TL;DR:

- A mortgage modification alters loan terms to make monthly payments more affordable by extending the repayment period, reducing interest rates, or deferring part of the principal. It works within your current loan and differs from refinancing or forbearance, often requiring detailed documentation and trial periods before becoming permanent. While many modifications defer debt through principal forbearance, understanding the full structure helps homeowners avoid pitfalls and ensure sustainable financial relief.

If your monthly mortgage payment feels like it's slowly draining your finances, you're not alone. Millions of American homeowners have faced the same pressure, and a mortgage modification program may be one of the most effective tools available to bring that payment down to something manageable. According to the Consumer Financial Protection Bureau, a mortgage modification is a change in one or more loan terms designed to make monthly payments more affordable, typically by extending the repayment period, reducing the interest rate, or deferring part of the principal balance. This guide walks you through every stage of the process so you can act with confidence.

Table of Contents

- Understanding mortgage modification: What it is and who qualifies

- Preparing for a mortgage modification: What you need before applying

- Step-by-step: Applying for a mortgage modification

- Comparing modification options: Impact on payments, principal, and long-term cost

- What to watch out for: Common pitfalls and expert strategies

- Expert perspective: Why not all mortgage modifications deliver true relief

- Next steps: Get personalized mortgage help

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Modification basics | Mortgage modification changes loan terms to make payments more affordable and may include extending the term or reducing the interest rate. |

| Preparation is vital | Gather all financial documents and a clear hardship statement to strengthen your application. |

| Most common method | The majority of U.S. mortgage modifications involve principal forbearance rather than outright debt reduction. |

| Long-term costs | Lower monthly payments may come with higher overall costs or deferred debt, so review the terms carefully. |

| Expert guidance matters | Getting professional advice increases your chance of success and helps you avoid costly mistakes. |

Understanding mortgage modification: What it is and who qualifies

With the challenge defined, the first step is to understand what mortgage modification actually involves and whether it's the right option for your situation.

A mortgage modification is not the same as refinancing. Refinancing replaces your existing loan with a brand new one, usually requiring a credit check, closing costs, and a formal application process through a new lender. Modification, by contrast, works within your current loan. Your servicer agrees to change one or more terms to reduce your monthly obligation. According to the CFPB, a mortgage loan modification can lower payments through three primary mechanisms: extending the loan term (say, from 20 remaining years to 30 years), reducing the interest rate permanently or temporarily, or deferring a portion of the principal balance to the end of the loan.

Modification also differs from forbearance. Forbearance is a temporary pause or reduction in payments. It does not change your loan permanently. Think of forbearance as hitting pause, while modification is actually rewriting part of the song.

Common eligibility factors for mortgage modification include:

- Documented financial hardship (job loss, medical emergency, divorce, income reduction)

- The home is your primary residence in most programs

- You are behind on payments or at imminent risk of default

- Your loan is owned or guaranteed by Fannie Mae, Freddie Mac, FHA, VA, or USDA (or held privately)

- You have enough income to sustain the modified payment

| Option | Changes loan? | Permanent? | Affects credit? |

|---|---|---|---|

| Modification | Yes, alters terms | Usually yes | Possible impact |

| Refinance | Yes, new loan | Yes | Soft/hard inquiry |

| Forbearance | No, pauses payments | No | Possible impact |

| Repayment plan | No, adds to payments | No | Minimal |

For a deeper look at navigating loan modification and how it fits your unique situation, understanding the program types available is critical. You can also explore permanent mortgage modification options for government-backed loans on our site.

Pro Tip: Forbearance can feel like relief in the moment, but missed payments don't disappear. They get added to what you owe. If you're struggling long term, push for modification instead of repeatedly extending forbearance.

Preparing for a mortgage modification: What you need before applying

Now that you know how modifications work, it's time to prepare the documents and proof you'll need to give your application the best shot.

Lenders and servicers evaluate your modification request based on your ability to sustain the modified payment. They want to see that you have enough income to support a lower payment, but not so much income that you don't actually need the help. This balancing act is why documentation is so critical.

