TL;DR:

- Brokered loans provide access to wholesale rates by comparing multiple lenders, often saving money.

- The process involves a broker assessing finances, matching lenders, negotiating terms, and guiding approval.

- Despite fees, brokered loans can offer better long-term savings than retail options.

Most homebuyers assume that using a mortgage broker adds another layer of cost to an already expensive process. That assumption costs people real money. A brokered loan is a loan facilitated by a third-party broker who matches borrowers with multiple lenders to secure favorable terms, without the broker lending money directly. Instead of walking into one bank and accepting whatever rate they offer, you get access to a network of wholesale lenders competing for your business. This article breaks down exactly how brokered loans work, what they cost, and how to use them to your advantage.

Table of Contents

- What is a brokered loan?

- How does the brokered loan process work?

- Costs and savings: fees, rates, and broker compensation

- Pros and cons of brokered loans for homebuyers

- What most borrowers miss when using a brokered loan

- Get expert support for your next mortgage

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Brokers connect borrowers | A brokered loan uses a third-party broker to match you with lenders for the best terms. |

| Lower rates possible | Brokers often access wholesale rates unavailable to direct bank customers, potentially saving you money. |

| Fees are regulated | Broker fees are typically 1-2% and must be clearly disclosed and regulated for your protection. |

| Process adds options | Working through a broker means more lender choices and potentially less legwork for you. |

| Choose your broker wisely | Not all brokers have equal access—ask about their lender panel and compensation structure. |

What is a brokered loan?

A brokered loan is not a special loan product. It is a standard mortgage, but the way you access it is different. Rather than going directly to a bank or lender, you work with a licensed mortgage broker who acts as the middleman between you and a pool of lenders.

The broker does not lend you money. Their job is to understand your financial situation, match you with lenders who fit your needs, and negotiate terms on your behalf. Think of it like hiring a buyer's agent for your mortgage instead of walking into a single dealership and accepting the sticker price.

Brokers access what are called wholesale mortgage rates. These are rates that lenders offer exclusively through broker channels, not to the general public. Retail loans, by contrast, come directly from banks or lenders at their posted public rates. Understanding what mortgage brokers do clarifies why this distinction matters so much for your final rate.

Brokered loan vs. retail loan at a glance:

| Feature | Retail loan | Brokered loan |

|---|---|---|

| Who you work with | Bank or lender directly | Licensed mortgage broker |

| Rate access | Public retail rates | Wholesale rates from multiple lenders |

| Lender options | One institution | Many lenders compared |

| Negotiation | Limited | Broker negotiates on your behalf |

| Transparency | Varies | CFPB-regulated disclosures required |

Key characteristics of brokered loans:

- The broker is not the lender and does not fund your loan

- You get access to wholesale pricing not available to the public

- Multiple lenders compete for your business

- The broker handles most of the lender communication

- Fees and compensation must be disclosed upfront

- Brokered loans are available for purchases and refinances

The core advantage is simple: more options mean more competition, and more competition typically means better terms for you.

