TL;DR:

- Mortgage brokers access wholesale lenders, offering more competitive rates than retail banks.

- Brokers' incentives align with borrowers through commissions tied to loan closings.

- Comparing Loan Estimates ensures transparency and helps avoid broker markups that could inflate rates.

Most homebuyers assume their bank offers the best mortgage rate available. It feels logical: you have a relationship, a history, maybe even a savings account there. But that assumption costs American homeowners real money every year. Wholesale mortgage brokers operate in a completely different lane, accessing lender pricing that retail banks simply don't offer to the public. And the numbers back this up. Broker market share has climbed to 24-26% in 2025, nearly doubling since 2019, which tells you something important: more borrowers are discovering what brokers can actually do.

Table of Contents

- How mortgage brokers operate differently from banks

- Why brokers can offer better rates: competition and access explained

- Potential pitfalls: When broker rates aren't always the lowest

- How to leverage a broker for the absolute best rate

- Our perspective: What most articles miss about broker rates

- Ready to compare rates? Find your best broker match

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Brokers shop multiple lenders | Mortgage brokers look at several wholesale lenders, giving you more choices than a single bank. |

| Broker market share is rising | More Americans are using brokers, with market share nearly doubling since 2019. |

| Not all broker rates are the lowest | While brokers often get better rates, some may add fees or markups, so comparing offers is essential. |

| Practical steps for best rate | Smart homebuyers ask the right questions and check all costs before committing to a broker. |

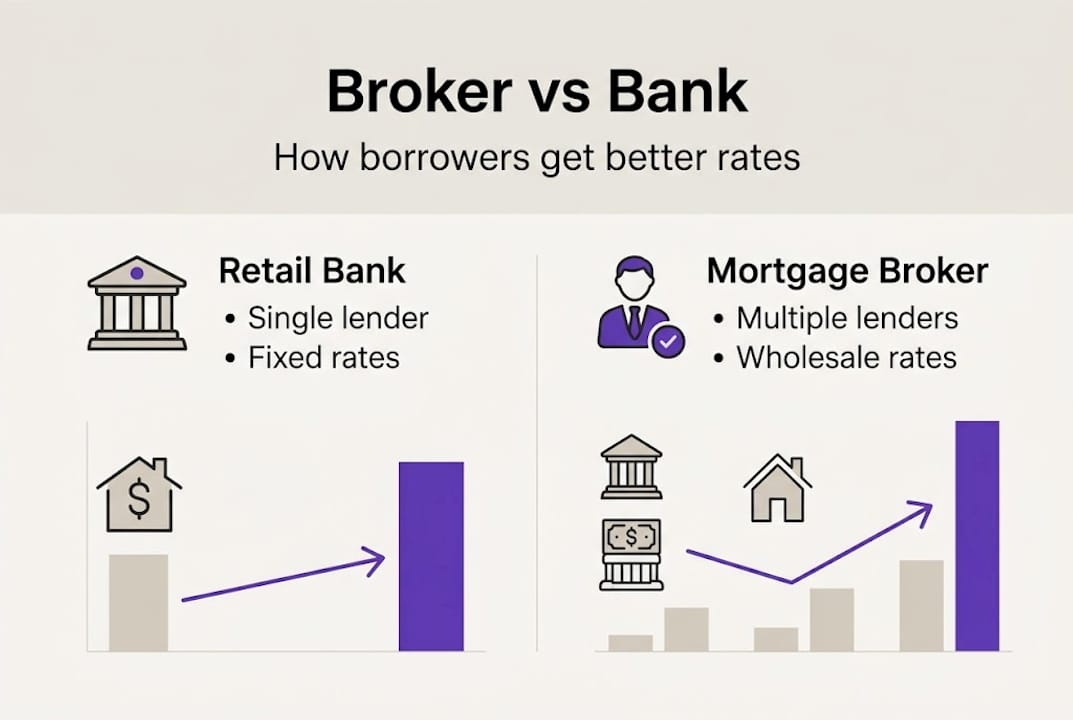

How mortgage brokers operate differently from banks

A mortgage broker is not a lender. That distinction matters more than most people realize. When you walk into a bank, the loan officer sitting across from you works for that bank. Their job is to place your loan with their employer. A broker, on the other hand, works as an intermediary between you and a network of wholesale lenders, shopping your application across multiple institutions to find the best fit.

