TL;DR:

- Mortgage compliance laws protect buyers by ensuring transparent fees and fair lending practices.

- Verifying broker licensing and requesting multiple loan estimates helps prevent overpayment.

- New regulations in 2026 focus on borrower data privacy and stricter enforcement of fair practices.

Most homebuyers assume the mortgage process is straightforward — pick a lender, sign some papers, move in. But minorities pay 3 to 5% higher fees through the same broker as white borrowers, and less sophisticated buyers routinely overpay without ever realizing it. The rules designed to protect you are real and enforceable, but they only work if you know how to use them. This guide walks you through why compliance in mortgage brokering matters, which federal regulations are on your side, how to verify your broker is playing by the rules, and what new 2026 laws mean for your privacy and wallet.

Table of Contents

- Why compliance matters in mortgage brokering

- Key mortgage brokering regulations every homebuyer should know

- How you can verify compliance and avoid overpaying

- Current and emerging compliance issues in 2026

- Why knowing the rules puts you in control — what most people miss

- Find a compliant, transparent mortgage match with LoFiRate

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Compliance protects borrowers | Mortgage regulations are designed to keep the process transparent, fair, and safe for homebuyers and homeowners. |

| Know your broker’s credentials | Always verify your mortgage broker's NMLS license and demand clear disclosures to avoid being overcharged. |

| Compare offers to save money | Shopping at least three lenders or brokers gives you better rates and uncovers any unfair fee structures. |

| New rules prioritize privacy | In 2026, data sharing laws expanded protections, so lenders must now obtain your consent before sharing your information. |

Why compliance matters in mortgage brokering

Compliance is not just a box regulators check. It is the mechanism that keeps brokers honest, fees transparent, and access fair. When brokers operate outside the rules, the costs land directly on you.

Three federal laws form the backbone of mortgage compliance. TILA, RESPA, and HMDA require brokers to disclose loan terms clearly, prohibit kickbacks between lenders and brokers, and track lending patterns to expose discrimination. Understanding what each law demands helps you spot when something is off.

Common violations that hurt buyers include:

- Undisclosed fees buried in closing documents

- Steering buyers toward higher-cost loans that pay the broker more

- Missing required disclosures like the Loan Estimate or Closing Disclosure

- Kickback arrangements between brokers and title companies or real estate agents

- Failure to report HMDA data, which masks discriminatory lending patterns

The financial consequences are significant. Overpaying by even half a percentage point on a $400,000 loan adds up to tens of thousands of dollars over 30 years. And the disparity is not random. Research confirms that minorities pay 3 to 5% higher fees through the same broker, pointing to systemic gaps in how compliance is enforced at the individual level.

| Violation type | Impact on buyer | Regulatory response |

|---|---|---|

| Undisclosed fees | Unexpected costs at closing | TILA enforcement |

| Steering to higher-cost loans | Overpayment over loan life | RESPA penalties |

| Missing HMDA reporting | Hidden discrimination | CFPB audit |

| Kickbacks | Inflated service costs | RESPA fines |

Understanding mortgage broker roles is the first step to knowing what you should and should not be paying for.

"Compliance is not protection for regulators. It is protection for you. When brokers follow the rules, you get fair pricing, honest advice, and equal access."

