Many homebuyers find mortgage pricing confusing, with hidden fees and unclear rate structures creating uncertainty. Understanding mortgage rate transparency helps you navigate interest rates, fees, and loan terms with confidence. This guide explains what mortgage rate transparency means, compares wholesale and retail rates, and shows how clear pricing empowers you to make informed decisions. You'll learn to spot hidden costs, leverage federal protections, and access competitive loan options that fit your financial goals.

Table of Contents

- Understanding Mortgage Rate Transparency

- Wholesale Vs Retail Mortgage Rates: What's The Difference?

- How Mortgage Rates Are Determined And The Role Of Transparency

- Regulations And Tools Promoting Mortgage Rate Transparency

- Explore Mortgage Loan Options With Lo Fi Rate

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Mortgage rate transparency | Clear disclosure of rates, fees, and loan terms protects borrowers from hidden costs. |

| Wholesale vs retail rates | Wholesale mortgage rates typically run lower due to reduced overhead and broker networks. |

| Rate determinants | Credit score, market conditions, loan type, and Federal Reserve policies shape your offered rate. |

| TRID rule protection | Federal disclosure requirements simplify mortgage documents and prevent surprise fees at closing. |

| Comparison strategy | Reviewing Loan Estimate against Closing Disclosure reveals discrepancies and ensures accurate pricing. |

Understanding mortgage rate transparency

Mortgage rate transparency refers to clear, accessible information about interest rates, fees, and terms tied to your home loan. When lenders provide complete upfront details, you can compare options accurately and avoid costly surprises. Transparency builds trust between borrowers and lenders, making the mortgage process less stressful and more predictable.

Lack of transparency leads to higher costs and hidden fees that catch borrowers off guard. Studies show transparent lenders attract more customers because buyers value honesty in such a significant financial commitment. When you understand exactly what you're paying for, you gain negotiating power and confidence.

Full mortgage transparency includes several critical components:

- Interest rate disclosure showing annual percentage rate and how it's calculated

- Origination fees, processing charges, and third-party service costs broken down line by line

- Discount points explaining how upfront payments reduce your rate

- Prepayment penalties that could limit your flexibility to refinance or sell

- Loan structure details covering term length, payment schedule, and any rate adjustment triggers

These elements give you a complete picture of your mortgage's true cost. Without them, comparing lending options becomes nearly impossible. You might think you're getting a great rate, only to discover excessive fees that erase any savings.

"Transparency in mortgage lending isn't just good practice, it's a legal requirement designed to protect consumers from predatory pricing and ensure informed decision making."

Transparent lenders willingly share this information early in the process, often before you submit a full application. They explain how your credit profile affects pricing and which factors you can control to improve your rate. This openness creates a foundation for a successful lending relationship and helps you avoid lenders who rely on confusion to maximize profits.

Regulatory frameworks like mortgage transparency regulation mandate specific disclosure formats and timelines. These rules standardize how lenders present information, making side by side comparisons straightforward. You can review multiple offers knowing each follows the same structure, which simplifies your decision.

Wholesale vs retail mortgage rates: What's the difference?

Wholesale mortgage rates are typically lower because wholesale lenders operate with reduced overhead and distribute loans through broker networks. Brokers shop multiple wholesale lenders on your behalf, creating competition that drives rates down. You access institutional pricing that retail banks reserve for their most profitable customers.

Retail mortgage rates come directly from banks and credit unions serving consumers face to face. These lenders maintain branches, marketing campaigns, and customer service teams that increase operational costs. Those expenses get passed to borrowers through higher interest rates and fees, even when the underlying loan product is identical to wholesale offerings.

The difference often amounts to 0.25% to 0.75% in rate, which translates to thousands of dollars over a 30 year loan. Wholesale lenders focus on volume and efficiency, while retail lenders emphasize brand recognition and convenience. Neither approach is inherently better, but understanding the tradeoffs helps you choose the right path.

| Factor | Wholesale Rates | Retail Rates |

|---|---|---|

| Access | Through licensed mortgage brokers | Directly from banks and credit unions |

| Typical rate range | 0.25% to 0.75% lower | Higher due to overhead costs |

| Customer service | Broker provides personalized guidance | Bank staff assist in branches |

| Lender options | Broker shops multiple wholesale sources | Limited to that institution's products |

| Fees | Broker compensation disclosed separately | Often bundled into rate or origination fees |

When considering wholesale versus retail lending, evaluate these factors:

- Your comfort level working with a broker versus a direct lender relationship

- Whether you prioritize lowest possible rate or convenience of a familiar bank

- How much time you can invest in comparing multiple wholesale offers

- Your need for specialized loan products that certain wholesale lenders offer

- The total cost including both rate and fees, not just the advertised rate

Pro Tip: Always calculate the total loan cost over your expected ownership period, not just the monthly payment. A slightly higher rate with zero origination fees might cost less than a lower rate with substantial upfront charges, especially if you plan to sell or refinance within five years.

