TL;DR:

- Shopping multiple lenders and using wholesale brokers can save homebuyers thousands over the life of their mortgage.

- Brokers access a wider range of lenders, offer lower rates, and help compare total costs beyond just interest rates.

- Actively comparing 3 to 5 mortgage quotes within a short window maximizes savings and ensures competitive rates.

Most homebuyers overpay by thousands of dollars simply because they accept the first mortgage offer they receive. That's not bad luck. It's a system problem. Retail banks have no incentive to compete for your business if you never ask them to. But borrowers who shop multiple lenders can save thousands over the life of their loan. Wholesale brokers flip this dynamic entirely. They access dozens of lenders at once, creating real competition on your behalf before you ever sign anything. This guide breaks down exactly how mortgage competition works, why brokers are your biggest advantage, and what steps you can take right now to stop leaving money on the table.

Table of Contents

- What is mortgage competition and why does it matter?

- How wholesale brokers create real mortgage competition

- The step-by-step process: Creating competition and comparing offers

- Beyond the basics: When competition matters most

- Market influences and common pitfalls in mortgage competition

- The hidden edge: What most articles miss about mortgage competition

- Ready to unlock smarter mortgage competition?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Shopping saves thousands | Comparing 3-5 mortgage offers can save you over $1,000 to $40,000 over your loan term. |

| Brokers boost competition | Wholesale brokers access many lenders and pass structural savings to borrowers for better rates. |

| Nuanced comparisons matter | Lowest rate is not always best—compare APR, fees, and projected costs for the full picture. |

| Complex loans demand options | Brokers especially outperform banks for jumbo, self-employed, and investment property loans. |

What is mortgage competition and why does it matter?

Mortgage competition is not a vague concept. It means actively collecting multiple loan offers and forcing lenders to fight for your business instead of settling for whatever one lender decides to charge you. Mortgage lender comparison works through standardized Loan Estimates, a federally required document that lets you compare offers side by side on equal terms.

Here's what you're actually comparing when you shop:

- Interest rate: The base cost of borrowing

- APR (Annual Percentage Rate): The true cost including fees

- Closing costs: Origination fees, points, and third-party charges

- Monthly payment: What you'll owe every month

- Loan terms: Length, fixed vs. adjustable, prepayment penalties

Even a small rate difference changes everything. A 0.11% rate reduction on a $400,000 loan saves you roughly $9,000 over 30 years. That's not a rounding error. That's a car payment gone.

"Most borrowers contact only one lender before choosing their mortgage. That single decision costs them more than almost any other financial choice they make that year."

The data backs this up. Getting two extra quotes saves borrowers $600 or more in the first year alone. Over a 30-year mortgage, that compounds dramatically. Yet most families skip this step entirely because they assume all lenders price the same, or they don't want to deal with multiple applications.

Understanding why comparing lenders matters is the first step. The second is knowing how to actually do it. Mortgage shopping explained shows that the process is far simpler than most borrowers expect, especially when a broker handles the heavy lifting. The goal is not to become a mortgage expert. The goal is to use competition as a tool to get a better deal.

The best way to compare mortgage rates starts with understanding what you're comparing and why each number matters to your long-term cost.

How wholesale brokers create real mortgage competition

Retail banks offer you their rates. That's it. One institution, one set of pricing, take it or leave it. Wholesale brokers work completely differently. They have access to daily rate sheets from 50+ lenders and select the best pricing for your specific loan profile, often saving borrowers between 0.125% and 0.50% compared to retail.

That structural advantage comes from how the broker channel is built. Wholesale lenders don't maintain retail branches or run national advertising campaigns. Their overhead is dramatically lower, and those savings flow directly to borrowers through better pricing. Brokers pass that value on because their business depends on delivering competitive results.

Here's how broker-sourced loans compare to retail bank loans:

| Factor | Retail bank | Wholesale broker |

|---|---|---|

| Lenders accessed | 1 | 50+ |

| Rate advantage | Baseline | 0.125%–0.50% lower |

| Loan product variety | Limited | Broad, including specialty |

| Fee transparency | Varies | Disclosed upfront under TRID |

| Complex scenario fit | Often poor | Strong |

Brokers save borrowers $20,000 to $44,000 compared to banks and small lenders over the life of a loan, and they offer the lowest available rate in 78% of borrower scenarios. Those are not marketing claims. That's what the data shows.

When you shop lenders with a broker, you're not just getting more quotes. You're getting better quotes from lenders that retail consumers can't access directly. Wholesale pricing is reserved for the broker channel.

Pro Tip: Under TRID regulations, brokers must disclose their compensation upfront and cannot profit from steering you toward a higher-rate loan. That legal protection means their incentive is aligned with yours.

To get lower rates with a broker, you simply need to connect with one and let them run your scenario across their lender network. Understanding what mortgage brokers do makes it clear why this channel consistently outperforms retail for most borrowers.

