Refinancing your mortgage can feel overwhelming, especially when you're juggling high monthly payments and trying to figure out if lower rates are truly within reach. Many homeowners wonder whether refinancing is the right move or just another financial hurdle. The good news is that with the right preparation and guidance, particularly from wholesale mortgage brokers, you can unlock significant savings and reduce your monthly burden. This guide walks you through the entire refinancing process, from understanding your options to verifying your new loan terms, so you can make informed decisions that protect your financial future.

Table of Contents

- Key takeaways

- Understanding the refinancing problem and how it affects you

- Preparing to refinance: what you need and key eligibility criteria

- Executing the refinancing process with wholesale mortgage brokers

- Verifying outcomes and managing your refinanced mortgage

- Explore low mortgage rates and loan options at LO FI RATE

- How to refinance mortgage frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Lower rates save money | Refinancing can lower your interest rate and monthly payments, producing meaningful savings over the life of the loan. |

| Prepare and gather documents | Organize income, assets, and debt information early to smooth the application process. |

| Work with wholesale brokers | Wholesale brokers can help you access better rates and terms. |

| Assess timing before refinancing | Consider how soon you plan to move and whether the monthly savings will cover closing costs. |

| Know common obstacles | Be aware of credit, appraisal, and income documentation hurdles that can delay or derail approval. |

Understanding the refinancing problem and how it affects you

Homeowners refinance for various reasons, but the most common motivation is securing a lower interest rate. When market rates drop or your credit improves, refinancing can translate into substantial monthly savings and thousands of dollars saved over the life of your loan. Lower mortgage rates can save thousands over loan lifetime, making refinancing an attractive option for many.

Beyond rate reduction, refinancing allows you to tap into home equity for renovations, debt consolidation, or other major expenses. Some homeowners refinance to switch from an adjustable rate mortgage to a fixed rate for payment stability. Others want to shorten their loan term, building equity faster and paying less interest overall.

However, refinancing isn't without challenges. Qualifying can be difficult if your credit score has dropped or your home value has declined. Closing costs typically range from 2% to 5% of the loan amount, which means you need to calculate whether the savings justify the upfront expense. The paperwork process can feel tedious, requiring extensive documentation of income, assets, and debts.

Timing matters significantly in refinancing decisions. If you plan to move within a few years, you might not recoup closing costs through monthly savings.

Common obstacles include:

- Insufficient credit score for the best rates

- Home appraisal coming in lower than expected

- Debt to income ratio exceeding lender limits

- Employment gaps or income documentation issues

- Existing mortgage penalties for early payoff

Understanding these challenges upfront helps you prepare effectively and avoid surprises during the application process. Not every situation benefits from refinancing, so you need to evaluate your specific circumstances carefully before moving forward.

