Securing a mortgage rate can feel like navigating a maze, especially when retail lenders offer limited options at inflated prices. Wholesale mortgage brokers provide access to multiple lenders, creating competition that drives rates down and saves you thousands over your loan's life. This guide walks you through preparing your finances, engaging brokers effectively, and verifying you've locked in the best possible rate. Whether you're buying your first home or refinancing, understanding how to leverage wholesale broker networks puts you in control of your mortgage costs.

Table of Contents

- Key takeaways

- Preparing to secure lower mortgage rates

- Step-by-step process to get lower mortgage rates with wholesale brokers

- Common pitfalls and how to verify you've secured the best mortgage rate

- Get started with LO FI RATE for low mortgage financing

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Shop around via brokers | Shopping through wholesale broker networks creates lender competition that can lower rates and reduce overall costs. |

| Wholesale brokers lower rates | Wholesale brokers access multiple lenders, driving competitive offers especially for refinancers and borrowers with non standard financial profiles. |

| Understand loan options and process | Knowing loan types, rate structures, and the application workflow helps you negotiate better terms. |

| Prepare required documents early | Gather identification, recent pay stubs, tax returns, bank statements, and other income records before applying. |

| Compare offers to save money | Evaluating multiple lender quotes through broker networks can save thousands over a 30 year mortgage. |

Preparing to secure lower mortgage rates

Before contacting brokers, you need foundational knowledge about how mortgage rates work and what lenders evaluate. Your mortgage rate represents the annual cost of borrowing, expressed as a percentage of your loan amount. This rate combines the base interest charge plus additional costs like origination points, which are upfront fees paid to reduce your ongoing rate. Understanding these components helps you evaluate whether a lower advertised rate actually saves money once you account for fees.

Different loan types carry distinct rate structures and qualification requirements. Fixed-rate mortgages lock your rate for the entire loan term, providing payment stability but typically starting higher than adjustable options. Adjustable-rate mortgages (ARMs) offer lower initial rates that reset periodically based on market indexes, creating payment uncertainty but potential savings in the early years. Government-backed loans like FHA and VA often feature competitive rates for qualified borrowers, while jumbo loans for high-value properties usually carry premium pricing due to increased lender risk.

Common loan types and typical rate ranges

| Loan Type | Typical Rate Range | Best For |

|---|---|---|

| 30-Year Fixed | 6.25% to 7.50% | Long-term stability, predictable budgets |

| 15-Year Fixed | 5.50% to 6.75% | Faster equity building, lower total interest |

