TL;DR:

- Homebuyers often mistakenly assume their real estate agent can handle financing, but only a mortgage broker can access wholesale lender rates. Using a licensed wholesale mortgage broker can save thousands over the loan's lifespan by providing access to more competitive rates and diverse loan options. Choosing a transparent, credentialed broker increases the chances of securing better deals, especially for borrowers with complex profiles or refinancing needs.

Most homebuyers assume their real estate agent is the only broker they need. That assumption can cost you tens of thousands of dollars over the life of your loan. The truth is that two entirely separate types of brokers play two very different roles in your home purchase or refinance, and understanding that distinction is one of the most financially valuable things you can do before signing any mortgage paperwork. This guide breaks down exactly who does what, where the real savings come from, and how to put both types of brokers to work for you.

Table of Contents

- Real estate brokers vs. mortgage brokers: Who does what?

- How wholesale mortgage brokers drive real savings

- Wholesale brokers and refinancing: Unlocking better options

- How to choose and work with a mortgage broker

- The overlooked broker advantage: Why competition is your friend

- Ready to unlock savings? Work with top mortgage brokers

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know each broker’s role | Real estate brokers handle property deals; mortgage brokers secure the best loan terms. |

| Save more with wholesale brokers | Using wholesale mortgage brokers typically means thousands saved on your mortgage. |

| Refinance smartly | Refinancing through brokers unlocks better rates and more flexible options. |

| Choose wisely | Pick licensed, transparent brokers for the best results and peace of mind. |

| Leverage competition | Broker-led lender competition drives rates down further than most realize. |

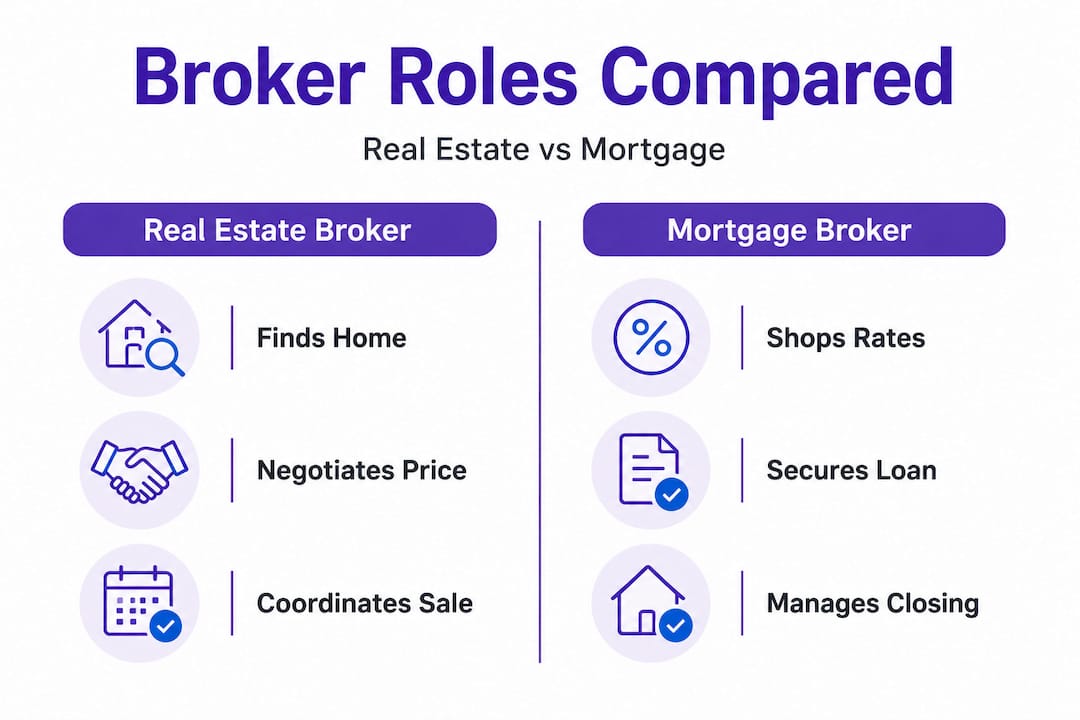

Real estate brokers vs. mortgage brokers: Who does what?

