Your mortgage rate is not a fixed fact. It's a number that shifts depending on the lender, the day, and how well you've positioned yourself as a borrower. That's why accepting a single offer is a bit like buying the first car you test drive. You have no reference point, no leverage, and no way of knowing whether you're getting a fair deal.

The numbers make the case clearly. Comparing 3 to 5 lender quotes can save homeowners between $600 and $3,000 or more over the life of a loan. And that's a conservative estimate. On a $300,000 mortgage, a 0.25% rate reduction can add up to $10,000 or more in long-term savings. A quarter of a percent doesn't sound like much until you do the math.

Here's a quick snapshot of what rate differences look like in real numbers:

| Loan amount | Rate | Monthly payment | 30-year total paid |

|---|---|---|---|

| $300,000 | 7.00% | $1,996 | $718,560 |

| $300,000 | 6.75% | $1,946 | $700,560 |

| $300,000 | 6.50% | $1,896 | $682,560 |

That $500 per year difference between 6.50% and 7.00% adds up to $18,000 over three decades. It's not small change.

Understanding why comparing lenders matters goes beyond rates alone. Many buyers focus only on the interest rate and miss the APR, which is the Annual Percentage Rate. APR includes fees, points, and other costs rolled into a single number. Two lenders can advertise the same rate but have wildly different APRs, which means you'd be paying more with one than the other.

Key facts about mortgage shopping:

- Wholesale brokers often have access to rates not available at retail banks

- Your Loan Estimate (the official three-page document lenders must give you by law) is the only true apples-to-apples comparison tool

- Rate locks vary between lenders and can affect your final cost

- Lender fees like origination charges can range from zero to several thousand dollars

Knowing how to compare mortgage rates puts you in a fundamentally stronger position before you ever sit down to sign.

What you need before seeking a second opinion

Going to a lender without your documents ready is like going to a job interview without your resume. You might still get a conversation, but you won't get taken seriously. Before you approach multiple brokers or lenders, get organized.

Lenders will typically ask for the following:

- Two years of W-2s or tax returns (self-employed borrowers need full tax returns)

- Recent pay stubs covering at least the last 30 days

- Two to three months of bank statements from all accounts

- Photo ID and Social Security number for credit authorization

- Documentation of any debts, including student loans, car payments, and credit cards

- Property details, including the address and purchase price if you're buying

Having all of this ready before your first call speeds up the entire process and signals to lenders that you're a serious buyer. Speed matters because mortgage rates can shift daily.

Pro Tip: Scan and save all your documents in a single folder labeled with your name and the current month. When a lender requests something, you can respond within minutes instead of days. Faster responses can sometimes mean better rate-lock opportunities.

One of the most important decisions in this process is choosing between a mortgage broker and a direct lender. Here's how they compare:

| Feature | Wholesale broker | Direct lender (bank) |

|---|---|---|

| Access to multiple lenders | Yes, shops several | No, offers only own products |

| Rate pricing | Wholesale (often lower) | Retail pricing |

| Loan options | Broader variety | Limited to in-house products |

| Origination fees | Varies, often negotiable | Set by institution |

| Processing speed | Can vary | Often standardized |

You should also request official Loan Estimates from every source you consult. A Loan Estimate isn't just a quote, it's a legally standardized form that makes comparison straightforward and honest. Without it, you're comparing guesses.

Learning what goes into choosing the right lender before you start will save you from making decisions based on charm or convenience instead of actual numbers. And brushing up on mortgage rate basics helps you speak the language fluently when lenders start throwing terms at you.

Step-by-step: How to get and compare mortgage offers

Once your documents are organized, it's time to collect and examine multiple offers. The process is more straightforward than most buyers expect, as long as you follow it systematically.

- Identify 3 to 5 sources. Include at least one wholesale broker, one credit union, and one bank. This gives you range across different pricing models.

- Submit identical information to each. The same loan amount, property value, and down payment. Inconsistency makes comparisons meaningless.

- Request a Loan Estimate from each source. Lenders are legally required to provide one within three business days of receiving your application. Collecting 3 to 5 Loan Estimates is the only reliable way to make true comparisons.

- Compare APR, not just the rate. A lower rate with high fees can cost more than a slightly higher rate with minimal fees.

- Track everything in a spreadsheet. Include lender name, rate, APR, origination fee, closing costs, rate lock period, and monthly payment.