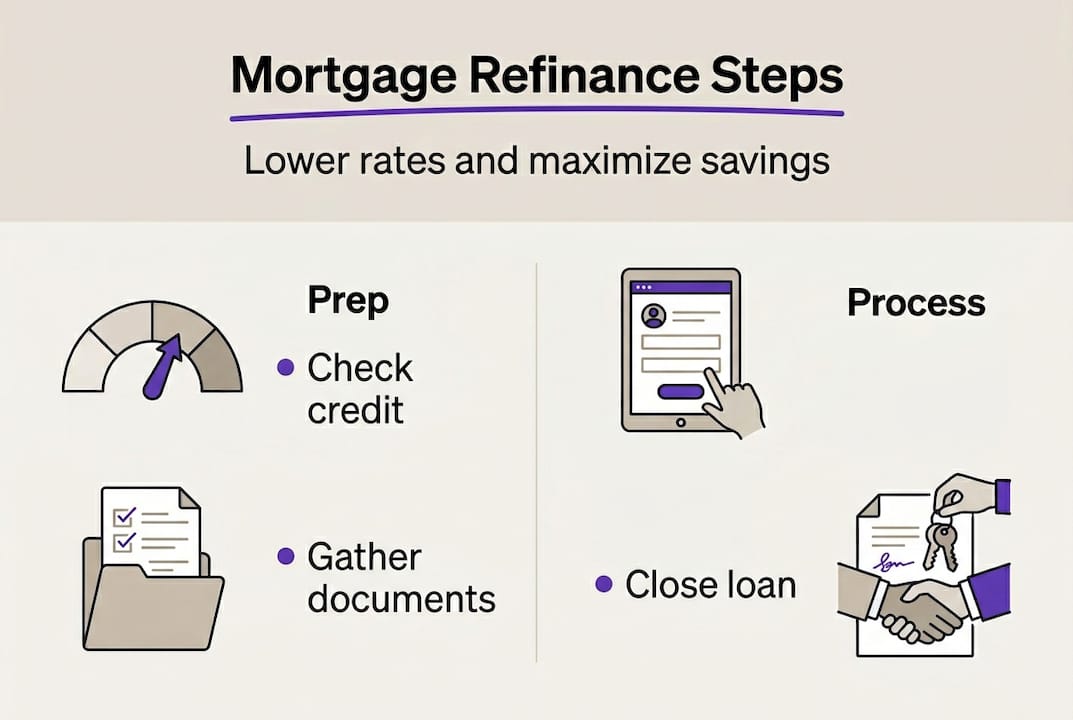

Preparing to refinance: what you need and key eligibility criteria

Successful refinancing starts with thorough preparation. Lenders evaluate several key factors when reviewing your application, and understanding these criteria helps you position yourself for approval with favorable terms.

Credit score requirements vary by loan type, but conventional refinancing typically requires a minimum score of 620. For the best rates, aim for 740 or higher. Your credit score directly impacts the interest rate you'll receive, with each tier representing potential savings or costs over the loan term. Clear steps help ensure mortgage refinancing approval when you understand what lenders are looking for.

Income verification is critical. Lenders want to see stable employment history and sufficient income to cover your new mortgage payment along with other debts. Self employed borrowers face additional scrutiny and may need two years of tax returns plus profit and loss statements.

Home equity plays a major role in approval. Most lenders require at least 20% equity for conventional refinancing, though some programs accept lower amounts with mortgage insurance. An appraisal determines your home's current value, which can be a sticking point if property values have declined in your area.

Here's what you'll need to gather:

- Last two years of federal tax returns

- Recent pay stubs covering 30 days

- Two months of bank statements for all accounts

- Current mortgage statement showing balance and payment history

- Homeowners insurance policy information

- Government issued photo identification

Calculating your break even point is essential before committing to refinancing. Divide your total closing costs by your monthly savings to determine how many months it takes to recoup the expense. If you plan to stay in your home longer than the break even period, refinancing likely makes financial sense.

| Documentation stage | What's required | Timeline |

|---|---|---|

| Initial application | Basic financial snapshot | 1-2 days |

| Document submission | Complete financial records | 3-5 days |

| Appraisal scheduling | Home inspection coordination | 1-2 weeks |

| Underwriting review | Detailed verification process | 2-3 weeks |

| Final approval | Conditional clearances met | 3-5 days |

Pro Tip: Request your credit reports from all three bureaus several months before applying. Dispute any errors and pay down high balance credit cards to improve your score. Even a 20 point increase can qualify you for a better rate tier, potentially saving thousands over the loan term.

Executing the refinancing process with wholesale mortgage brokers

Working with wholesale mortgage brokers offers distinct advantages over going directly to retail lenders. Wholesale brokers often provide better mortgage rates and lower fees because they access multiple lenders' wholesale pricing rather than being limited to a single institution's retail rates.

Here's how to navigate the refinancing process with a wholesale broker:

- Research and contact licensed wholesale brokers in your state. Verify their credentials and read reviews from previous clients.

- Schedule consultations with at least three brokers to compare their approach, lender networks, and fee structures.

- Provide your financial documentation and discuss your refinancing goals, including desired loan terms and monthly payment targets.

- Review the loan estimates each broker provides, paying close attention to interest rates, closing costs, and any lender credits.

- Ask detailed questions about each offer, including potential rate locks, processing timelines, and any conditions that could affect final terms.

- Select the best offer and begin the formal application process with your chosen broker.

- Stay responsive throughout underwriting, promptly providing any additional documentation requested.

- Review your closing disclosure carefully at least three days before closing, verifying all numbers match your expectations.

| Factor | Wholesale broker | Retail lender |

|---|---|---|

| Rate access | Multiple lenders' wholesale pricing | Single institution's retail rates |

| Closing costs | Often lower due to competition | Typically higher with fewer negotiations |

| Processing speed | 30-45 days average | 45-60 days average |

| Personal service | Dedicated broker guidance | May work with multiple loan officers |

| Lender options | 10-50+ lenders available | One lender only |

When evaluating broker offers, don't focus solely on interest rate. Compare annual percentage rates, which include fees and give a more complete picture of loan costs. Watch for junk fees that add unnecessary expenses without providing value.

Pro Tip: Ask brokers these critical questions: How many lenders do you work with? What's your average closing timeline? Can you provide references from recent refinancing clients? Do you charge broker fees, and are they negotiable? What happens if my appraisal comes in low? Getting clear answers helps you identify brokers who prioritize your interests.