This structural difference changes everything about how rates get priced. Banks set their own rate sheets and rarely budge. Brokers bring your application to lenders who compete for your business, which creates downward pressure on pricing. Understanding what brokers actually do helps clarify why this model consistently produces better outcomes for borrowers.

Here's a quick comparison of how each model works:

| Feature | Retail bank | Wholesale broker |

|---|---|---|

| Lender options | One (their own) | Multiple wholesale lenders |

| Rate access | Retail pricing only | Wholesale pricing |

| Compensation | Salaried loan officer | Commission on closed loans |

| Flexibility | Limited | Higher |

Broker compensation is also worth understanding. Most brokers earn a commission only when your loan closes, which means their incentive is directly tied to finding you a deal you'll actually accept. Bank loan officers are typically salaried, so their motivation to find you the lowest possible rate is structurally weaker.

The growth in broker activity reflects this advantage. Broker origination share has risen from 14% in 2019 to 24-26% in 2025, while independent mortgage banks now handle 55-65% of originations. Borrowers are voting with their applications.

Key advantages brokers bring to the table:

- Access to wholesale lender networks not open to the public

- Ability to compare multiple loan programs simultaneously

- Flexibility to match loan products to unique borrower profiles

- Incentive structure aligned with closing your loan at a competitive rate

Pro Tip: Before working with any broker, ask directly: how are you compensated, and which lenders are in your network? A trustworthy broker will answer both questions without hesitation.

Why brokers can offer better rates: competition and access explained

The core reason brokers often beat bank rates comes down to two words: wholesale access. Retail banks mark up their rates before presenting them to consumers. That markup covers overhead, branch costs, and profit margin. Wholesale lenders, by contrast, offer pricing that isn't marked up for public consumption because they only work through licensed brokers.

When a broker submits your application to five wholesale lenders, those lenders know they're competing. That competition is the engine behind better pricing. How brokered loans unlock better rates is rooted in this simple dynamic: lenders want your business, and brokers create the environment where they have to earn it.

Here's how brokered and direct bank rates typically compare:

| Factor | Direct bank loan | Brokered loan |

|---|---|---|

| Rate type | Retail (marked up) | Wholesale (lower base) |

| Lender options | One | Five or more |

| Fee transparency | Varies | Loan estimate required |

| Rate negotiation | Rare | Common |

The process a broker uses to maximize your rate advantage typically follows this sequence:

- Collect your financial profile: income, credit, assets, and loan goals

- Submit your scenario to multiple wholesale lenders simultaneously

- Compare rate sheets, fees, and loan terms across all responses

- Present the top options with a clear explanation of trade-offs

- Negotiate with the preferred lender before locking your rate

This is why broker-driven lender competition produces results that a single bank visit rarely can. The market share shift to 24-26% in 2025 reflects borrowers recognizing that shopping through a broker is simply a smarter way to buy or refinance.

"The broker channel thrives because it creates genuine competition at the lender level. When lenders know they're being compared side by side, pricing sharpens in the borrower's favor."

Potential pitfalls: When broker rates aren't always the lowest

Brokers offer real advantages, but they don't come with a guarantee. Not every broker passes along the full wholesale discount. Some add their own markup to the rate, which can partially or fully erase the savings you'd otherwise capture. Knowing this upfront is what separates informed borrowers from those who overpay.

Research confirms this risk is real. One study found that intermediaries can raise effective interest rates through markups, even when they improve the screening and matching process. The efficiency benefit is real, but so is the potential cost if you don't ask the right questions.

Here are the warning signs that a broker's quoted rate may include extra padding:

- The rate is higher than what you've seen advertised elsewhere for your credit profile

- The broker is vague about which lenders they work with

- You're not offered a formal Loan Estimate within three business days of applying

- The broker discourages you from getting a second opinion

- Origination fees seem unusually high relative to the rate offered

The Loan Estimate is your most powerful tool here. Federal law requires lenders and brokers to provide it within three business days of receiving your application. It shows the interest rate, monthly payment, closing costs, and total loan cost over five years. Use it.