Exploring competitive mortgage rates explained reveals how broker networks access pricing unavailable to individual consumers. Wholesale lenders compete aggressively for broker business, knowing brokers will direct volume to the most competitive offers. This market dynamic benefits you when working with a broker who actively shops your loan.

For homeowners considering refinance tips wholesale brokers provide, the wholesale advantage often proves even more significant. Refinance transactions involve less complexity than purchase loans, allowing wholesale lenders to price even more competitively. Understanding mortgage rate regulations ensures your broker operates within legal boundaries and discloses all compensation clearly.

How mortgage rates are determined and the role of transparency

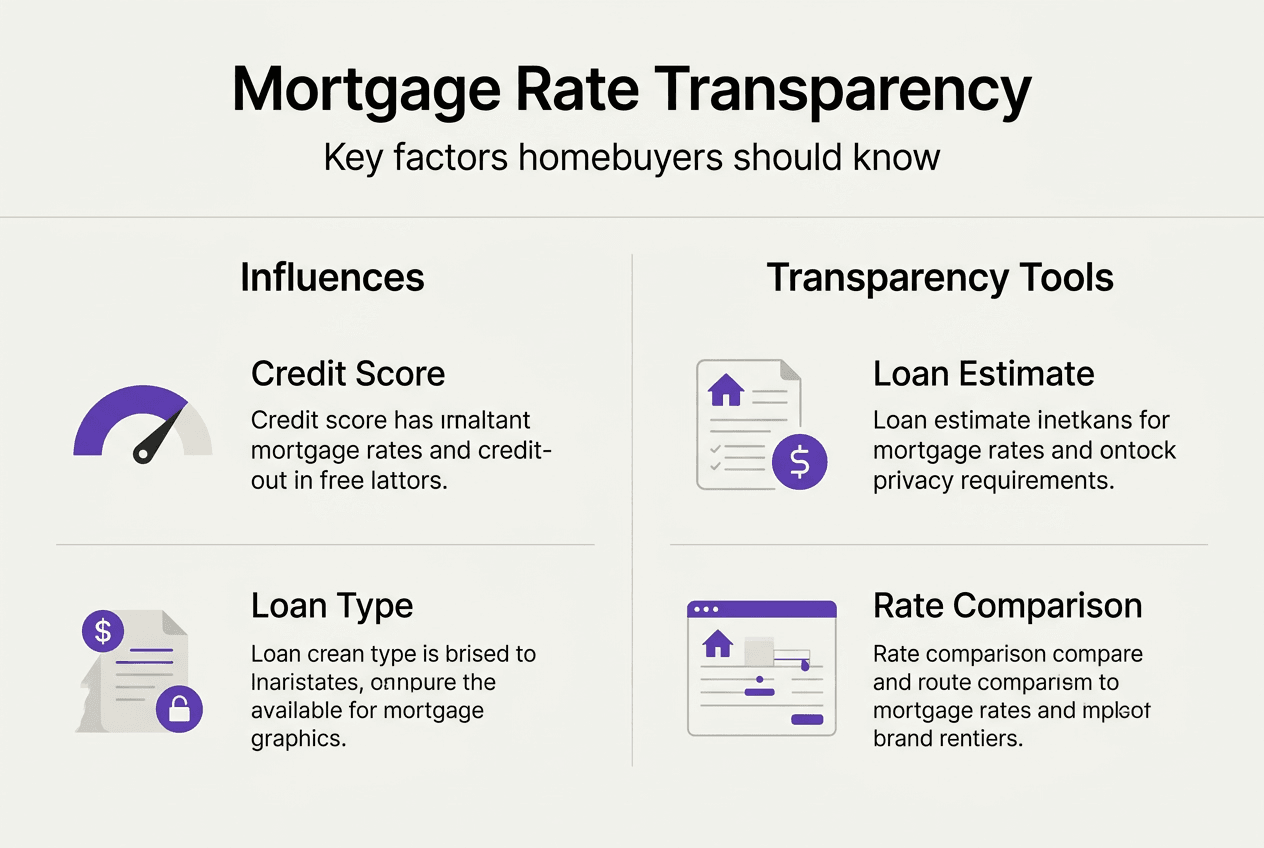

Mortgage pricing is influenced by market rates, loan type, borrower specific factors like credit score and down payment, and Federal Reserve policies. Each element plays a distinct role in shaping your final rate. Market conditions set the baseline, while your personal financial profile determines how much you'll pay above or below that baseline.