To understand how you can maximize savings, let's first get clear on the two types of brokers involved in the process.

Most people use the word "broker" loosely, which creates genuine confusion. A real estate broker and a mortgage broker are two completely separate professionals with completely different jobs. They sometimes work together on the same transaction, but mixing them up can lead to costly mistakes.

Real estate brokers are licensed professionals who guide buyers and sellers through property transactions. According to Redfin, real estate brokers represent buyers or sellers, providing market knowledge, property showings, negotiations, and guidance through closing. They know neighborhoods, comparable sales, contract terms, and how to negotiate a fair purchase price. Their job is about the property itself.

Mortgage brokers, on the other hand, focus entirely on your financing. They shop wholesale lenders for optimal financing, connecting homebuyers and homeowners to lenders competing for your business. That competition is what drives better rates and better terms.

Here is a simple side-by-side comparison:

| Feature | Real estate broker | Mortgage broker |

|---|---|---|

| Primary role | Buy/sell property | Secure loan financing |

| Paid by | Commission on sale price | Lender or borrower fee |

| Shopping power | Property listings | Multiple wholesale lenders |

| Helps with | Negotiations, contracts | Rates, loan types, approval |

| Involved in | Property transaction | Financing and closing |

In a typical home purchase, both work together. Your real estate broker finds the property and negotiates the deal. Your mortgage broker finds the financing that makes the deal affordable. But here is the part most people miss: your real estate agent cannot replace your mortgage broker. They are not licensed to shop lenders on your behalf, and they do not have access to wholesale pricing.

Understanding what mortgage brokers do is the first step to using them effectively. Once you see the separation clearly, you start to realize exactly where your savings potential lives.

Key benefits of using a mortgage broker specifically include:

- Access to multiple wholesale lenders, not just one bank's products

- Ability to compare loan types including FHA, conventional, jumbo, and VA

- Negotiating leverage because lenders compete for your business

- Independent guidance not tied to selling you a specific bank's product

- Better outcomes for borrowers with unique financial profiles

"The biggest mistake borrowers make is assuming their bank has the best deal. Banks compete to win your business, but you have to give them a reason to compete. That's exactly what a broker does."

How wholesale mortgage brokers drive real savings

Now that you know who does what, let's look at why more homebuyers are turning to wholesale mortgage brokers for financial advantages.

The word "wholesale" matters here. Wholesale mortgage pricing is the rate that lenders offer to brokers, not to the public. It is typically lower than the retail rate you would get walking into a bank branch, because the broker handles much of the origination work and brings volume to the lender. The lender passes some of those savings to you.

How significant are those savings? Industry data shows that wholesale borrowers save roughly $10,000 over the life of their loan, and brokers deliver the lowest available rates in about 78% of lending scenarios. Those are not marginal improvements. On a 30-year mortgage, even a 0.25% rate difference can translate into hundreds of dollars per year.

Here is a data snapshot on what broker access typically delivers:

| Scenario | Retail bank rate | Wholesale broker rate | Estimated 30-year savings |

|---|---|---|---|

| $350,000 loan | 7.25% | 6.85% | ~$9,800 |

| $500,000 loan | 7.10% | 6.70% | ~$14,500 |

| $600,000 loan | 7.00% | 6.60% | ~$17,200 |

These are illustrative figures, but they reflect real patterns. The point is clear: rate differences compound significantly over time.

Of course, brokers are not free. Some charge origination fees or receive yield spread premiums from lenders. But savings outweigh fees for most borrowers who work with licensed, transparent professionals. The key word is "transparent." A broker who clearly discloses how they are compensated and what your total loan costs are is the type of broker worth working with.