Here's a step-by-step prep checklist to organize your materials:

- Collect proof of income. This includes recent pay stubs (last two months), tax returns (last two years), and bank statements (last two to three months). If you're self-employed or have irregular income, include profit and loss statements.

- Draft a hardship letter. This is a written explanation of what caused your financial difficulty and why it affected your ability to make mortgage payments. Be specific, honest, and brief. One to two pages is typically enough.

- List all monthly expenses. Servicers may require a full budget breakdown, including utilities, insurance, car payments, and minimum debt payments.

- Gather your mortgage statement. Have your most recent statement and loan number ready.

- Check for government program eligibility. FHA, VA, USDA, Fannie Mae, and Freddie Mac each have their own modification guidelines. Knowing which one backs your loan helps you target the right program.

- Compile any correspondence from your servicer. If you've received any notices, save them all. They can contain important deadlines.

The CFPB notes that modifications are evaluated for affordability and may include trial terms before becoming permanent. Borrowers should understand both short-term and long-term consequences of modified terms, including how deferred amounts or longer loan periods affect total cost over the life of the loan.

| Government loans | Private/conventional loans |

|---|---|

| Specific program rules (FHA-HAMP, VA LOOP, etc.) | Servicer has more discretion |

| Standardized documentation | May require more negotiation |

| Term extension often capped | More flexible structures possible |

| Streamlined for qualifying borrowers | Approval varies widely by servicer |

Taking time to learn smart mortgage saving strategies while you prepare can also help you spot other cost-cutting opportunities in your overall mortgage picture.

Pro Tip: Your hardship letter is not the place to be vague. Servicers read hundreds of these. A specific, timeline-driven explanation ("I was laid off in March 2025 and found part-time work in July") is far more persuasive than a general statement about financial difficulty.

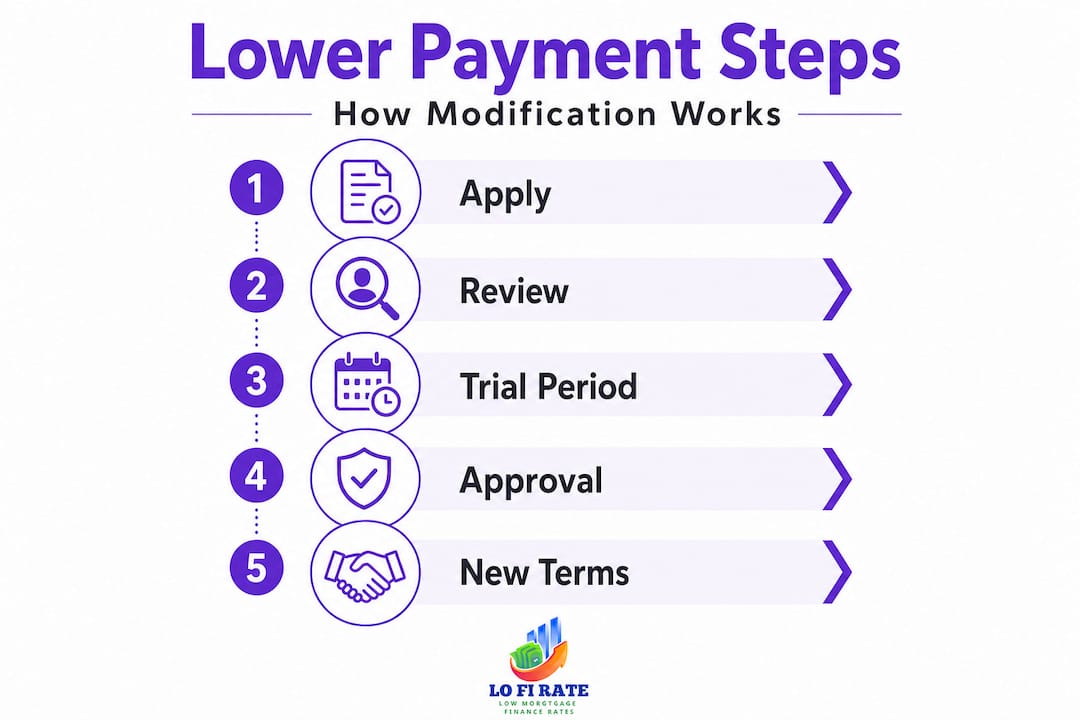

Step-by-step: Applying for a mortgage modification

With documents ready, here's exactly what to expect from your first call to the servicer through final approval.

