Shopping for a mortgage without comparing rates is like buying a car from the first dealership you visit. Most homebuyers accept the first offer they receive, leaving thousands of dollars on the table. The difference between the best and worst mortgage rates can cost you over $40,000 across a 30-year loan. By understanding how to evaluate multiple offers, analyze total costs beyond interest rates, and leverage wholesale broker access, you can secure financing that saves substantial money while avoiding common comparison pitfalls that trap uninformed borrowers.

Table of Contents

- Key takeaways

- Why you should get multiple mortgage quotes quickly

- Evaluating mortgage offers beyond the interest rate

- How wholesale brokers help you secure better mortgage rates

- Step-by-step guide to comparing mortgage rates effectively

- Save on your mortgage rates with LoFiRate

- How to compare mortgage rates: FAQs

Key Takeaways

| Point | Details |

|---|---|

| Shop multiple quotes | Request five to seven mortgage quotes within a focused window because credit bureaus treat multiple inquiries in a 14 to 45 day span as a single pull. |

| Compare total costs | Evaluate APR and closing costs in addition to the interest rate to see the true long term expense. |

| Wholesale broker advantage | Wholesale brokers can access lower rates by reducing retail overhead, helping you save on fees and pricing. |

| Use a comparison spreadsheet | List each quote's rate, APR, estimated closing costs, and loan features to make side by side decisions. |

Why you should get multiple mortgage quotes quickly

Getting just one mortgage quote is a costly mistake. Research shows that obtaining 5 quotes saves approximately $3,000 over the life of your loan compared to accepting the first offer. The good news is that credit bureaus treat multiple mortgage inquiries within a 14 to 45 day window as a single credit pull, protecting your score while you shop.

This shopping window gives you the freedom to request quotes from multiple lenders without worrying about credit damage. Each lender evaluates your application differently, offers distinct rate structures, and prices their loans based on internal cost models. By comparing at least three to five offers, you expose yourself to a wider range of pricing and increase your chances of finding the best deal.

Timing matters significantly. If you spread your applications across several months, each inquiry counts separately and can lower your credit score by a few points per pull. Concentrate your shopping into a focused period to maximize savings while minimizing score impact.

Pro Tip: Create a spreadsheet before you start shopping. List each lender, their quoted rate, APR, estimated closing costs, and any unique loan features. This simple organization tool helps you track offers and make informed comparisons without relying on memory.

"The difference between shopping one lender versus five can mean the difference between paying $1,200 or $900 monthly on the same loan amount. That $300 monthly savings compounds to tens of thousands over 30 years."

To shop efficiently, prepare your financial documents in advance. Gather recent pay stubs, tax returns, bank statements, and employment verification. Having these ready lets you submit complete applications quickly, ensuring all your quotes arrive within your credit shopping window. Understanding why comparing lenders matters helps you appreciate the value of this preparation.

Consider these tips for shopping lenders as you begin your search:

- Contact lenders on the same day to receive quotes based on similar market conditions

- Request quotes for identical loan types, terms, and down payment amounts

- Ask each lender for a written Loan Estimate within three business days

- Note the lock period for each rate quote, as rates can change daily

- Follow up with questions about any fees or terms you don't understand

The effort you invest in gathering multiple quotes pays immediate dividends. Even if shopping feels time consuming, remember that each additional quote potentially saves you $1,500 or more. That works out to hundreds of dollars per hour for the time you spend comparing offers.

Evaluating mortgage offers beyond the interest rate

The interest rate grabs attention, but it tells only part of the cost story. A 0.5% rate difference on a $360,000 loan saves $41,000 in interest over 30 years, yet focusing solely on rate can lead you to choose a more expensive loan overall. The Annual Percentage Rate captures a fuller picture by including both interest and most loan fees, giving you a standardized comparison metric.

Closing costs vary dramatically between lenders. One lender might quote 3.5% interest with $8,000 in fees, while another offers 3.625% with $3,000 in fees. If you plan to keep the loan for only five years, the second option costs less overall despite the slightly higher rate. Your expected holding period determines which offer delivers better value.

| Cost Component | Lender A | Lender B | Impact |

|---|---|---|---|

| Interest Rate | 3.50% | 3.625% | Lender A lower |

| APR | 3.72% | 3.68% | Lender B lower |

| Closing Costs | $8,000 | $3,000 | Lender B lower |

| Monthly Payment | $1,616 | $1,642 | Lender A lower |

| Total 5-Year Cost | $104,960 | $101,520 | Lender B lower |

This table demonstrates why comprehensive comparison matters. Lender A appears cheaper based on rate and monthly payment, but Lender B costs $3,440 less over five years when you account for upfront fees.

Examine these specific cost elements in every offer:

- Origination fees and points paid to the lender

- Third-party fees for appraisal, title, and escrow services

- Prepaid items like property taxes and homeowners insurance

- Private mortgage insurance if your down payment is below 20%

- Rate lock fees and extension charges

Pro Tip: Ask each lender for a total cost projection based on your expected holding period. If you plan to sell or refinance in seven years, request a calculation showing total payments and fees through year seven. This reveals the true winner for your specific situation.