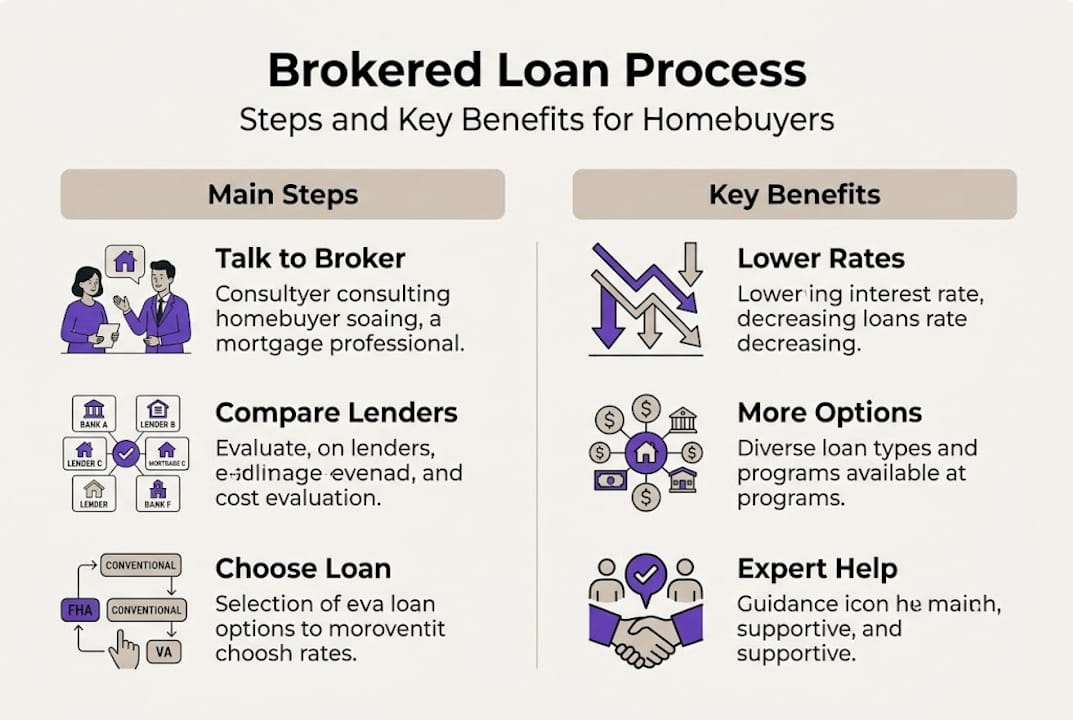

How does the brokered loan process work?

The brokered loan process follows a clear sequence. Knowing each step removes the mystery and helps you stay in control throughout.

Step-by-step breakdown:

- Initial broker consultation. You meet with a licensed broker to discuss your goals, budget, and timeline. This is where you share your financial picture and ask about their lender network.

- Financial assessment. The broker reviews your income, credit score, debt load, and assets. This shapes which lenders and loan programs are realistic options for you.

- Lender matching. Using their wholesale lender access, the broker identifies lenders whose products and pricing fit your profile. This is where the brokered loan model earns its value.

- Rate and terms negotiation. The broker negotiates with multiple lenders simultaneously. You see competing offers rather than a single take-it-or-leave-it quote.

- Application and documentation. Once you choose a lender, the broker helps you complete the formal application and gather required documents. They act as your point of contact with the lender.

- Underwriting and approval. The lender reviews your file. The broker follows up, responds to conditions, and keeps things moving.

- Closing. You sign final documents and the lender funds the loan. The broker's role wraps up here.

One thing buyers often miss: the broker communicates with the lender on your behalf throughout this process. You are not left navigating lender portals or phone trees alone.

Knowing the right questions to ask a broker before you start saves time and sets expectations clearly.

Pro Tip: Ask your broker how many lenders they actively work with and whether they have any preferred or exclusive lender relationships. A broker with access to 30 or more wholesale lenders gives you meaningfully more options than one working with just a handful.

Costs and savings: fees, rates, and broker compensation

The cost question is where most people get nervous. Here is the reality: brokers earn money, but the structure is regulated and often offset by the savings they generate.

Broker compensation typically runs 1 to 2% of the loan amount, paid either through a lender commission, a borrower-paid fee, or a combination of both. The Consumer Financial Protection Bureau (CFPB) regulates how brokers are compensated and requires full disclosure of all fees before you commit.

The key insight is that wholesale rates are often lower than retail rates even after broker compensation is factored in. That gap is where your savings live. Accessing lower rates with wholesale brokers can translate to thousands of dollars saved over the life of a loan.

Rate and fee comparison example (based on a $400,000 loan):

| Item | Retail loan | Brokered loan |

|---|---|---|

| Interest rate | 7.25% | 6.85% |

| Monthly payment (30-yr) | $2,729 | $2,630 |

| Monthly savings | — | ~$99 |

| 10-year interest savings | — | ~$11,880 |

| Broker fee (1.5%) | None | $6,000 |

| Net 10-year benefit | — | ~$5,880 |

Note: Rates are illustrative. Actual rates vary by credit profile and market conditions.

Even with a broker fee, the math often works in the borrower's favor over time. Exploring competitive mortgage rates through a wholesale broker is one of the most direct ways to reduce your long-term housing costs.