Common mistakes include accepting the first offer without shopping mortgage lenders wholesale brokers, failing to lock your rate when favorable, or not reading the fine print on adjustable rate features. Taking time to understand each offer prevents buyer's remorse and ensures you secure the best possible terms.

Verifying outcomes and managing your refinanced mortgage

Closing on your refinanced mortgage isn't the finish line. Careful verification of your new loan terms and proactive management ensure you realize the full benefits of refinancing.

Start by thoroughly reviewing your closing disclosure, which you'll receive at least three business days before closing. Compare every line item to your initial loan estimate. Interest rate, loan amount, closing costs, and monthly payment should all match your expectations. If you spot discrepancies, address them immediately with your broker or lender.

At closing, you'll sign numerous documents. Don't rush through this process. Read each form carefully, asking questions about anything unclear. Key documents include the promissory note, deed of trust or mortgage, and closing disclosure. Keep copies of everything in a secure location for future reference.

After closing, monitor your first few mortgage statements closely. Verify that your payment amount matches the closing disclosure and that your lender is correctly applying payments to principal and interest. Proper management after refinancing maximizes long-term savings through strategic payment approaches.

Strategies to accelerate equity building:

- Make biweekly payments instead of monthly, resulting in one extra payment per year

- Round up your monthly payment to the nearest hundred dollars, applying extra to principal

- Use windfalls like tax refunds or bonuses for additional principal payments

- Set up automatic extra payments to maintain consistency without ongoing decisions

- Refinance again if rates drop significantly, but calculate new break even points first

Watch for these warning signs that might indicate issues with your refinanced mortgage:

- Payment amounts that fluctuate unexpectedly

- Escrow shortages requiring sudden large payments

- Property tax or insurance increases not reflected in escrow adjustments

- Confusion about where to send payments if servicing transfers

- Difficulty accessing online account information or customer service

Consider refinancing again if market rates drop at least 0.75% to 1% below your current rate and you plan to stay in your home long enough to recoup new closing costs. Your improved payment history and potentially higher credit score might qualify you for even better terms.

Common post refinancing pitfalls include forgetting to cancel old automatic payments, missing the first payment due date because of confusion about timing, or failing to update homeowners insurance with your new lender information. Create a checklist to ensure you handle all administrative tasks promptly.

Explore low mortgage rates and loan options at LO FI RATE

Now that you understand the refinancing process and how wholesale brokers can help you secure better rates, it's time to explore your options. LO FI RATE connects homeowners with licensed wholesale mortgage brokers who shop multiple lenders to find competitive pricing you won't get from retail banks.

Whether you're looking to lower your monthly payment, tap into home equity, or switch loan types, LO FI RATE provides access to low mortgage finance rates through a transparent, no obligation consultation process. You'll work with experienced professionals who understand the wholesale market and can guide you toward loan options that match your financial goals. Getting a second opinion on your refinancing options takes minutes and could save you thousands over your loan term.

How to refinance mortgage frequently asked questions

What credit score do I need to refinance my mortgage?

Most conventional refinancing programs require a minimum credit score of 620, though government backed loans like FHA may accept scores as low as 580. For the best interest rates and terms, aim for a score of 740 or higher. If your score falls below these thresholds, focus on paying down debts and disputing credit report errors before applying.

How long does the refinancing process typically take?

The average refinancing timeline ranges from 30 to 45 days from application to closing, though it can extend to 60 days depending on your lender's workload and any complications with documentation or appraisal. Working with wholesale brokers often speeds up the process because they have established relationships with multiple lenders. You can help by submitting complete documentation promptly and responding quickly to any underwriter requests.

Are there fees I should expect when refinancing?

Yes, refinancing typically costs 2% to 5% of your loan amount in closing costs. Common fees include appraisal charges, title search and insurance, origination or broker fees, credit report costs, and recording fees. Some lenders offer no closing cost refinancing, but they build the expenses into a higher interest rate. Always compare the total cost of each option over your expected time in the home.

Can I refinance if my home value has decreased?

Refinancing with decreased home value is challenging but not impossible. If you owe more than your home is worth, you might qualify for specific programs like the FHA Streamline Refinance or VA Interest Rate Reduction Refinance Loan, which have more flexible equity requirements. Conventional refinancing typically requires at least 20% equity, so a low appraisal can derail your application unless you can bring cash to closing.

How do wholesale mortgage brokers save me money?

Wholesale brokers access pricing that retail banks reserve for industry professionals rather than direct consumers. They shop your application to multiple lenders simultaneously, creating competition that drives down rates and fees. Because brokers work on commission from lenders rather than charging you directly, their services often cost less than going through a retail bank while delivering better loan terms. This wholesale access can save you thousands in interest over your loan term.