- Note any conditions. Some rates are only available if you set up auto-pay or maintain a certain account balance.

Pro Tip: Date-stamp every Loan Estimate when you receive it. Rates are time-sensitive, and comparing an estimate from Monday to one from Friday can introduce misleading differences if the market moved.

If a lender refuses to give you an official Loan Estimate and only offers a verbal quote or a vague summary sheet, walk away. That's a red flag. Every legitimate lender is required by federal law to provide this document.

Using a mortgage shopping checklist keeps the process from feeling overwhelming. And understanding the benefits of brokers can help you decide early on whether going through a wholesale channel makes sense for your situation.

Verifying, negotiating, and choosing your best offer

You've got the offers. Now the real work begins. Collecting Loan Estimates is only the start. Verifying, negotiating, and then choosing wisely is where most buyers leave money on the table.

Step 1: Verify what you're actually being promised. Check every line of the Loan Estimate. Confirm the rate lock period (30, 45, or 60 days), whether the rate is fixed or adjustable, and what closing costs are included. Ask each lender to clarify any fees that feel vague.

Step 2: Use offers as leverage. This is where most buyers hold back, and they shouldn't. Wholesale brokers often negotiate better rates and terms than direct banks because they have access to a wider pricing network. But even banks can move on fees and sometimes on rate when pushed.

Here's a simplified example of what negotiation can look like in practice:

| Item | Original offer | After negotiation |

|---|---|---|

| Interest rate | 7.00% | 6.875% |

| Origination fee | $2,500 | $1,500 |

| Lender credits | $0 | $750 |

| Monthly payment | $1,996 | $1,970 |

That negotiation took one phone call and saved this borrower over $9,000 across the loan term.

Final checklist before you decide:

- Does the rate lock cover your expected closing date with a buffer?

- Are closing costs clearly itemized and reasonable?

- Is the APR the lowest among comparable offers?

- Have you asked whether the lender will match or beat a competing quote?

- Do you understand if the rate is fixed or could change?

Understanding how brokers access better rates gives you insight into why wholesale pricing often beats retail. And knowing the right questions for brokers means you walk into every conversation with confidence instead of confusion.

The overlooked power of borrower leverage

Here's something the mortgage industry rarely advertises: lenders and brokers fully expect you to negotiate. The first offer is not a final offer. It never is. But most buyers treat it like a take-it-or-leave-it situation because they don't realize they have any power.

The moment you hold two competing Loan Estimates in your hands, you have leverage. Real, measurable, financial leverage. You're no longer a buyer hoping to get approved. You're a client that multiple lenders want to win. That shift in dynamic changes everything about how the conversation goes.

One buyer we know of shared a competitor's Loan Estimate with their broker during a refinance. The broker came back with a rate that was 0.375% lower, saving roughly $14,000 over the life of the loan. No special credit score. No larger down payment. Just the act of mortgage rate transparency and a willingness to share information.

Most people never do this because no one tells them they can. Now you know.

Get matched with top mortgage offers

You've done the research. You understand what a Loan Estimate is, why APR matters more than the headline rate, and how a single conversation with a competing lender can change your entire mortgage picture. The logical next step is putting that knowledge into action with real wholesale broker access.

LoFiRate connects you with licensed wholesale mortgage brokers in your state who shop multiple lenders on your behalf. There's no obligation and no pressure, just a transparent consultation that could reveal real savings on your purchase or refinance. Explore your loan options or get started with mortgage broker matching today and see what a second opinion can actually do for your bottom line.

Frequently asked questions

How many mortgage offers should I get for a second opinion?

Aim for at least three, and ideally five Loan Estimates. Shopping 3 to 5 lenders maximizes your savings potential and gives you real negotiating power.

Does getting multiple mortgage quotes hurt my credit score?

No, not if you gather them within a focused window. Multiple inquiries within 14 to 45 days are treated as a single event by credit scoring models, so your score stays protected.

Are brokers always cheaper than banks for refinancing?

Not always, but brokers frequently outcompete banks by accessing wholesale pricing that retail institutions simply don't offer to the public.

Can I negotiate mortgage fees and rates if I have multiple offers?

Absolutely. Lenders often match or beat competitors when you present a valid competing offer. Negotiating with Loan Estimates in hand is one of the smartest moves a borrower can make.