The wholesale mortgage savings model works because of lender competition. When a broker submits your loan file to multiple lenders simultaneously, each lender knows they are competing. That dynamic is fundamentally different from walking into a bank and accepting whatever rate they post on the board.

Pro Tip: Before accepting your first mortgage quote from any lender, ask your broker to show you at least three competing loan scenarios. This simple step alone can reveal rate differences that save you thousands.

If you want to learn more about getting lower rates through the wholesale channel, or understand securing better rates as a first-time buyer or repeat borrower, the research consistently points in the same direction: broker access beats single-bank shopping in the vast majority of cases.

Wholesale brokers and refinancing: Unlocking better options

Savings aren't limited to initial homebuying. If you already own your home, brokers can help solve another critical puzzle: refinancing.

When interest rates drop, refinancing becomes one of the most powerful financial moves available to homeowners. And when rates dropped in late 2025, wholesale brokers were again at the center of who captured the best outcomes. According to 2026 mortgage market data, the late 2025 rate environment drove a meaningful pickup in refinancing activity, with wholesale brokers handling both rate-and-term and cash-out refinances effectively.

Rate-and-term refinancing replaces your current mortgage with a new one at a lower rate, reducing your monthly payment. Cash-out refinancing lets you borrow against your home's equity, replacing your mortgage with a larger loan and receiving the difference in cash. Both strategies can be highly effective, and a wholesale broker can find you better pricing on either one than most retail banks offer.

Real estate agents can explain the basics of financing options, as NAR notes, but for the actual rates and loan structures, you need a mortgage broker. This is especially true for borrowers with non-prime credit, self-employment income, or recent financial events. Those borrowers often get turned down by retail banks but approved through wholesale lenders that brokers access.

Here is how the refinancing process typically works when you partner with a wholesale broker:

- Initial consultation: You share your current loan details, credit profile, and goals with the broker.

- Market analysis: The broker pulls quotes from multiple wholesale lenders based on your specific situation.

- Loan comparison: You review competing offers side by side, comparing rates, terms, and closing costs.

- Application: You submit your documents to the selected lender through the broker.

- Underwriting: The lender reviews your file; the broker monitors and advocates for smooth processing.

- Closing: You sign the new loan documents and your refinance is complete.

This process is often faster and less stressful than going directly to a retail bank, because your broker manages the communication and troubleshooting between you and the lender. Refinancing with wholesale brokers is a well-documented path to meaningful monthly savings, and steps to refinancing are simpler than most homeowners expect.

Pro Tip: If you refinanced in 2021 or 2022 when rates were near historic lows, you probably don't need to refinance now. But if your current rate is above 7%, it may be worth having a broker run the numbers to see if a lower rate justifies the closing costs.

How to choose and work with a mortgage broker

Understanding the value is one side; actually choosing a broker you can trust is the next, and just as important.

The mortgage industry is licensed and regulated, but not all brokers operate with the same level of transparency. Choosing the right broker is not just about finding the lowest rate quote. It is about finding a professional who will give you honest information, clearly explain your costs, and advocate for your best outcome throughout the process.

Here is what to look for and ask before committing to a broker:

Licensing and credentials:

- Confirm your broker holds an active NMLS (Nationwide Multistate Licensing System) license in your state

- Verify their license status at the NMLS Consumer Access website

- Ask how long they have been in business and what loan volume they handle

Wholesale lender access:

- Ask how many wholesale lenders are in their network

- A strong broker typically works with 20 or more lenders, giving you genuine shopping power

- Ask if they have access to lenders who specialize in your loan type (FHA, VA, jumbo, etc.)

Fee transparency:

- Request a written fee disclosure before submitting any documents

- Ask whether they earn a lender-paid or borrower-paid compensation, and what the total is

- Compare total loan costs across scenarios, not just interest rates

Communication and responsiveness:

- A good broker explains loan options in plain language without pressure

- They respond promptly and keep you informed throughout the process

- They will tell you when a deal doesn't make sense for you, not just when it does

As research confirms, the savings brokers generate outweigh their fees for most borrowers, but that outcome depends entirely on working with a licensed, transparent professional. Cutting corners on broker selection can erase the financial benefit.

