Applying for a home loan in 2026 can feel overwhelming with multiple forms, strict documentation requirements, and confusing terminology. Many homebuyers struggle to navigate the application process efficiently, often missing opportunities for lower mortgage rates. This guide breaks down the home loan application into clear, actionable steps that prepare you for success. You'll learn what documents to gather, how to complete your application correctly, and how wholesale mortgage options can help you secure better rates. By following this structured approach, you'll confidently move through the process and potentially save thousands over your loan's lifetime.

Table of Contents

- Understanding What You Need Before Applying

- Step-By-Step Home Loan Application Process Explained

- How Wholesale Mortgage Options Can Help You Secure Lower Rates

- Common Application Mistakes And How To Avoid Them

- Explore Low Mortgage Rates With Lofirate

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Preparation is essential | Gathering tax returns, pay stubs, bank statements, and credit reports before applying speeds up approval and improves your chances for better rates. |

| Pre-approval matters | Getting pre-approved shows sellers you're serious and often unlocks access to more competitive mortgage rates in 2026. |

| Wholesale saves money | Wholesale mortgage brokers shop multiple lenders to find lower rates compared to retail lenders offering only their own pricing. |

| Avoid common mistakes | Incomplete forms, missing paperwork, and overstating income cause delays that can cost you better rate opportunities. |

| Documentation drives success | Organizing your financial documents digitally and keeping them current ensures a smooth, faster application process. |

Understanding what you need before applying

Before submitting your home loan application, you need to gather specific financial documents that lenders require to verify your income, assets, and creditworthiness. Preparation with correct documentation improves application success and can mean the difference between approval and rejection. Start by collecting your last two years of tax returns, including all schedules and W2 forms. You'll also need recent pay stubs covering at least 30 days, bank statements from all accounts for the past two to three months, and a current credit report from all three bureaus.

Your credit score plays a major role in determining which loan programs you qualify for and what interest rate you'll receive. Most conventional loans require a minimum score of 620, though some government-backed programs accept scores as low as 580. Higher scores above 740 typically unlock the best rates and terms. Understanding where your credit stands before applying lets you address any errors or issues that might hurt your chances.

Different loan types have varying documentation requirements. Conventional loans generally demand the most paperwork, while FHA loans offer more flexibility for borrowers with lower credit scores or smaller down payments. VA loans provide excellent terms for eligible veterans but require military service verification. Jumbo loans for amounts exceeding conformity limits need extensive documentation of assets and income stability.

| Document Type | Purpose | Timeframe Required |

|---|---|---|

| Tax returns | Verify income history and stability | Past 2 years |

| Pay stubs | Confirm current employment and earnings | Most recent 30 days |

| Bank statements | Prove assets for down payment and reserves | Past 2-3 months |

| Credit report | Assess creditworthiness and payment history | Current (within 90 days) |

| Employment verification | Validate job status and income | Current |

Pro Tip: Create a dedicated digital folder with scanned copies of all your documents organized by category. This lets you respond quickly to lender requests and prevents delays caused by searching for paperwork. Keep everything current and update monthly statements as they arrive.

