TL;DR:

- Licensed mortgage brokers act as intermediaries who connect borrowers with multiple lenders, not fund or underwrite loans. Their access to wholesale lenders often results in more competitive rates and broader program options compared to retail lenders offering only in-house products. Verifying a broker's license through the NMLS system and understanding their compliance ensures consumer protection and informed borrowing decisions.

Most people assume the person helping them get a mortgage works for the bank. That assumption costs borrowers money every year. The role of state-licensed brokers is fundamentally different from what retail lenders do, and that distinction shapes every part of your mortgage experience, from the rate you receive to the loan programs available to you. Understanding how brokers operate, what they're legally required to do, and why their access to multiple lenders creates real advantages puts you in a much stronger position before you ever sign a loan application.

Table of Contents

- Key takeaways

- The role of state-licensed brokers in mortgage lending

- How brokers differ from retail lenders

- Licensing, compliance, and consumer protection

- Working with a broker: practical benefits and real considerations

- My perspective on what the broker conversation really costs borrowers

- Find a licensed broker through Lofirate

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Brokers are intermediaries, not lenders | Licensed brokers connect you to multiple lenders but never fund or underwrite your loan. |

| Multi-lender access changes rate outcomes | Brokers shop your loan across lenders, creating competition that retail pricing cannot match. |

| Licensing protects you | NMLS registration and SAFE Act requirements mean your broker's credentials are publicly verifiable. |

| RESPA governs broker compensation | Federal law prohibits illegal kickbacks, so broker fees must be tied to actual services performed. |

| Documentation drives your timeline | Closing speed depends more on your document readiness than on how many lenders a broker contacts. |

The role of state-licensed brokers in mortgage lending

A state-licensed mortgage broker is a licensed intermediary. That three-word description carries more weight than it appears to. The broker's entire job is to sit between you, the borrower, and the lenders who actually fund mortgages. They do not own the money. They do not set the final rate in a vacuum. They work on your behalf to find the lender whose product and pricing fits your specific financial situation.

The functions of licensed brokers cover a specific set of activities that move your loan from initial inquiry to lender submission:

- Reviewing your financial profile, including income, credit, and debt ratios

- Matching your situation to suitable loan programs across their lender network

- Preparing and submitting your loan application and supporting documentation

- Acting as your primary point of contact throughout the approval process

- Explaining loan options, disclosures, and rate differences in plain terms

What brokers do not do is equally significant. They do not underwrite your loan. They do not approve or deny your application. Loan funding and underwriting authority stay with the lender, not the broker, even though the broker acts as your main contact through most of the process. This distinction becomes critical when you are comparing who to work with.

On the licensing side, all mortgage brokers must comply with the SAFE Act and register through the Nationwide Mortgage Licensing System, commonly called NMLS. The SAFE Act requires 20 hours of pre-licensing education at minimum, and many states require additional coursework on top of that federal baseline. Brokers must also pass a national exam, submit to background checks, and maintain continuing education annually to keep their license active.

Pro Tip: Before your first meeting with any broker, ask for their NMLS number. You can verify their active license status and any disciplinary history directly through the NMLS Consumer Access portal at no cost.