Some lenders offer rate buydowns where you pay upfront points to lower your interest rate. One point equals 1% of the loan amount and typically reduces your rate by 0.25%. Calculate your breakeven point by dividing the point cost by your monthly payment savings. If you'll keep the loan longer than the breakeven period, buying points saves money.

Understanding why comparing lending options comprehensively matters helps you avoid fixating on rate alone. Use this mortgage rate comparison guide to evaluate all cost dimensions systematically.

Lender fees deserve special scrutiny because they vary widely and are often negotiable. Application fees, underwriting fees, and processing fees can range from zero to several thousand dollars. Some lenders inflate these fees to boost profit margins, knowing many borrowers focus only on interest rates. Question any fee that seems excessive or unclear.

How wholesale brokers help you secure better mortgage rates

Wholesale mortgage brokers operate differently than retail banks, giving you access to institutional pricing typically reserved for high-volume lenders. Wholesale brokers access rates 0.25-0.50% lower than retail banks by eliminating expensive branch networks, advertising budgets, and retail overhead. They connect you with 50 or more wholesale lenders, shopping your scenario across multiple pricing engines to find the best match.

This model works because wholesale lenders price their loans aggressively for brokers who deliver volume. The broker's compensation appears clearly on your Loan Estimate, ensuring transparency. Even after paying the broker, you typically save about $10,000 over the loan lifetime compared to retail bank pricing.

The wholesale channel has grown substantially, now representing a significant share of mortgage originations. This growth reflects borrower recognition that brokers deliver better pricing and service than traditional banks for most scenarios.

"Wholesale brokers serve as your advocate in the lending process, shopping multiple lenders to find pricing you can't access directly. Their compensation is disclosed upfront, and the rates they deliver typically beat retail banks even after their fee is included."

Consider these advantages of working with wholesale brokers:

- Access to 50+ lenders versus one bank's products

- Institutional pricing not available to retail consumers

- Expert guidance through complex loan scenarios

- Faster processing through established lender relationships

- Ability to compare multiple offers from one application

Brokers earn their compensation through lender-paid or borrower-paid models. In lender-paid scenarios, the wholesale lender pays the broker a percentage of the loan amount, and this cost is built into your rate. In borrower-paid models, you pay the broker directly and receive a lower base rate. Both approaches are disclosed on your Loan Estimate, letting you see exactly what you're paying.

Understanding mortgage broker benefits helps you evaluate whether this channel makes sense for your situation. Most borrowers benefit from broker access, especially when purchasing or refinancing in competitive markets.

The Freddie Mac mortgage rate survey tracks pricing across different origination channels, consistently showing that wholesale broker rates compete favorably with retail banks. This data validates the cost advantage of the wholesale model for typical borrowers.