The application process can feel bureaucratic and slow. But knowing what's coming at each stage reduces the frustration significantly.

Here's the full process from start to finish:

- Call your servicer's loss mitigation department. Don't call general customer service. Ask specifically for loss mitigation. Explain that you want to apply for a mortgage modification and request their complete application package.

- Submit your complete application. Send everything in one organized package. Missing documents are the number one reason applications stall. Use certified mail or the servicer's online portal so you have a record.

- Follow up within five to seven business days. Confirm receipt. Ask for a dedicated point of contact or case number.

- Respond to all information requests immediately. Servicers often send requests for additional documentation. A slow response can reset your timeline or result in a denial.

- Enter the trial modification period. If approved for trial, you'll be given a lower trial payment for three months (typically). Make every payment on time and in full.

- Receive and review your permanent modification offer. After the trial period, the servicer issues a permanent modification agreement. Read every line before signing. Confirm the rate, term, and any deferred balance.

- Sign and return the agreement promptly. Delays in returning the signed agreement can create complications.

According to FHFA foreclosure prevention data, Fannie Mae and Freddie Mac have completed tens of thousands of permanent loan modifications since the 2008 conservatorship began, demonstrating that this is a well-established and accessible process for qualifying borrowers.

Warning: Missing even one payment during your trial modification period can disqualify you from receiving a permanent modification. Treat those trial payments like the most important bills you have. Set up autopay if you can and never assume a grace period applies.

Staying informed about compliance during mortgage modification is also smart. Understanding your rights protects you from errors that could delay or derail your approval.

Comparing modification options: Impact on payments, principal, and long-term cost

Once your application is moving, you'll likely face different program options. Understanding their true impacts will help you make smarter choices.

Three modification approaches dominate the landscape. Each one produces a lower monthly payment through a different mechanism, and each carries a different long-term price tag.

According to the FHFA's January 2026 report, 20,330 foreclosure prevention actions were completed that month alone. Of those, approximately 38.7% were permanent loan modifications, totaling 6,670 permanent modifications. Strikingly, about 62.4% of those modifications involved principal forbearance, while only 36.9% were extend-term-only modifications.

That statistic matters. It tells you that the majority of modifications don't actually reduce your debt. They defer it.

| Modification type | How it lowers payment | Effect on total loan cost | Debt eliminated? |

|---|---|---|---|

| Term extension | Spreads payments over more years | Higher total interest paid | No |

| Interest rate reduction | Lowers rate on existing balance | Lower total interest paid | No |

| Principal forbearance | Defers part of balance | Deferred balance due at payoff | No |

| Principal reduction | Actually reduces balance | Lowest total cost | Yes (rare) |

Pros and cons of each approach:

- Term extension: Simple to understand, easy to implement, but you'll pay significantly more interest over a longer loan life.

- Interest rate reduction: Most impactful for long-term savings, but servicers may only offer this temporarily.

- Principal forbearance: Immediately drops your payment but leaves a deferred balance (often called a "balloon") due when you sell, refinance, or pay off the loan.

- Principal reduction: Rare, but the most genuinely helpful. This actually erases debt rather than delaying it.

FHFA data from Q4 2025 confirms that principal forbearance represents a large share of enterprise loan modifications, meaning that much of the "relief" many borrowers receive is deferred, not eliminated.

If you're weighing whether modification even makes sense versus starting fresh, comparing refinancing vs. modification side by side is worth doing before you commit.

What to watch out for: Common pitfalls and expert strategies

Before finalizing your choice, don't overlook common mistakes that can undermine your efforts and cost you more later on.

The modification process has several traps that catch homeowners off guard. Knowing them in advance puts you in a much stronger position.