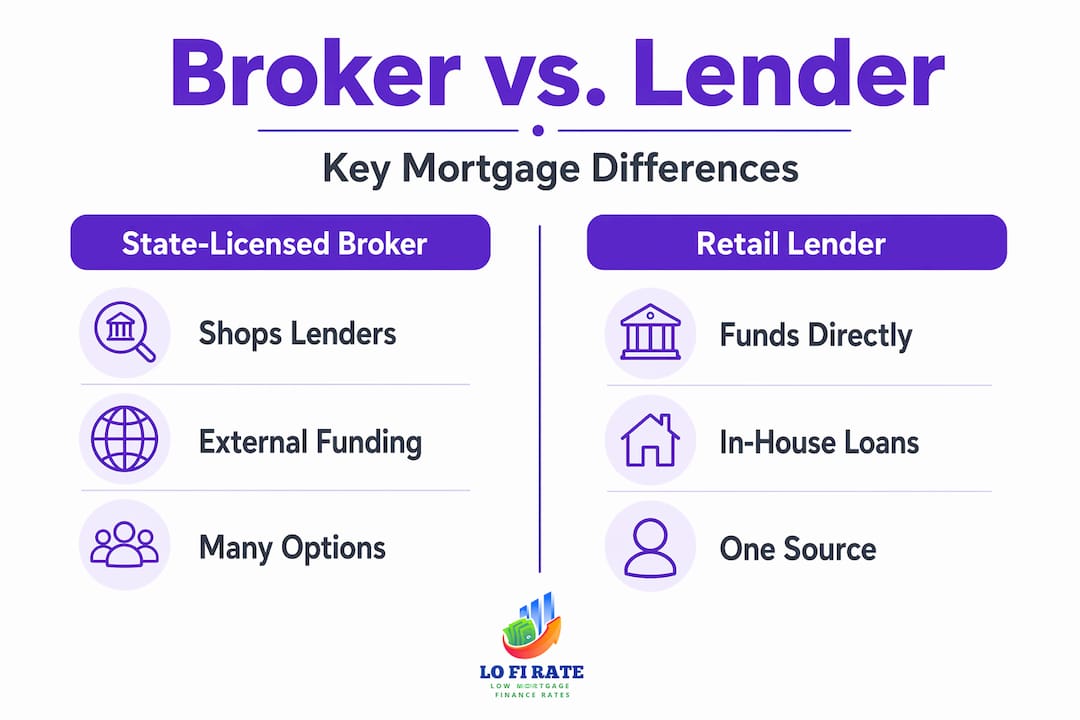

How brokers differ from retail lenders

The simplest way to understand this comparison is to ask one question about any mortgage professional you are considering: who underwrites the loan? If the answer is the company itself, you are talking to a retail lender or mortgage banker. If the answer is a separate lender that the professional submits to, you are talking to a broker.

Retail lenders and mortgage bankers fund loans directly from their own capital or credit lines. That means the rates and programs they offer you come exclusively from their own product shelf. A large bank might have a dozen loan products. A regional credit union might have fewer. Either way, you get what that institution has chosen to offer, nothing more.

| Feature | State-licensed broker | Retail lender |

|---|---|---|

| Loan funding | External lender funds the loan | Lends its own money |

| Product options | Multiple lenders, wider program variety | In-house products only |

| Rate shopping | Submits to competing lenders | One institution's pricing |

| Underwriting authority | Lender handles approval and underwriting | Internal underwriting team |

| Compensation | Paid by lender or borrower via origination fee | Earns spread on funded loans |

| Best for | Complex situations, rate comparison | Borrowers who prefer one-stop banking |

Brokers offer wider loan options by shopping your mortgage across multiple lenders simultaneously, and that competition is the mechanism behind better pricing. When five lenders are all looking at the same borrower file, they compete on rate and terms in ways a single institution never has to. The retail lender's rate is the retail lender's rate. The broker's rate is what the market will actually offer you.

This does not mean retail lenders are always a worse choice. If you have a straightforward financial profile and a long banking relationship with an institution offering genuine loyalty pricing, that can work in your favor. The difference is that you will not know whether their offer is competitive unless you have something to compare it against. A licensed broker's role gives you that comparison built into the process.

Pro Tip: When comparing a broker offer to a retail lender's offer, compare Annual Percentage Rates rather than headline interest rates. APR accounts for lender fees and gives you a truer side-by-side comparison.

Licensing, compliance, and consumer protection

The regulatory framework around state-licensed broker duties exists specifically to protect you, and it is more detailed than most borrowers realize. Three layers of oversight apply to any legitimate mortgage broker operating in the United States.

The first layer is NMLS registration. The NMLS consolidates licensing information for mortgage professionals across all states, making it possible to verify credentials, check for disciplinary actions, and confirm that a broker is legally authorized to originate loans in your state. This single system dramatically reduces fraud risk. Any broker who cannot provide an NMLS number is not operating legally.

The second layer is state-specific licensing. While the SAFE Act creates a federal floor for licensing standards, states layer additional requirements on top of it. These include state-specific exams, surety bond requirements, and varying renewal timelines. Some states have modernized their licensing terminology as well. Hawaii, for example, replaced traditional broker licenses with Mortgage Loan Originator licenses in 2010. Knowing your state's current terminology matters when you are trying to verify someone's credentials.

The third layer is RESPA, the Real Estate Settlement Procedures Act. Section 8 of RESPA directly governs broker referral fees and kickbacks, prohibiting any payment that is not tied to actual services performed. This means a broker cannot legally receive compensation simply for sending you to a particular lender or service provider. Every fee your broker collects must correspond to real work done on your behalf.