Credit scores directly impact your rate because they predict repayment likelihood. Borrowers with scores above 740 typically receive the best pricing, while scores below 680 face rate adjustments that can add 0.5% or more. Lenders price this risk into every loan, making credit improvement one of the most powerful tools for securing better rates.

Loan type matters significantly. Fixed rate mortgages carry higher initial rates than adjustable rate products because lenders assume interest rate risk for 15 or 30 years. Adjustable rate mortgages start lower but expose you to future rate increases, creating a tradeoff between stability and initial savings. Government backed loans like FHA and VA offer competitive rates but require specific qualifications and mortgage insurance.

Down payment size affects your rate because larger down payments reduce lender risk. Putting 20% down eliminates private mortgage insurance and often unlocks better pricing tiers. Borrowers with less than 20% down pay for that additional risk through higher rates or required insurance premiums.

Federal Reserve policy influences mortgage rates through its impact on bond markets and overnight lending rates. When the Fed raises rates to combat inflation, mortgage rates typically follow. When the Fed cuts rates to stimulate the economy, mortgage rates often decline, though the relationship isn't perfectly direct.

Transparency around these factors empowers you to understand exactly why you received a specific rate quote. Lenders should explain which elements you can improve and which remain outside your control. This knowledge helps you decide whether to accept an offer or work on your financial profile before applying.

To understand your personalized mortgage rate, follow these steps:

- Check your credit reports from all three bureaus and dispute any errors that could lower your score.

- Calculate your debt to income ratio by dividing monthly debt payments by gross monthly income.

- Determine your available down payment and whether reaching 20% is feasible with additional savings.

- Research current market trends affecting mortgage rates to understand the baseline environment.

- Request rate quotes from multiple lenders on the same day to ensure accurate comparisons.

- Ask each lender to explain how your credit, down payment, and loan type affected the quoted rate.

After the Federal Reserve's recent rate cut, the average 30 year fixed mortgage rate settled at 6.285%, demonstrating how policy changes ripple through the mortgage market. This rate represents a snapshot in time, with daily fluctuations based on economic data and investor sentiment.

Understanding these determinants positions you to negotiate better terms and avoid surprises. When a lender quotes a rate significantly higher than competitors, you can ask which specific factors drove that pricing. Sometimes the difference reflects legitimate risk assessment, while other times it reveals a lender trying to maximize profit on uninformed borrowers.

Regulations and tools promoting mortgage rate transparency

The TILA RESPA Integrated Disclosure rule combined multiple mortgage disclosures into two simplified forms, making loan costs and terms easier to understand. Known as the Know Before You Owe rule, TRID transformed mortgage transparency by standardizing how lenders present information. This regulation protects borrowers from last minute fee changes and ensures you have time to review terms before closing.

Key disclosures under TRID include:

- Loan Estimate delivered within three business days of application, outlining estimated costs and terms

- Closing Disclosure provided at least three business days before closing, showing final verified costs

- Itemized fee breakdowns separating lender charges from third party services

- Clear explanations of rate lock periods and what happens if rates change

- Projections showing total interest paid over the loan's life

Comparing the Loan Estimate to Closing Disclosure helps catch discrepancies before you sign final documents. Certain fees cannot increase at all, while others can rise only within specific limits. Understanding these rules prevents lenders from sneaking in higher charges at the last minute.

| Disclosure | Purpose | Timing |

|---|---|---|

| Loan Estimate | Provides initial cost and term estimates for comparison shopping | Within 3 business days of application |

| Closing Disclosure | Shows final verified costs and terms before closing | At least 3 business days before closing |

| Rate Lock Agreement | Confirms your locked rate and expiration date | When you lock your rate |

| Appraisal Report | Verifies property value supporting the loan amount | Before closing, copy provided to borrower |

Digital tools have revolutionized mortgage transparency, with platforms like Optimal Blue providing real time pricing data. However, mortgage pricing data has gone digital, raising questions about market manipulation versus genuine transparency. Some industry participants worry that excessive data sharing could enable price fixing rather than healthy competition.