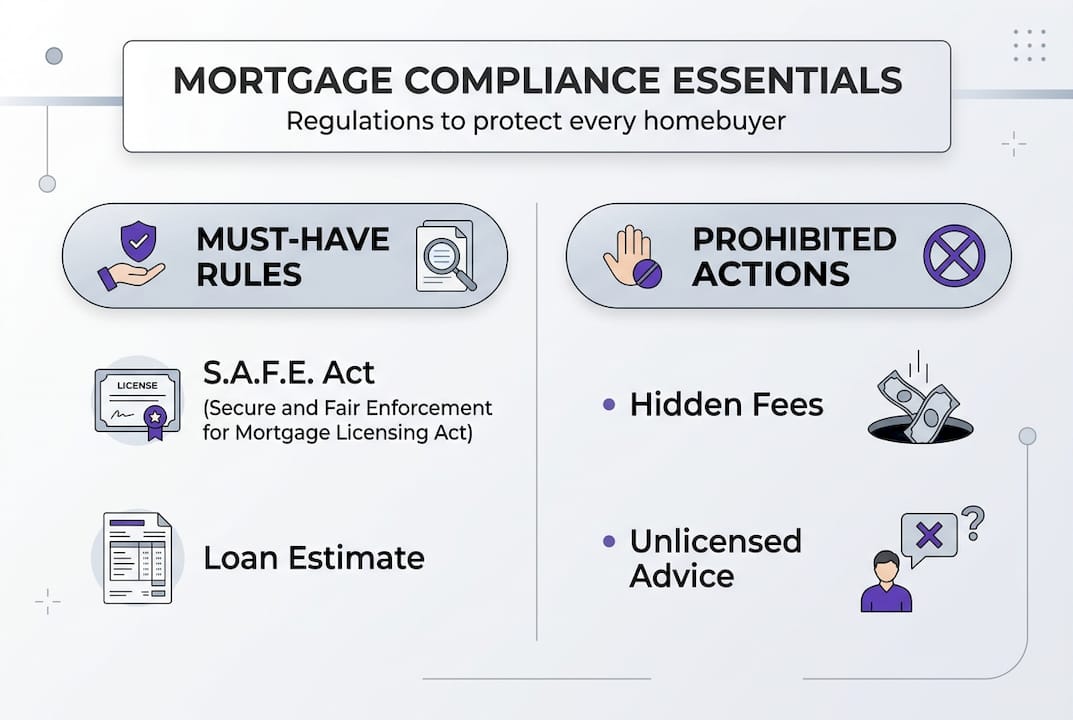

Pro Tip: Before you sign anything, look up your broker on NMLSConsumerAccess.org and confirm they are registered under S.A.F.E. Act rules. No NMLS number is an immediate red flag.

Key mortgage brokering regulations every homebuyer should know

Knowing which rules exist and what they require puts you in a much stronger position at the negotiating table. Here are the four regulations that matter most.

- S.A.F.E. Act — Mortgage brokers and loan originators must be licensed and registered in a national database. This ensures they have passed background checks, completed education requirements, and can be held accountable.

- TILA (Truth in Lending Act) — Requires brokers to give you a standardized Loan Estimate within three business days of your application. It shows the interest rate, APR, monthly payment, and total loan costs in plain language.

- RESPA (Real Estate Settlement Procedures Act) — Prohibits kickbacks, fee-splitting, and referral arrangements that inflate your costs without adding value. It also governs escrow accounts.

- HMDA (Home Mortgage Disclosure Act) — Requires lenders to collect and report demographic data on loan applicants. This data is publicly available and can reveal patterns of discrimination in a given market.

On compensation, the rules are specific. Loan originator compensation cannot be based on loan terms, meaning a broker cannot earn more by steering you into a higher rate. Dual compensation, where a broker is paid by both you and the lender on the same loan, is prohibited. Brokers must also clearly disclose whether they are lender-paid or borrower-paid.

| Regulation | What it requires | What it prohibits |

|---|---|---|

| S.A.F.E. Act | Licensing and registration | Unlicensed origination |

| TILA | Loan Estimate, APR disclosure | Hidden rate changes |

| RESPA | Fee transparency, escrow rules | Kickbacks, fee-splitting |

| HMDA | Data collection and reporting | Concealing lending patterns |

For more detail on CFPB compensation rules, the Consumer Financial Protection Bureau publishes plain-language guidance on what brokers can and cannot charge.

Pro Tip: Never proceed with a broker who cannot provide their NMLS number upfront or who delays sending your Loan Estimate. Both are required by law, and hesitation on either is a serious warning sign. Review the mortgage qualification steps so you know exactly what to expect at each stage.

How you can verify compliance and avoid overpaying

Regulations only protect you if you act on them. Here is a practical, step-by-step approach to protecting yourself from the moment you start shopping.

- Look up the NMLS number. Use the NMLS lookup tool at NMLSConsumerAccess.org to verify your broker's license status, state registrations, and any disciplinary actions.

- Request the Loan Estimate immediately. After submitting an application, you must receive a Loan Estimate within three business days. Review it carefully for the APR, origination charges, and third-party fees.

- Get at least three quotes. Verifying NMLS license and comparing estimates from 3 or more lenders is one of the most effective ways to ensure you are not overpaying. Even a 0.25% rate difference can save you thousands.

- Compare APR, not just the interest rate. The APR includes fees and gives a more accurate picture of total loan cost. Two loans with the same rate can have very different APRs.

- Review HMDA data for your area. Publicly available HMDA data shows lending patterns by race, income, and geography. If a lender shows a pattern of denials or higher rates for certain groups in your area, that is worth noting.

Watch for these red flags:

- No NMLS number provided or broker is evasive when asked

- Vague Loan Estimates that lack itemized fees

- Pressure to use a preferred lender or title company without explanation

- Verbal promises that differ from written disclosures

- Rushed timelines that prevent you from comparing offers

When comparing mortgage rates, focus on the full cost picture, not just the headline rate. And use the right questions for brokers to surface any hidden arrangements before you commit.