Fees you may encounter with a brokered loan:

- Origination fee: Covers broker compensation, typically 1 to 2% of the loan

- Processing fee: Charged by the lender for handling the file

- Appraisal fee: Paid to a third-party appraiser to value the property

- Title and escrow fees: Standard closing costs present in all loan types

- Credit report fee: Small charge for pulling your credit

Most of these fees exist in retail loans too. The difference is that with a brokered loan, all broker-related compensation must be disclosed clearly and early.

Pros and cons of brokered loans for homebuyers

No mortgage path is perfect for everyone. Here is an honest look at both sides.

Advantages of brokered loans:

- Rate shopping at scale. Your broker compares multiple lenders at once, something most borrowers lack the time or access to do themselves.

- Wholesale access. Rates available through brokers are often not accessible to the public directly.

- Personal service. A good broker is your advocate, not a lender's sales rep.

- Flexibility. Brokers can match borrowers with niche programs, including those for self-employed buyers or people with less-than-perfect credit.

- Time savings. One application goes to multiple lenders rather than filling out separate forms at each bank.

Potential drawbacks:

- Added process layer. Communication goes through the broker, which can slow things down if the broker is not responsive.

- Documentation demands. Some lenders accessed through brokers may require more paperwork than a direct retail lender.

- Not all lenders participate. A few large banks do not work with brokers, so those options may not be on the table.

- Broker quality varies. A less experienced broker may not have strong lender relationships or negotiating leverage.

Pro Tip: Ask any broker upfront whether they are restricted from working with specific lenders. Some brokers operate on limited panels, which reduces your options without you realizing it.

Understanding lender competition is what makes the brokered model powerful. When lenders know they are competing against each other for your loan, they sharpen their pricing. And understanding mortgage rates in general helps you evaluate what you are actually being offered.

"A brokered loan is a loan facilitated by a third-party broker who matches borrowers with multiple lenders to secure favorable terms, without the broker lending money directly." — Brokered Loan Definition

What most borrowers miss when using a brokered loan

Here is something worth saying plainly: not all brokers are equal, and treating them like they are is one of the most common mistakes buyers make.

Brokers vary significantly in how many lenders they access, how aggressively they negotiate, and whether they have conflicts of interest tied to preferred lender relationships. A broker working with 10 lenders and a broker working with 50 lenders are not offering you the same service, even if both call themselves wholesale brokers.

Smart borrowers also use their broker relationship beyond the initial purchase. Brokers can monitor rate movements and flag refinancing opportunities when conditions shift in your favor. That ongoing relationship has real financial value that most first-time buyers never tap.

The fine print matters too. Compensation structures, lender panel restrictions, and fee disclosures all affect your outcome. Most buyers skim past these details. Staying compliant with brokers and understanding the regulatory framework gives you leverage in the relationship.

Treat your broker choice as seriously as your lender choice. The right broker is a long-term financial ally, not just a one-time transaction facilitator.

Get expert support for your next mortgage

If you have read this far, you already understand more about brokered loans than most buyers walking into a bank. The next step is putting that knowledge to work.

LoFi Rate connects homebuyers and homeowners with licensed wholesale mortgage brokers who shop multiple lenders on your behalf. There is no obligation and no cost to connect. Whether you are buying your first home or exploring a refinance, our mortgage broker matching services make it easy to get a second opinion on your rate. You may be surprised how much room there is between what a retail lender quotes and what a wholesale broker can find. Take a few minutes to explore loan options and see what is actually available to you.

Frequently asked questions

Who actually funds a brokered loan?

With a brokered loan, the funding comes directly from the lender your broker selects, not from the broker. The broker simply facilitates the match between you and the lender.

Do brokered loans usually have lower rates than going direct?

Brokered loans often carry lower rates because brokers access wholesale pricing from multiple lenders, though your final rate depends on your credit profile and current market conditions.

What fees should I expect with a brokered loan?

Expect broker compensation of 1 to 2% of your loan amount, which can be paid by you or the lender and must be fully disclosed before closing.

Is using a mortgage broker regulated for consumer protection?

Yes, broker fee disclosures are regulated by the CFPB, which requires clear documentation and protects consumers from hidden compensation arrangements.

Can I refinance with a brokered loan?

Absolutely. Mortgage brokers can shop wholesale refinance rates across multiple lenders, often finding better terms than a single bank can offer on a refinance.