Exploring broker strategies for lower costs can help you recognize when a broker is working for you versus padding their commission. And understanding the potential for broker markups means you'll know exactly what questions to ask before you sign anything.

The bottom line: a broker who is transparent about compensation and willing to show you multiple Loan Estimates is almost always working in your interest. One who resists comparison is a red flag.

How to leverage a broker for the absolute best rate

Knowing that brokers can get you a better rate is only useful if you know how to make sure they actually do. The difference between a good broker experience and a great one usually comes down to preparation and the questions you ask before you commit.

Follow these steps to get the most out of working with a wholesale mortgage broker:

- Gather your documents first. W-2s, tax returns, pay stubs, bank statements, and your credit report. Brokers who see a complete file can get sharper pricing from lenders.

- Ask for quotes from at least three lenders. A good broker will show you multiple options. If they only show you one, ask why.

- Request a Loan Estimate from each option. Compare not just the rate but the APR, closing costs, and total interest paid.

- Get a direct bank quote too. Comparing a brokered offer against your bank's best offer gives you real leverage.

- Negotiate. If one lender's rate is lower but another's fees are better, ask your broker to combine the best elements.

Pro Tip: Don't just compare interest rates. Two loans with the same rate can have very different total costs depending on points, origination fees, and closing costs. Always compare the full Loan Estimate, not just the headline number.

For homeowners considering a refinance, the broker advantage is often even larger. IMBs handled 65.4% of purchase and refinance originations in 2024, which shows where the volume and competition actually live. Reviewing smart questions for mortgage brokers before your first meeting puts you in a much stronger position. Learning how to compare mortgage rates effectively, and understanding the full case for using wholesale brokers for lower rates, can make the difference between a good deal and a great one.

Our perspective: What most articles miss about broker rates

Most comparisons between brokers and banks focus entirely on rate. Who got the lower number? That framing misses the bigger picture. The real value a skilled broker brings isn't just a lower rate, it's a loan that actually fits your situation.

Banks are built for the average borrower. Their underwriting is rigid, their products are standardized, and their loan officers have limited room to problem-solve. Brokers work with dozens of lenders, each with different guidelines, and they know which ones favor self-employed borrowers, which ones are lenient on credit score dips, and which ones move fastest for a tight closing timeline.

We've seen borrowers get turned down by their bank and approved at a better rate through a broker the same week. That's not a rate story. That's an expertise story. The refinance guidance from brokers that makes the biggest difference isn't about chasing the lowest number, it's about finding the right lender for your specific profile. That nuance is what most rate comparison articles skip entirely.

Ready to compare rates? Find your best broker match

You've seen how the broker model works, where the savings come from, and how to protect yourself from the pitfalls. Now it's time to put that knowledge to work.

LoFiRate.com connects you with licensed wholesale mortgage brokers in your state who can shop multiple lenders on your behalf. There's no obligation, no pressure, and no retail markup baked into the process. Whether you're buying your first home or refinancing an existing mortgage, you deserve to see what competitive wholesale pricing actually looks like. Find your broker today and get a no-obligation consultation, or explore loan options to understand what programs might fit your situation best.

Frequently asked questions

Do mortgage brokers always provide the lowest rate?

No. Brokers often secure better rates through wholesale access, but some add markups that reduce or eliminate the savings, so comparing a brokered Loan Estimate against a direct lender offer is always a smart move.

How do brokers get access to wholesale mortgage rates?

Brokers are licensed to work directly with wholesale lenders who don't sell to the public, and with broker share at 24-26% of the market in 2025, that network is substantial and competitive.

Can I use a broker to refinance my existing mortgage?

Absolutely. Brokers are well suited for refinancing because they can compare multiple lenders quickly, and with IMBs handling 65.4% of purchase and refi originations in 2024, the wholesale channel is where most of the action is.

What is the main difference between a mortgage broker and a bank loan officer?

A broker shops your application across multiple wholesale lenders to find competitive options, while a bank loan officer can only offer the rates and products from their own institution.