When it comes to document readiness, gather your W-2s, pay stubs, tax returns, and bank statements before your first broker meeting. This speeds up the process significantly and puts you in a stronger position to act when a great rate becomes available. Shopping lenders with brokers becomes much smoother when your paperwork is ready to go.

The overlooked broker advantage: Why competition is your friend

Beyond the basic mechanics, there is a piece of the broker puzzle that most guides don't discuss, so let's tackle it head-on.

Conventional wisdom says you should call a few big banks, compare their rates, and pick the lowest one. That advice sounds logical. It is also incomplete. What that approach misses is that the rates banks show you directly are retail rates, priced to include their full margin. When you go through a wholesale broker, lenders are bidding against each other using their wholesale pricing, which is inherently more competitive.

The real insight here is that it is not just negotiation that drives lower rates. It is competition structure. A borrower calling one bank at a time is in a weak negotiating position. A broker submitting your loan profile to 15 lenders simultaneously creates a fundamentally different dynamic. Those lenders compete via brokers in ways they simply will not when you approach them directly.

This matters even more for borrowers with complex financial profiles. If you are self-employed, have a recent credit event, carry significant investment income, or are buying a non-standard property type, retail banks often have rigid guidelines that result in denials or punitive rates. Wholesale lenders accessed through brokers often have more flexible underwriting and more appetite for diverse loan profiles. That flexibility can be the difference between an approval and a rejection.

The path to avoiding retail rates is not complicated, but it requires knowing that a better option exists. Most borrowers simply don't realize that lender competition is the engine behind better rates, not just individual negotiation at a single institution.

We think the most underutilized move in real estate finance is simply asking for a second opinion from a wholesale broker before closing. It costs nothing, takes very little time, and the potential upside is significant. If your current lender has the best deal, you lose nothing. If they don't, you could save thousands.

Ready to unlock savings? Work with top mortgage brokers

With the full picture of how brokers can benefit your real estate journey, the next step is simple.

Whether you are buying your first home, upgrading to a larger property, or thinking about a refinance, the right wholesale mortgage broker can put thousands of dollars back in your pocket. The data is clear, the process is straightforward, and the only thing standing between most borrowers and better rates is access.

At LoFiRate.com, we connect homebuyers and homeowners with licensed wholesale mortgage brokers in their state, at no obligation and no cost to get started. You can find the right broker for your situation quickly, or explore loan options currently available in your market. Our platform is built on transparency and consumer protection. We do not quote rates or lend money directly. We simply give you access to the professionals who can shop the market on your behalf and help you avoid overpaying at retail pricing.

Frequently asked questions

What is the main difference between a real estate broker and a mortgage broker?

A real estate broker helps buy or sell property, while a mortgage broker connects you to lenders competing for your loan business. One handles the transaction; the other handles your financing.

How much can I really save by using a wholesale mortgage broker?

Industry studies show that wholesale borrowers save roughly $10,000 over the life of their loan, and brokers deliver the lowest available rates in about 78% of scenarios compared to retail lenders.

Do brokers charge extra fees, and are they worth it?

Most borrowers still come out ahead financially even after broker fees. Research confirms that savings outweigh fees for the majority of borrowers, but always ask for written fee disclosures upfront before moving forward.

How do I pick a trustworthy mortgage broker?

Start by verifying their license through the NMLS Consumer Access database, request a fee disclosure before submitting any documents, and ask how many wholesale lenders are in their network.

When should I work directly with a bank instead of a broker?

Direct bank relationships occasionally make sense for highly qualified borrowers with straightforward loan needs and an existing banking relationship that comes with loyalty pricing. For most other borrowers, especially those with complex income or credit profiles, a wholesale broker delivers better outcomes.