These technological advances allow brokers to compare dozens of lender offers instantly, finding the best combination of rate and fees for your situation. The same tools that empower brokers also create transparency risks if lenders use shared data to avoid competing aggressively. Regulators continue monitoring these platforms to ensure they promote rather than hinder genuine price competition.

Staying informed about mortgage rate trends 2026 helps you time your application when rates favor borrowers. While predicting exact rate movements is impossible, understanding economic indicators gives you context for evaluating offers.

Pro Tip: Keep copies of every disclosure document you receive and review them carefully before signing. If any fees on your Closing Disclosure exceed the amounts on your Loan Estimate beyond allowable tolerances, question the lender immediately. You have the right to delay closing until discrepancies are resolved.

The TRID rule explained in detail shows how these protections work in practice. The three day review period for your Closing Disclosure isn't just a formality, it's your opportunity to verify accuracy and walk away if something seems wrong. Closing Disclosure guidance from the Consumer Financial Protection Bureau outlines your rights and what to do if you spot problems.

Explore mortgage loan options with Lo Fi Rate

Now that you understand mortgage rate transparency, put that knowledge to work by exploring loan options at Lo Fi Rate. Our platform connects you with licensed wholesale mortgage brokers who shop multiple lenders to find competitive rates tailored to your situation. Unlike retail banks limited to their own products, wholesale brokers access institutional pricing that can save you thousands over your loan's life.

Lo Fi Rate prioritizes transparency throughout the mortgage process. You'll receive clear explanations of how your credit, down payment, and loan type affect your rate, with no hidden fees or surprise charges. Our broker network operates under strict disclosure requirements, ensuring you understand exactly what you're paying for and why.

Pro Tip: Use Lo Fi Rate's online tools to compare loan offers side by side, reviewing not just rates but total costs including origination fees, discount points, and closing expenses. This comprehensive view reveals which offer truly delivers the best value for your specific timeline and financial goals.

Whether you're buying your first home or refinancing an existing mortgage, Lo Fi Rate mortgage services provide the transparency and competitive pricing you need to make confident decisions. Our commitment to clear communication and honest pricing helps you avoid the confusion that plagues many homebuyers navigating the mortgage market.

Frequently asked questions

What is mortgage rate transparency and why does it matter?

Mortgage rate transparency means lenders clearly disclose interest rates, fees, and loan terms upfront without hiding costs in fine print. It matters because transparent pricing helps you compare offers accurately and avoid paying more than necessary. When lenders explain how your credit and down payment affect your rate, you can make informed decisions and negotiate better terms.

How do wholesale and retail mortgage rates differ in practice?

Wholesale rates come through brokers who shop multiple lenders, typically offering rates 0.25% to 0.75% lower than retail options. Retail rates come directly from banks and credit unions that maintain branches and marketing campaigns, passing those costs to borrowers. The practical difference is that wholesale access requires working with a broker, while retail offers the convenience of a direct banking relationship.

What are key fees that borrowers should watch for to ensure transparency?

Origination fees, discount points, and prepayment penalties can significantly impact your total loan cost beyond the interest rate. Origination fees compensate the lender for processing your loan, while discount points let you buy down your rate with upfront payment. Prepayment penalties restrict your ability to refinance or pay off the loan early, so understanding these charges prevents costly surprises. Comparing your Loan Estimate to Closing Disclosure reveals whether fees increased beyond allowable limits.

How does the TRID rule protect borrowers from hidden or confusing loan costs?

The TRID rule merged multiple disclosure forms into two standardized documents, the Loan Estimate and Closing Disclosure, making costs easier to understand. It requires lenders to provide the Closing Disclosure at least three business days before closing, giving you time to review and question any discrepancies. This regulation limits how much certain fees can increase from initial estimate to final closing, protecting you from last minute price hikes.

What steps can I take to compare mortgage offers confidently?

Request quotes from multiple lenders on the same day to ensure rate comparisons reflect identical market conditions. Review both the interest rate and total fees on each Loan Estimate, calculating the all in cost over your expected ownership period. Ask lenders to explain how your credit score and down payment affected their pricing, and verify that rate lock terms protect you from increases before closing. Shopping for mortgage lenders with this systematic approach reveals which offer delivers genuine value rather than just an attractive headline rate.