Here is what to look for when verifying a broker's standing:

- Confirm their NMLS ID is active through the NMLS Consumer Access portal

- Check your state's financial regulatory agency for any complaints or license suspensions

- Request a Loan Estimate form within three business days of application, which is a legal requirement, not a courtesy

- Ask directly whether the broker is paid by the lender, by you, or both, and get that answer in writing

Working with a broker: practical benefits and real considerations

The clearest benefit of working with a state-licensed broker shows up in complex financial situations. Borrowers with self-employment income, non-traditional credit histories, or lower down payments often struggle to qualify with banks that have rigid in-house criteria. Brokers have access to a broader lender network that includes portfolio lenders, credit unions, and wholesale lenders, many of whom offer programs specifically designed for borrowers who do not fit the conventional mold.

For most borrowers who want to work effectively with a broker, the process goes more smoothly when you approach it with preparation:

- Gather your documents before the first conversation. Two years of tax returns, recent pay stubs, bank statements, and your most recent W-2s will be the minimum. Having these ready prevents delays.

- Be upfront about your credit history. Brokers can only match you to the right lender if they know the full picture. Surprises after application submission slow everything down.

- Ask how many lenders they work with and whether any lenders are excluded from their network. Some brokers have preferred lenders, and you want to know if that affects your options.

- Confirm compensation structure upfront. Brokers are required to disclose how they are paid. Understanding this helps you evaluate whether the loan terms you receive reflect your interests.

- Request written comparisons. A good broker will show you at least two or three loan scenarios side by side so you can weigh rate, term, and closing cost tradeoffs yourself.

One thing borrowers often misattribute to the broker is closing speed. The reality is that documentation readiness drives timelines more significantly than how many lenders a broker contacts. A borrower who submits a complete, clean file closes faster than a borrower with gaps in documentation, regardless of who they are working with.

Pro Tip: Create a digital folder with all your mortgage documents before starting any loan application. Brokers who receive complete files can move to underwriting submission much faster, which directly reduces your closing timeline.

My perspective on what the broker conversation really costs borrowers

I've spent years watching borrowers walk into a mortgage with the wrong mental model. They treat the bank they have a checking account with as the obvious starting point, and because that bank feels familiar and trustworthy, they never ask whether the offer they receive is actually competitive. That default assumption is where significant money gets left behind.

What I've learned is that the broker versus lender distinction is not really a philosophical debate. It comes down to whether you want one institution's pricing or the market's pricing. A licensed broker, operating within state regulations and NMLS oversight, has access to wholesale rates that retail branches are not structured to offer. The compliance framework around licensed brokerage roles is actually a feature here, not a bureaucratic obstacle. Knowing your broker passed a standardized exam, operates under a verified license, and cannot legally accept kickbacks changes the trust dynamic considerably.

Where I've seen borrowers get tripped up is in assuming that working with a broker is slower or more complicated than going direct. In my experience, the opposite is often true when the borrower comes prepared. A broker who genuinely works across multiple lenders is doing the comparison work you would otherwise have to do yourself across multiple bank websites, with no ability to access wholesale pricing anyway. The real cost of skipping that process is not just a slightly higher rate. On a 30-year mortgage, a quarter-point rate difference can mean tens of thousands of dollars in additional interest paid.

— LoFi

Find a licensed broker through Lofirate

Lofirate connects you directly with state-licensed mortgage brokers who have access to wholesale lender networks, the kind that retail bank branches simply do not offer. If you are purchasing a home or considering a refinance, you deserve to know whether your current rate offer is actually competitive. Lofirate does not lend money or quote rates. Instead, it matches you with a licensed broker in your state for a transparent, no-obligation consultation. Explore your loan options through Lofirate and request a second opinion before you commit to any mortgage offer. Visit the Lofirate services page to see how broker matching works and get started today.

FAQ

What does a state-licensed broker actually do?

A state-licensed broker acts as a licensed intermediary who matches borrowers with multiple lenders, prepares and submits loan applications, and guides you through your mortgage options. They do not fund or underwrite the loan themselves.

How is a broker different from a bank or retail lender?

A retail lender funds loans from its own capital and offers only its in-house products, while a licensed broker shops your application across multiple lenders to find competitive rates and programs you would not access directly.

How can I verify a mortgage broker's license?

Look up their NMLS number through the free NMLS Consumer Access portal, where you can confirm active licensing, state authorizations, and any disciplinary history associated with that broker.

Do brokers cost more than going directly to a lender?

Not necessarily. Brokers are often compensated by the lender through wholesale pricing spreads, and the rate savings from multi-lender competition frequently offset or exceed any origination fees involved.

Are mortgage brokers required to disclose their fees?

Yes. Federal law requires brokers to disclose compensation on the Loan Estimate form within three business days of your application, so you can see exactly how and how much your broker is being paid before you commit.