Pro Tip: NMLSConsumerAccess.org is free and takes about two minutes to use. Search by name or license number. If a broker's license is expired, inactive, or shows complaints, walk away.

Current and emerging compliance issues in 2026

The compliance landscape is not static. New laws and enforcement priorities in 2026 are changing what brokers must do and what you can demand.

The most significant new development is the Homebuyers Privacy Protection Act, which directly addresses trigger leads. When you apply for a mortgage, your credit inquiry can trigger a flood of unsolicited calls and offers from competing lenders. This law requires your explicit consent before your data can be sold or shared for marketing purposes. It is a meaningful shift toward borrower control.

Other emerging issues include:

- Marketing service agreements (MSAs) between brokers and real estate agents are under increased RESPA scrutiny, especially in high-concentration markets where RESPA violations lead to higher rates

- Anti-kickback enforcement is intensifying, with the CFPB focusing on arrangements that appear legitimate but effectively reward referrals

- Data retention requirements under Regulation Z and Regulation X mandate that brokers and lenders keep records for 5 to 7 years minimum, meaning your loan file must be preserved and accessible if a dispute arises

- Cybersecurity and data privacy are now compliance issues, not just IT concerns. Lenders must demonstrate secure handling of your personal and financial data

"The rules are getting tighter, but enforcement still depends on borrowers knowing their rights and pushing back when something feels wrong."

For a deeper look at what these changes mean for your transaction, the rate transparency guide covers 2026 disclosure requirements in detail. Staying informed about the homebuyer privacy law is one of the simplest ways to protect yourself from the moment you start shopping.

Why knowing the rules puts you in control — what most people miss

Here is the honest truth about compliance in mortgage brokering: the rules help, but they do not automatically protect you. They create a floor, not a ceiling.

The real problem is that brokers with market power extract premiums from buyers who do not shop around. When you accept the first offer, you give up your negotiating leverage entirely. Compliance rules cannot fix that. Only you can.

There is also a nuance that rarely gets discussed. Overly aggressive enforcement and litigation can sometimes make lenders more conservative, which reduces access to credit for borrowers with thin files or non-traditional income. Compliance is not always a simple win for every group. That is why pairing regulatory knowledge with active comparison shopping matters more than most buyers realize.

The buyers who come out ahead are the ones who treat compliance as a baseline, not a guarantee. They check the NMLS, request multiple Loan Estimates, ask pointed questions, and review every disclosure before signing. That behavior shifts the leverage. Explore broker competition strategies to understand how to use market dynamics in your favor. Regulations protect you from the worst outcomes. Your own vigilance determines whether you get the best one.

Find a compliant, transparent mortgage match with LoFiRate

If you have done the reading and want to put this knowledge to work, LoFiRate makes the next step straightforward. The platform connects you with licensed wholesale mortgage brokers who are required to meet strict compliance and transparency standards from day one.

Instead of accepting a single retail quote, you can access brokers who shop multiple lenders on your behalf, giving you real pricing options and the disclosures you are entitled to see. Whether you are buying your first home or refinancing an existing loan, explore mortgage broker matching to find a broker in your state, or review available loan options to understand what products fit your situation. No obligation, no pressure, just transparent access to competitive rates.

Frequently asked questions

How can I check if my mortgage broker is properly licensed?

Verify your broker's NMLS number at NMLSConsumerAccess.org, where you can check their registration and disciplinary history under the S.A.F.E. Act requirements.

What disclosures am I entitled to see before closing a mortgage?

You are entitled to a Loan Estimate, Closing Disclosure, and a clear explanation of broker compensation, all required under TILA disclosure rules.

What is the new Homebuyers Privacy Protection Act?

This 2026 law limits brokers from selling or sharing your data without explicit consent, directly restricting trigger lead practices that flood buyers with unsolicited offers.

How many lender quotes should I compare to get the best rate?

Compare offers from at least three lenders using standardized Loan Estimates so you can make a true apples-to-apples comparison on rate and fees.

Why do some buyers end up paying higher broker fees?

Less informed buyers and minorities are statistically more likely to overpay, often because they do not shop around, as confirmed by research showing 3 to 5% higher fees paid by minority borrowers through the same broker.

Recommended

- How mortgage competition works: save big with broker strategies

- Mortgage qualification guide: clear steps for 2026

- Top questions to ask mortgage brokers for smart homebuying

- What Does a Mortgage Broker Do? Save 0.5% on Rates in 2026

- How to Secure Mortgage for Mallorca Property Easily - ULI & LISA Mallorca Property Blog