| 5/1 ARM | 5.75% to 7.00% | Short-term ownership, rate risk tolerance |

| FHA | 6.00% to 7.25% | Lower credit scores, smaller down payments |

| VA | 5.75% to 7.00% | Military service members, zero down payment |

| Jumbo | 6.50% to 8.00% | High-value properties exceeding conforming limits |

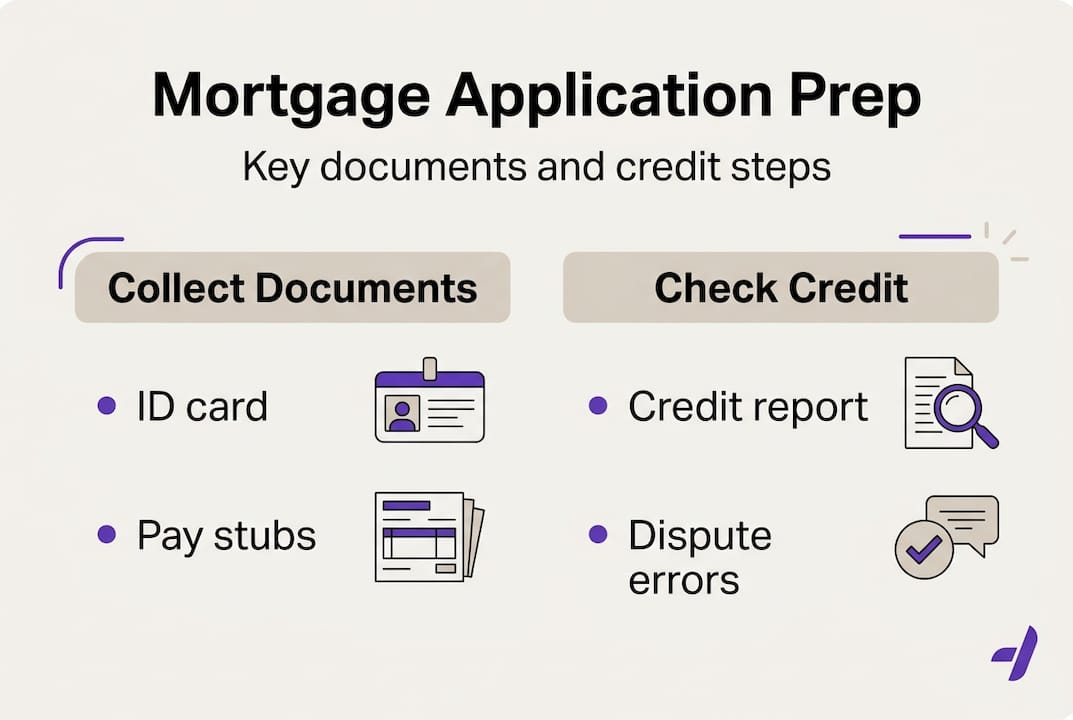

Lenders evaluate your creditworthiness through several key documents. You'll need government-issued identification, recent pay stubs covering at least 30 days, two years of tax returns with all schedules, bank statements showing reserves, and documentation of any additional income sources. Property details including the address, purchase price, and estimated value help brokers match you with appropriate loan programs. Your credit score plays a crucial role, with scores above 740 typically qualifying for the best rates while scores below 620 face significant rate premiums or limited options.

Pro Tip: Pull your credit report from all three bureaus at least 60 days before applying. This gives you time to dispute errors, pay down balances, and avoid new credit inquiries that temporarily lower your score.

Financial preparation extends beyond documents. Calculate your debt-to-income ratio by dividing monthly debt payments by gross monthly income. Most lenders prefer ratios below 43%, though some programs allow higher percentages with compensating factors like substantial cash reserves. Save for closing costs ranging from 2% to 5% of the purchase price, covering appraisals, title insurance, and lender fees. Understanding mortgage rates and their calculation methods helps you recognize competitive offers when brokers present options.

Research loan options that match your financial situation and homeownership goals. First-time buyers might benefit from FHA loans requiring just 3.5% down, while veterans should explore VA loans offering zero down payment and no mortgage insurance. Refinancers need to calculate break-even points where monthly savings offset closing costs, typically requiring at least a 0.75% rate reduction to justify the expense.

Step-by-step process to get lower mortgage rates with wholesale brokers

Engaging wholesale brokers requires a systematic approach that maximizes competition while protecting your interests. Follow these seven steps to secure optimal mortgage pricing:

-

Research and vet multiple wholesale brokers. Start by identifying licensed brokers in your state through the Nationwide Multistate Licensing System registry. Check reviews, verify their lender network size, and confirm they access wholesale pricing rather than retail channels. Interview at least three brokers to compare their approach, transparency about compensation, and willingness to explain rate differences.

-

Submit your complete financial profile. Provide all documentation upfront rather than piecemeal. Complete applications generate accurate rate quotes instead of estimates that change during underwriting. Include explanations for any credit issues, employment gaps, or unusual financial circumstances that might raise underwriter questions.

-

Request itemized quotes from multiple lenders. Ask your broker to shop your scenario with at least five different wholesale lenders. Require detailed breakdowns showing base rate, points, lender fees, and third-party costs. This transparency reveals whether a lower rate comes with offsetting fees that negate savings.

-

Compare total loan costs, not just rates. Calculate the annual percentage rate (APR) for each offer, which includes interest plus fees amortized over the loan term. An offer with a 6.5% rate and $8,000 in fees might cost more than a 6.625% rate with $2,000 in fees, depending on how long you keep the mortgage.

-

Negotiate terms and timing. Once you identify the best offer, ask if the lender will match competitor pricing or reduce specific fees. Discuss rate lock periods, which typically range from 30 to 60 days. Longer locks cost more but protect against rate increases during extended closings. Brokers excel in non-standard scenarios where retail lenders struggle, particularly for refinancing during rate volatility.