Common pitfalls to avoid:

- Submitting an incomplete application. Servicers are not required to chase you for missing documents. An incomplete file is often just closed.

- Missing deadlines. Modification programs have windows. Missing a response deadline can result in automatic denial.

- Misreading the new terms. A lower payment sounds great until you realize it comes with a deferred balance that's due as a lump sum when you sell your home.

- Assuming approval equals done. Verbal approvals mean nothing. Always wait for written confirmation.

- Stopping communication. If your servicer goes quiet, don't assume everything is fine. Call and get a status update.

As the FHFA data for January 2026 illustrates, the majority of modifications involve principal forbearance rather than outright reduction. A lower monthly payment can be misleading if deferred debt is quietly stacking up in the background. Always compare not just the new payment amount but the full structure of the relief being offered.

Understanding how to evaluate servicers is similar to choosing the right mortgage lender in the first place. The same principles of clarity, transparency, and comparison apply.

Pro Tip: Before signing your permanent modification agreement, ask your servicer two specific questions: "What is the deferred principal amount, if any?" and "When and how is the deferred balance due?" Get both answers in writing. If a servicer won't confirm terms in writing, that's a red flag.

Expert perspective: Why not all mortgage modifications deliver true relief

Most homeowners enter the modification process hoping for genuine debt relief. What they often get is something more complicated. And understanding that difference can mean saving tens of thousands of dollars over time.

Here's the uncomfortable reality: the structure of most modification programs today prioritizes payment reduction over debt elimination. Based on FHFA's reporting, principal forbearance accounts for a majority of permanent enterprise loan modifications. That means most borrowers who get "relief" are actually just pushing a portion of their debt further down the road.

This isn't inherently bad. If the alternative is foreclosure, a deferred balance you pay off years from now is far better than losing your home. But it becomes a problem when homeowners don't fully understand what they've agreed to.

Our candid view: modification makes the most sense when you have a temporary hardship and expect your financial situation to improve. If the hardship is permanent (a disability, a permanently reduced income), modification buys time but may not be sustainable long term. In those cases, a genuine financial counseling session to evaluate selling, downsizing, or other alternatives is often the more honest conversation to have.

For borrowers who have stabilized their finances, refinancing at a lower rate through a wholesale broker can sometimes produce better long-term savings than a modification. Explore the full process for lowering your mortgage to see which path fits your financial picture.

The best outcome isn't just a lower payment today. It's a sustainable mortgage that you can carry comfortably for years without deferred debt turning into a crisis later.

Next steps: Get personalized mortgage help

You now have a solid understanding of how mortgage modification works, what to prepare, and what to watch out for. But every homeowner's situation is different, and the stakes are too high to navigate this alone.

At LoFiRate.com, we connect homeowners with licensed wholesale mortgage brokers who can evaluate your specific loan situation and help you understand whether modification, refinancing, or another strategy makes the most sense for you. Unlike retail lenders, wholesale brokers shop multiple lenders to find the most competitive terms available. There's no obligation and no cost to get a second opinion. Visit our mortgage modification guidance page to see how we can help, explore mortgage loan options tailored to your situation, or go directly to LoFiRate.com to connect with a licensed broker in your state today.

Frequently asked questions

How long does the mortgage modification process take?

The timeline varies but typically ranges from several weeks to a few months, depending on your servicer's workload, the completeness of your application, and whether a trial period is required before permanent approval.

Will a mortgage modification hurt my credit?

A modification may show up on your credit report and cause a temporary dip, but it is generally far less damaging than foreclosure or a series of missed payments. According to the CFPB, modification is a structured loss-mitigation option designed to help borrowers stay in their homes.

What are the most common types of mortgage modifications?

The three most common types are principal forbearance, term extension, and interest rate reduction. According to FHFA's January 2026 data, principal forbearance made up approximately 62.4% of permanent modifications completed that month.

How does a mortgage modification compare to refinancing?

Refinancing replaces your existing loan with an entirely new one, while a modification adjusts the terms of your current loan without creating a new loan. According to the CFPB, modification is specifically designed to create affordability within the existing loan structure, making it accessible even when credit conditions prevent a traditional refinance.