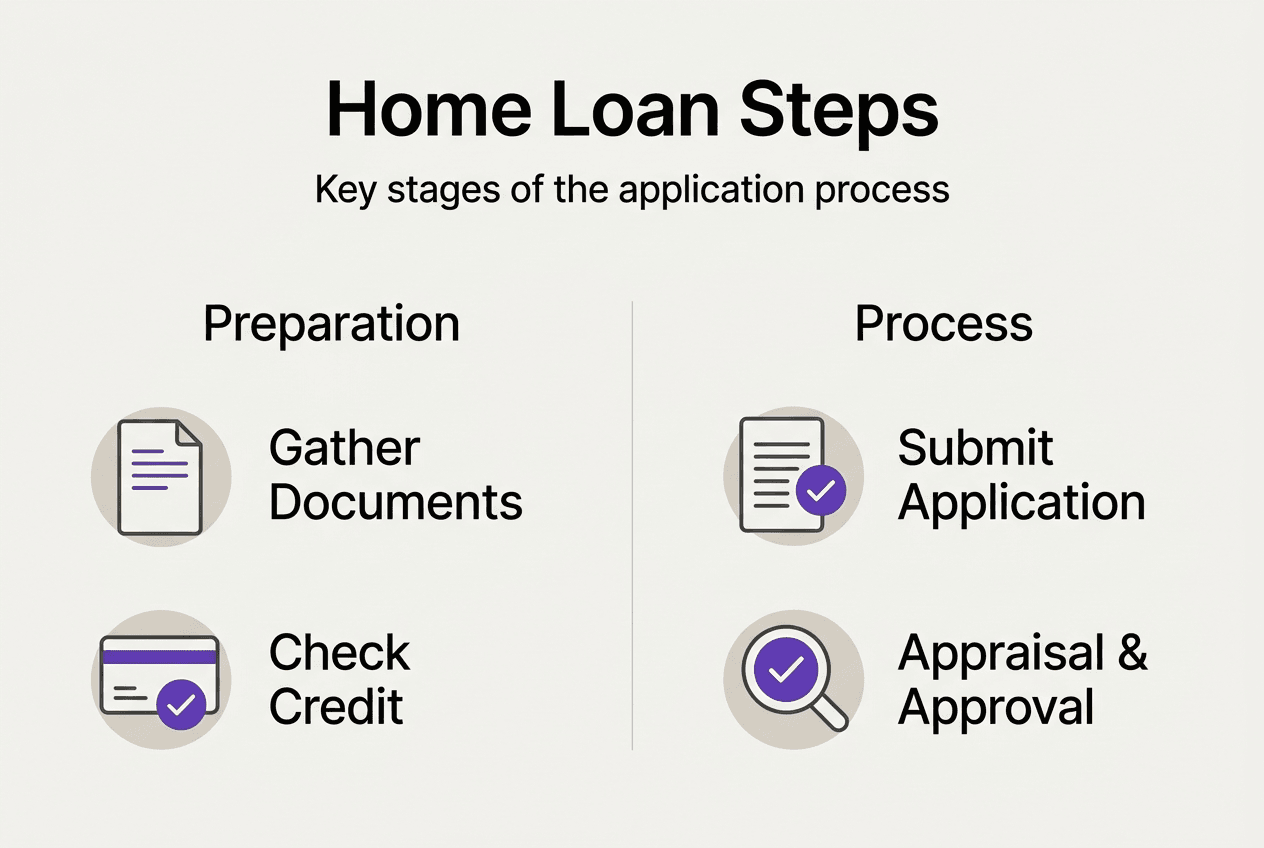

Step-by-step home loan application process explained

Once you've gathered your documentation, you're ready to move through the actual application process. Following a structured loan application process helps avoid common delays and keeps your timeline on track. The process typically unfolds in these sequential steps that build on each other.

- Get pre-approved by submitting your financial documents to a lender or broker who will review your credit, income, and assets to determine how much you can borrow.

- Complete the Uniform Residential Loan Application (Form 1003) with accurate information about your employment, income, assets, debts, and the property you're purchasing.

- Submit all required documentation including the items listed in the previous section, plus any additional paperwork your lender requests based on your specific situation.

- Respond promptly to any requests for clarification or additional documents, as delays here can push back your closing date and potentially affect your rate lock.

- Schedule and complete the home appraisal, which the lender orders to verify the property's value supports the loan amount you're requesting.

- Review and sign your Loan Estimate within three days of application, which outlines your estimated costs, monthly payment, and loan terms.

- Complete the home inspection if required, addressing any issues that could affect the property's value or your ability to secure financing.

- Finalize your loan terms after the underwriter reviews everything and issues conditional approval, addressing any remaining conditions they specify.

- Attend closing where you'll sign final documents, pay closing costs, and receive the keys to your new home.

Communicating effectively with your lender or broker throughout this process prevents misunderstandings and keeps things moving. Ask questions when you don't understand something rather than guessing or leaving fields blank. Respond to emails and calls within 24 hours to show you're engaged and serious about closing on time.

The appraisal and inspection stages deserve special attention because they can uncover issues that affect your loan approval. The appraisal determines whether the home's value supports your loan amount, while the inspection reveals potential problems with the property's condition. If the appraisal comes in low, you may need to renegotiate the purchase price, increase your down payment, or find a different property. Inspection issues might require the seller to make repairs or adjust the price.

Pro Tip: Double-check every entry on your application before submitting it. Simple errors like transposed numbers or misspelled names can trigger verification requests that delay processing by days or weeks. Taking 15 minutes to review everything carefully saves hours of frustration later.

How wholesale mortgage options can help you secure lower rates

Wholesale mortgage lenders operate differently than the retail banks and lenders most homebuyers encounter first. Understanding this difference can save you significant money on your mortgage rate and fees. Wholesale mortgage brokers can provide access to lower rates through lender competition, giving you options that retail lenders simply cannot match.

Retail lenders work directly with consumers and offer only their own loan products at their own pricing. They employ loan officers who earn commissions on the loans they close, and these costs get built into your rate and fees. Wholesale lenders, by contrast, work exclusively through licensed mortgage brokers who can access multiple wholesale lenders simultaneously. This creates competition for your business, which typically results in better pricing.

| Feature | Wholesale Mortgage | Retail Lender |

|---|---|---|

| Lender options | Multiple lenders competing | Single lender only |

| Rate pricing | Lower due to competition | Higher with built-in costs |

| Fees | Typically lower overhead | Higher operational costs |

| Flexibility | More program options | Limited to their products |

| Shopping ease | Broker shops for you | You shop multiple banks |

The advantages of working with wholesale mortgage brokers extend beyond just lower rates. Brokers can match you with specialized loan programs that fit unique situations like self-employment income, investment properties, or credit challenges. They handle the shopping process for you instead of requiring you to apply at multiple banks separately. This saves time and prevents multiple credit inquiries that could lower your score.