-

Lock your rate strategically. Monitor rate trends through your broker. If rates are rising, lock immediately. If falling, consider a float-down option that lets you capture lower rates if they drop before closing, though this feature adds cost. Understand that locks expire, requiring extensions that might increase your rate if closing delays occur.

-

Review final loan estimate carefully. Lenders must provide a standardized loan estimate within three business days of application. Compare it line-by-line against your initial quote. Question any fee increases or changed terms. Federal rules limit how much certain costs can increase between estimate and closing, but lender fees can change if not properly locked.

Pro Tip: Ask brokers about portfolio loans or niche programs if you're self-employed, have recent credit events, or need jumbo financing. These mortgage broker benefits often include access to specialized lenders that retail banks won't offer.

Effective broker relationships require clear communication about your priorities. Specify whether you prefer the lowest rate, minimal closing costs, or fastest closing timeline. These goals sometimes conflict, requiring trade-offs that only you can decide. Prepare smart broker questions covering their lender relationships, average rate spreads versus retail pricing, and how they handle rate changes between application and closing.

Refinancers face unique considerations. Refinancing with brokers works best when you can reduce your rate by at least 0.75%, shorten your loan term without significantly increasing payments, or eliminate mortgage insurance by reaching 20% equity. Calculate break-even by dividing closing costs by monthly savings. If you plan to move within three years, paying points to reduce rates rarely makes financial sense.

Common pitfalls and how to verify you've secured the best mortgage rate

Even informed borrowers make costly mistakes during the mortgage process. Recognizing these errors helps you avoid thousands in unnecessary expenses.

Falling for the lowest advertised rate without examining total costs represents the most common trap. Lenders advertise rock-bottom rates that require paying substantial points upfront or apply only to borrowers with perfect credit and large down payments. A 6.0% rate with $12,000 in points costs more over five years than a 6.375% rate with $3,000 in fees if you sell or refinance before recovering the upfront investment.

Ignoring credit score improvements before applying leaves money on the table. A 40-point score increase from 680 to 720 might reduce your rate by 0.5%, saving $150 monthly on a $400,000 loan. Paying down credit card balances, correcting report errors, and avoiding new credit inquiries for 90 days before applying can significantly improve your rate offer.

Skipping lender comparisons because one broker seems trustworthy creates blind spots. Most borrowers overpay by accepting initial offers without shopping alternatives. Even excellent brokers have lender preferences or compensation arrangements that might not align with your best interests. Getting quotes from multiple brokers introduces competition that benefits you.

Cost comparison: poor versus effective shopping

| Scenario | Rate | Monthly Payment | Closing Costs | 5-Year Total Cost | Savings |

|---|---|---|---|---|---|

| Accepted first offer | 7.00% | $2,661 | $8,500 | $168,160 | Baseline |

| Shopped 2-3 lenders | 6.75% | $2,594 | $6,200 | $161,940 | $6,220 |

| Used wholesale broker | 6.50% | $2,528 | $5,800 | $157,480 | $10,680 |

| Shopped multiple brokers | 6.375% | $2,495 | $4,500 | $154,200 | $13,960 |

Based on $400,000 loan amount, 30-year term, includes principal, interest, and closing costs

Misunderstanding rate locks causes preventable problems. Some borrowers assume verbal agreements constitute locks, only to discover rates increased before formal documentation. Others lock too early, paying extension fees when closings delay, or lock too late and face rate increases during processing. Get rate lock confirmations in writing specifying the exact rate, points, fees, and expiration date.

Neglecting to read loan estimates thoroughly allows errors and unauthorized charges to slip through. The three-page standardized form breaks costs into categories that cannot increase, costs that can increase up to 10%, and costs with no limits. Verify that your loan estimate matches your rate lock agreement. Question any fees you don't understand or that seem excessive compared to market norms.