The step-by-step process: Creating competition and comparing offers

Knowing what brokers can do, here's how you can use their access and your own savvy to drive true competition and secure the best deal.

- Gather your documents first. W-2s, tax returns, pay stubs, and bank statements. Having these ready speeds up every quote request.

- Request 3 to 5 Loan Estimates within a 14 to 45 day window. Multiple quotes in this window count as a single credit inquiry, protecting your score.

- Compare APR, not just rate. A low rate with high fees can cost more than a slightly higher rate with minimal fees.

- Review the "in 5 years" cost projection. Every Loan Estimate includes this. It's the most honest snapshot of total cost.

- Use competing offers as leverage. Tell each lender what the others offered. Many will sharpen their pricing to win your loan.

- Evaluate lender service. Speed, communication, and reliability matter as much as rate when you're on a closing deadline.

Here's a quick reference for what to compare:

| Loan Estimate section | What to look for |

|---|---|

| Interest rate | Lower is better, but check fees |

| APR | True cost including all fees |

| Closing costs (page 2) | Origination charges and points |

| Projected payments | Monthly cost over loan life |

| In 5 years total cost | Best apples-to-apples comparison |

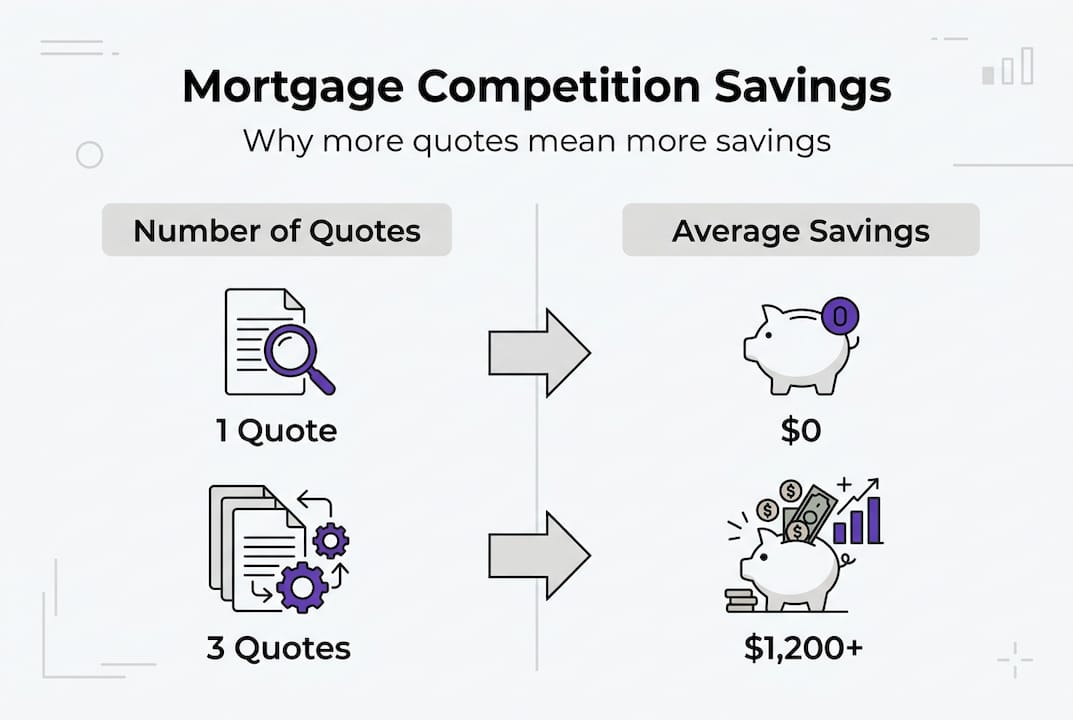

Borrowers who pursue five or more quotes save an average of $1,200 or more. That's real money for a few hours of work.

The biggest pitfall? Assuming your pre-approval rate is your best rate. Pre-approval just confirms you qualify. It is not a competitive offer. Follow the mortgage loan shopping steps and compare mortgage offers carefully before committing.

Beyond the basics: When competition matters most

While everyone can benefit, some situations make competition downright critical. Here's when broker-driven shopping is a must.

For most standard purchase loans, competition saves you money. But for certain borrower profiles, it can be the difference between getting a loan at all and being turned away entirely.

- Jumbo loans: Retail banks often have rigid guidelines and limited jumbo products. Brokers access 50+ lenders including specialty jumbo investors with aggressive pricing.

- Self-employed borrowers: Income documentation is complex. Brokers find lenders who use bank statements or 1099s instead of W-2s.

- Investment properties: DSCR loans and investor-specific products are largely unavailable at retail banks.

- Non-QM borrowers: Recent credit events, foreign nationals, and high-asset borrowers need lenders who understand their situation.