Competition among lenders creates downward pressure on rates because each wholesale lender knows the broker can take your business elsewhere. When five lenders are competing for your loan instead of you being limited to one bank's pricing, the lenders sharpen their pencils to win the deal. This competitive dynamic works in your favor, especially in 2026 when rate differences of even 0.25% can mean thousands in savings over a 30-year loan.

Pro Tip: Request rate quotes from at least three different sources, including at least one wholesale broker, to ensure you're getting competitive pricing. Compare not just the interest rate but also the annual percentage rate (APR) and closing costs, as lenders sometimes offset a lower rate with higher fees.

Common application mistakes and how to avoid them

Even with preparation and good intentions, homebuyers frequently make preventable mistakes that delay approval or result in less favorable terms. Awareness of typical mistakes reduces processing delays and rejections, helping you navigate the process smoothly. Recognizing these pitfalls before you encounter them keeps your application on track.

Incomplete applications rank as the most common problem lenders see. Leaving fields blank, providing partial information, or skipping required sections triggers requests for clarification that add days to your timeline. Every blank space needs either information or an explanation of why it doesn't apply to your situation. Read each question carefully and answer completely, even if it seems repetitive or unnecessary.

Missing or outdated documentation causes similar delays. Lenders require current information, typically within 30 to 90 days depending on the document type. Submitting bank statements from four months ago or pay stubs from your previous job wastes everyone's time. Keep your document folder updated with the most recent versions of everything.

- Overstating income or assets to qualify for a larger loan amount almost always backfires when the lender verifies your information and discovers discrepancies.

- Making large purchases or opening new credit accounts during the application process changes your debt-to-income ratio and can disqualify you after initial approval.

- Switching jobs or changing your employment status before closing raises red flags about income stability and may require restarting the approval process.

- Ignoring lender requests for additional information or clarification signals that you're not serious and can result in your application being closed.

- Failing to disclose all debts, including student loans, car payments, or credit cards, creates problems when they appear on your credit report.

Staying organized prevents most of these mistakes. Create a checklist of everything your lender needs and mark items off as you submit them. Set reminders to follow up if you haven't heard back within the timeframe your lender specified. Keep all communication in writing through email so you have a record of what was requested and when you provided it.

Open communication with your lender or broker helps catch potential issues early. If something changes in your financial situation, tell them immediately rather than hoping they won't notice. If you're unsure how to answer a question or what documentation to provide, ask for clarification. Lenders would rather spend two minutes explaining something than two weeks sorting out problems caused by assumptions.

Explore low mortgage rates with LoFiRate

Navigating the home loan application process becomes simpler when you have the right partner supporting your journey. LoFiRate connects you with licensed wholesale mortgage brokers who shop multiple lenders to find competitive rates you won't find at retail banks. Instead of being limited to one lender's pricing, you gain access to a marketplace of options competing for your business.

Our platform focuses on transparency and consumer protection, helping you avoid overpaying through retail pricing. Whether you're purchasing your first home or refinancing to lower your current rate, LoFiRate's network of brokers provides a no-obligation consultation to explore your options. You'll receive personalized guidance through each step of the application process, from gathering documents to closing on your loan. Discover how low mortgage finance rates and flexible loan options can help you achieve your homeownership goals in 2026 while keeping more money in your pocket.

Frequently asked questions

How long does the home loan application process typically take?

The typical home loan application takes 30 to 45 days from application to closing, though this timeline varies based on how quickly you provide documentation and how busy the lender's underwriting department is. Getting pre-approved before house hunting can shorten this timeframe significantly because much of the verification work happens upfront. Complex situations like self-employment income or multiple properties may extend the process.

Can I apply for a home loan with less-than-perfect credit?

Yes, some lenders offer loans for credit scores below 620, though you'll typically face higher interest rates and stricter requirements. FHA loans accept scores as low as 580 with a 3.5% down payment, or 500 with 10% down. Improving your credit score before applying, even by 20 to 40 points, can qualify you for better terms and save thousands over your loan's life. Review your mortgage qualification guide 2026 to understand specific requirements.

What are the benefits of using a wholesale mortgage broker?

Wholesale mortgage brokers access multiple lenders simultaneously, creating competition that typically results in lower rates and fees compared to retail lenders. They shop the market for you instead of requiring you to apply at multiple banks separately, saving time while expanding your options. Brokers can also match you with specialized loan programs for unique situations that retail lenders might not offer. Learn more about wholesale mortgage brokers and how they work.

What documents do I need to start the application process?

You'll need your last two years of tax returns with all schedules, recent pay stubs covering at least 30 days, bank statements from all accounts for the past two to three months, and a current credit report. Additional documents may include employment verification letters, explanations for any credit issues, and proof of other income sources like bonuses or rental income. Having everything organized digitally before you start speeds up the process significantly.

Can I lock my interest rate during the application process?

Most lenders allow you to lock your interest rate once you have a signed purchase agreement and have submitted your complete application. Rate locks typically last 30 to 60 days, protecting you from rate increases while your loan processes. If rates drop during your lock period, some lenders offer float-down options that let you capture the lower rate, though this may come with additional fees. Discuss rate lock options with your lender early in the process.