Verifying you've secured the best available rate requires systematic comparison:

- Calculate the APR for each offer, which reveals true cost including fees

- Request detailed rate sheets showing the lender's full pricing matrix for your scenario

- Compare your broker's quote against direct lender offers for the same loan type

- Check online rate aggregators to confirm your quote falls within competitive ranges

- Ask brokers to explain their compensation and whether they receive higher payments for steering you to certain lenders

- Review the loan estimate's Section A (origination charges) and Section B (services you cannot shop for) for unexpected fees

- Verify third-party costs like title insurance and appraisals match local market rates

Comparing lenders across multiple channels creates pricing pressure that works in your favor. Don't rely solely on broker representations. Independently verify rate competitiveness through direct lender quotes and online resources. This dual approach ensures your broker delivers genuine wholesale pricing rather than retail rates with minimal discounts.

Understanding home loan application tips helps you navigate the verification process efficiently. Maintain organized files of all rate quotes, lock confirmations, and fee disclosures. Create a comparison spreadsheet tracking each lender's terms, allowing quick identification of the best overall value. This documentation proves invaluable if disputes arise about promised rates or if you need to switch lenders mid-process.

Get started with LO FI RATE for low mortgage financing

After learning how wholesale brokers reduce mortgage costs, you need a trusted platform connecting you with licensed professionals who deliver these savings. LO FI RATE low mortgage finance rates specializes in matching homebuyers and refinancers with wholesale brokers offering competitive pricing unavailable through retail channels.

Unlike retail lenders limited to their own rate sheets, LO FI RATE's broker network shops multiple wholesale lenders simultaneously, creating competition that drives your costs down. Their platform handles both purchase financing and refinancing, with specialized programs for first-time buyers, veterans, and borrowers with unique financial profiles. You'll receive transparent pricing breakdowns showing exactly how wholesale access saves money compared to retail alternatives.

The process starts with a no-obligation consultation where licensed brokers review your financial situation and homeownership goals. They'll explain LO FI RATE loan options matching your scenario, from conventional conforming loans to government-backed programs and jumbo financing. Their technology streamlines documentation submission and tracks your application progress in real-time, eliminating the communication gaps that plague traditional mortgage processes.

Pro Tip: Use LO FI RATE's expert team to navigate complex mortgage choices, particularly if you're self-employed, recently experienced credit challenges, or need specialized loan structures. Their wholesale access includes portfolio lenders offering flexibility that retail banks cannot match.

LO FI RATE delivers:

- Fast preliminary approvals typically within 24 hours of complete application submission

- Personalized guidance from licensed brokers who explain options without sales pressure

- Transparent pricing with detailed breakdowns of all costs and fees

- Access to wholesale rate sheets showing real-time pricing across multiple lenders

- Ongoing rate monitoring to capture improvements before closing

FAQ

How long does it take to get a mortgage rate quote from a wholesale broker?

Most wholesale brokers provide initial rate quotes within 24 to 48 hours after receiving your complete financial information. The timeline depends on how quickly you submit required documents and how responsive wholesale lenders are to quote requests. Brokers with established lender relationships often receive faster responses than those working with new wholesale partners.

Can first-time homebuyers get lower rates using wholesale brokers?

Yes, wholesale brokers offer competitive rates and specialized loan programs designed specifically for first-time buyers. They help navigate FHA loans requiring just 3.5% down, conventional loans with first-time buyer assistance, and state-specific programs offering down payment grants or reduced rates. Brokers' access to multiple lenders increases your chances of finding programs that accommodate limited credit history or smaller down payments.

What documents should I prepare to work with a wholesale mortgage broker?

Prepare government-issued photo identification, 30 days of recent pay stubs, two years of complete tax returns with all schedules, two months of bank statements for all accounts, documentation of additional income sources, and details about the property you're purchasing or refinancing. Having these documents organized and ready to submit speeds up the rate quote process and helps brokers provide accurate pricing rather than estimates that change during underwriting.

How can I be sure the mortgage rate I get is the lowest available?

Compare your broker's quote with direct lender offers and carefully review the APR, which includes both interest and fees. Request rate sheets showing the lender's full pricing matrix for your loan scenario, and use multiple broker quotes to create competition. Check online rate aggregators to verify your quote falls within competitive ranges for your credit profile and loan type. Ask brokers to explain their compensation structure and whether they receive higher payments for steering you to certain lenders.