- Rural and underserved markets: Retail bank branches may be scarce; brokers operate remotely and access the same national lender network.

"For a self-employed borrower, one broker with access to 50 lenders is worth more than calling 10 banks directly. Most of those banks will say no."

The dollar impact is substantial. On a $750,000 loan, a 0.25% rate difference saves $75,000 over 30 years. For jumbo borrowers, lender competition scenarios show even larger spreads between the best and worst available rates.

Pro Tip: If your loan is anything other than a straightforward W-2 purchase under conforming limits, always ask a broker to run specialized comparisons before you accept any retail offer. The gap between retail and wholesale pricing widens significantly for complex scenarios.

For jumbo purchases specifically, understanding jumbo loan appraisal requirements is another factor brokers can help navigate, since appraisal standards vary by lender and can affect your approval timeline.

Market influences and common pitfalls in mortgage competition

Even with all these tools, market factors and behavioral pitfalls shape how effective mortgage competition really is.

Mortgage rates are not set by your lender alone. They're driven by mortgage-backed securities spreads in the secondary market, where investors buy bundled home loans. When those spreads widen, rates rise for everyone. When they tighten, rates fall. Wholesale lenders, with lower overhead, can pass more of those improvements to borrowers faster than retail banks.

The competitive landscape is shifting. Banks are re-entering the mortgage market after years of pullback, but non-banks and fintechs still dominate origination volume. More competition among lenders generally benefits borrowers, but only if you're actively shopping.

Here's where many borrowers go wrong:

- Comparing only base rates: Two loans at 6.75% can have wildly different true costs depending on fees and points

- Skipping the APR column: APR is the honest number. Rate is the marketing number.

- Ignoring the 5-year cost projection: This is where short-term vs. long-term tradeoffs become visible

- Stopping at pre-approval: That's qualification, not competition

- Not asking brokers to re-shop at lock time: Rates change daily; a broker can often improve pricing right before you lock

Few borrowers shop effectively despite clear evidence that it saves money. Minorities and rural borrowers face additional barriers, including less access to broker networks and less familiarity with the Loan Estimate process. Awareness is the first step to closing that gap.

Staying informed about market trends and rates and following 2026 mortgage rate trends helps you time your rate lock more strategically.

The hidden edge: What most articles miss about mortgage competition

Most rate-shopping advice stops at "get a few quotes and pick the lowest number." That's not wrong, but it's incomplete. The borrowers who save the most don't just collect quotes. They use those quotes as leverage, ask the right follow-up questions, and know exactly when to push back.

We've watched borrowers walk into a broker consultation with a retail offer in hand and walk out with a rate 0.375% lower simply because they were willing to compare. That willingness to walk away is worth more than any single lender relationship.

Here's the contrarian truth: a flashy ultra-low rate is sometimes a trap. Points, origination fees, and prepayment penalties can make that "great rate" more expensive than a slightly higher rate with no fees. APR and the 5-year cost projection reveal this. Most borrowers never look.

Brokers are not just rate-finders. They're advocates who understand lender overlays, pricing adjustments, and which investors price certain loan profiles best. That knowledge is the real edge. Advanced comparison strategies show that informed borrowers consistently outperform those who rely on rate alone.

Ready to unlock smarter mortgage competition?

If you're ready to put these lessons into practice, getting started is easier than you think.

LoFiRate.com connects you with licensed wholesale mortgage brokers who shop 50+ lenders on your behalf, all in one request. No cold-calling banks. No guessing which lender is best for your situation. Just one submission and multiple competitive offers tailored to your loan profile.

Whether you're buying your first home or refinancing an existing loan, our broker matching services make it simple to access wholesale pricing that most borrowers never see. You can also explore loan options to understand which products fit your goals before you ever speak to a lender. The consultation is free, transparent, and carries no obligation.

Frequently asked questions

How does mortgage competition actually lower my interest rate?

When lenders know you're comparing offers, each one must price competitively to win your business. Shopping multiple lenders consistently lowers rates and fees compared to accepting a single offer.

How many mortgage quotes should I get for maximum savings?

Aim for 3 to 5 quotes within a 2 to 6 week window. Freddie Mac data shows each additional quote typically increases your savings, with five or more quotes averaging $1,200+ in savings.

Are wholesale brokers really better than banks for most mortgages?

Yes. Study data shows brokers offer lower rates in 78% of scenarios and deliver the largest dollar savings, especially for borrowers with complex loan profiles.

Does shopping for multiple quotes hurt my credit score?

No. If you request all mortgage quotes within a 14 to 45 day window, all inquiries count as one for credit scoring purposes, so your score is protected.

Are there special advantages to using brokers for jumbo, self-employed, or investor mortgages?

Absolutely. Brokers have access to far more specialized lenders for jumbo, non-QM, and DSCR loans than retail banks can offer, making them essential for non-standard borrowing situations.