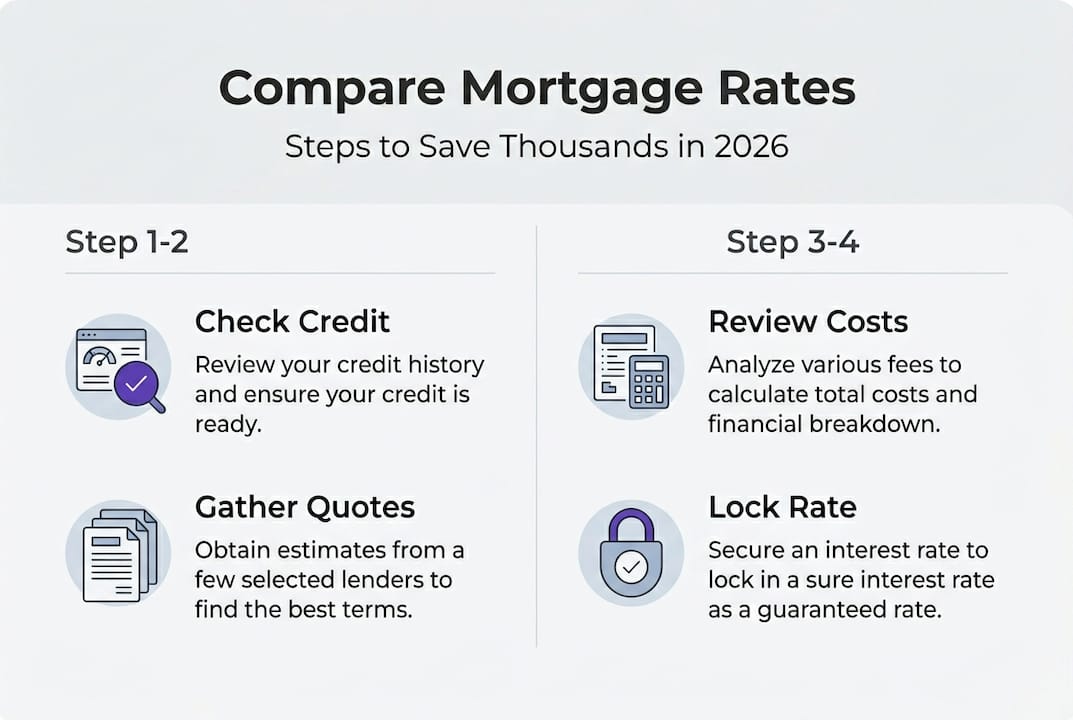

Step-by-step guide to comparing mortgage rates effectively

Start by checking your credit score and report at least 60 days before you plan to shop. This gives you time to correct errors or address issues that might affect your rate. Lenders price loans based on credit tiers, and even a small score increase can lower your rate significantly.

Request prequalification from three to five lenders within your 14 to 45 day shopping window. Provide identical information to each lender, specifying the same loan type, term, down payment, and property details. This standardization ensures you receive comparable quotes.

Use Loan Estimates for standardized comparison of the same loan type, term, and down payment. Federal law requires lenders to provide this three-page form within three business days of your application. The Loan Estimate breaks down costs into clear categories, making comparison straightforward.

Pro Tip: Create a comparison checklist with these items: interest rate, APR, monthly principal and interest payment, total closing costs, lender fees, third-party fees, prepaid items, estimated cash to close, and rate lock period. Score each lender on these dimensions to identify the best overall value.

Follow this sequence for effective comparison:

- Verify each quote uses identical loan parameters

- Compare interest rates and APRs across all offers

- Examine closing costs section by section

- Calculate total cost over your expected holding period

- Evaluate lender reputation and service quality

- Negotiate with top lenders using competing offers

| Comparison Element | What to Check | Why It Matters |

|---|---|---|

| Interest Rate | Quoted rate and lock period | Determines monthly payment |

| APR | Includes rate plus most fees | Shows true borrowing cost |

| Closing Costs | Total on Loan Estimate page 2 | Affects cash needed and overall cost |

| Lender Fees | Section A on page 2 | Often negotiable |

| Monthly Payment | Principal and interest only | Basis for affordability |

Avoid these common pitfalls when comparing offers:

- Comparing different loan types or terms

- Ignoring the rate lock expiration date

- Overlooking prepayment penalties

- Focusing only on monthly payment

- Failing to account for your expected holding period

Once you identify your top choice, ask about rate locks. Most lenders offer 30 to 60 day locks at no cost, with longer periods requiring a fee. Lock your rate when you're satisfied with the offer and confident you can close within the lock period.

Learning how to shop mortgage lenders with wholesale brokers can streamline this process by giving you access to multiple wholesale lenders through a single point of contact.

Save on your mortgage rates with LoFiRate

Comparing mortgage rates takes effort, but the savings justify your time investment. LoFiRate connects you with licensed wholesale mortgage brokers who access institutional pricing from 50+ lenders, delivering rates typically 0.25% to 0.50% lower than retail banks. Unlike traditional lenders offering only their own products, wholesale brokers shop multiple lenders to find competitive options tailored to your scenario.

LoFiRate doesn't lend money or quote rates directly. Instead, it connects you with licensed brokers in your state for a transparent, no-obligation consultation. Whether you're purchasing your first home or refinancing to lower your payment, you can request a second opinion and explore potential savings through wholesale mortgage access. Visit LoFiRate for low mortgage rates to start your comparison, or explore loan options at LoFiRate to see what programs fit your needs. The platform focuses on simplicity, compliance, and consumer protection, helping you avoid overpaying retail pricing.

How to compare mortgage rates: FAQs

When is the best time to shop for mortgage rates?

Shop within a 14 to 45 day window to minimize credit score impact, as multiple mortgage inquiries during this period count as a single pull. Start shopping after you've checked your credit and gathered financial documents, but before you've found a property if possible.

What is a Loan Estimate and why does it matter?

A Loan Estimate is a standardized three-page form that lenders must provide within three business days of your application. It breaks down your interest rate, monthly payment, closing costs, and loan terms in a consistent format, making it easy to compare offers accurately.

Can wholesale brokers really offer better rates than banks?

Yes, wholesale brokers typically access institutional pricing that's 0.25% to 0.50% lower than retail banks because they eliminate branch overhead and advertising costs. Even after broker compensation, borrowers usually save about $10,000 over the loan lifetime compared to retail pricing.

Should I focus on interest rate or APR when comparing?

Focus on both, but prioritize APR for comprehensive cost comparison. APR includes the interest rate plus most loan fees, giving you a fuller picture of borrowing costs. However, also calculate total cost over your expected holding period for the most accurate comparison.

How do I know if I'm getting a competitive mortgage rate?

Compare your quotes against current market averages and obtain at least three to five offers. Ask questions for mortgage brokers about how your rate compares to their average for similar credit profiles and loan types. If your rate seems high, ask what factors are affecting your pricing and whether you can improve your offer.