TL;DR:

- A bridge loan is a short-term, secured financing option that allows homebuyers to purchase a new property before selling their current home. It typically lasts 6–12 months and uses the current home's equity as collateral, with repayment due once the existing home sells. While offering speed and flexibility, bridge loans are costly and carry risks like foreclosure if the home does not sell in time.

A bridge loan is defined as a short-term, secured financing option that lets you buy a new home before your current one sells. Typical terms run 6–12 months, though lenders may extend them up to three years. Think of it as a financial runway. You get the funds to close on your next property today, then repay the loan once your existing home sells. For buyers competing in fast-moving markets, this kind of temporary loan for real estate can be the difference between landing your dream home and watching it go to someone else.

What is a bridge loan and how does it work?

A bridge loan works by using your current home's equity as collateral to fund the purchase of a new one. The lender advances you capital based on the value of the property you already own. You use those funds to make a down payment or cover the full purchase price of your next home. Once your current home sells, the proceeds pay off the bridge loan balance.

The repayment structure varies by lender. Some lenders allow interest-only payments or deferred payments during the loan term, with the full principal due at the end. That final lump sum is called a balloon payment. It keeps your monthly obligations lower during the transition period, but it means you must sell your home before the loan matures.

Here is how the process typically unfolds:

- List your current home for sale. Most lenders require your property to be listed before they approve a bridge loan. This confirms you have a clear exit strategy.

- Apply for the bridge loan. The application mirrors a standard mortgage. Lenders review your credit, equity position, and debt-to-income ratio.

- Get approved and funded. Approval and funding can move quickly, sometimes within two weeks, which is far faster than a conventional mortgage timeline.

- Close on your new home. You use the bridge loan proceeds for the down payment or full purchase.

- Sell your current home. The sale proceeds repay the bridge loan balance, including any accrued interest.

Pro Tip: List your current home before you apply. Lenders treat an active listing as proof of your repayment plan. Without it, many lenders will decline the application outright.

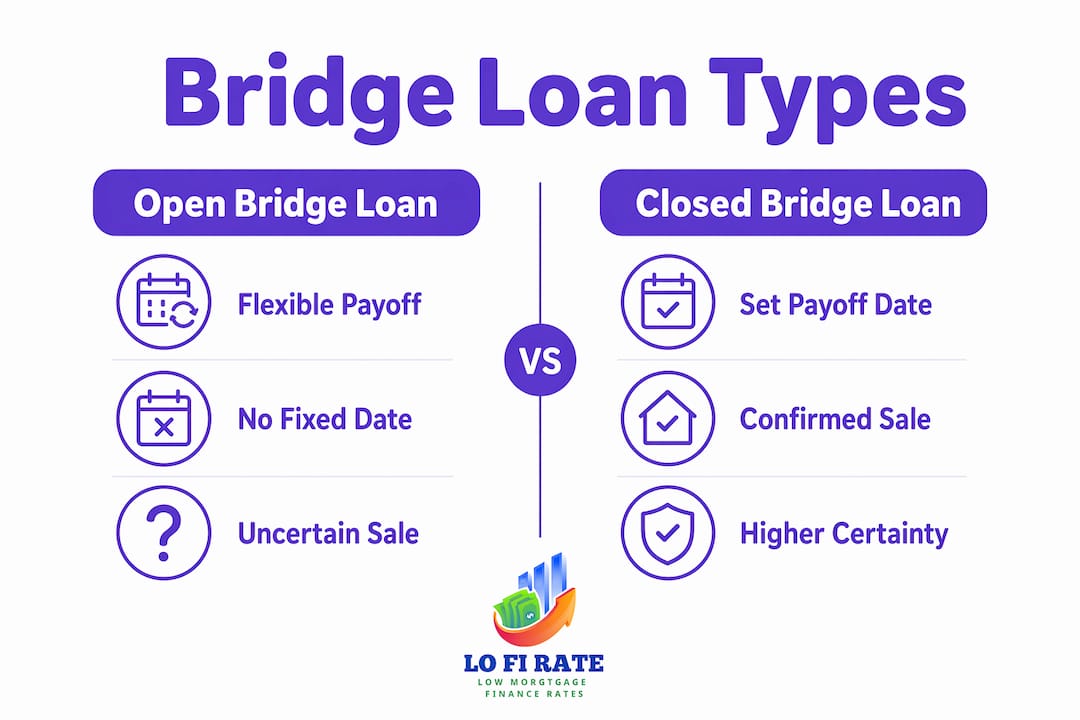

Open vs. closed bridge loans: which type fits you?

Not all bridge financing options are structured the same way. The two main categories are open and closed bridge loans, and the difference matters for your risk exposure.

Open bridge loans have no fixed payoff date, which gives you flexibility if your home takes longer to sell. That flexibility comes at a cost. Lenders charge higher rates on open loans because the repayment timeline is uncertain. If your home sits on the market for months, your interest costs climb with it.

Closed bridge loans carry a set payoff date tied directly to a confirmed sale date. Because the lender knows exactly when they will be repaid, the terms are more favorable. Closed loans are the lower-risk option for both parties.

| Feature | Open Bridge Loan | Closed Bridge Loan |

|---|---|---|

| Payoff date | Flexible, no fixed date | Fixed, tied to confirmed sale |

| Interest rate | Higher due to uncertainty | Lower, more predictable |

| Lender risk | Higher | Lower |

| Borrower risk | Higher if home sells slowly | Lower with confirmed sale date |

| Best for | Uncertain sale timelines | Buyers with a sale already in progress |

Most buyers in competitive markets prefer closed loans when they already have an offer accepted on their current home. Open loans make more sense when you need to move fast but have not yet secured a buyer.

What are the real costs and risks of bridge loans?

Bridge loans are significantly more expensive than conventional mortgages. Higher interest rates and fees are built into the product because lenders take on more risk with short-term, transitional financing. You are not just paying a higher rate. You are also paying origination fees, appraisal costs, and closing costs, all compressed into a loan that may only last six months. For a full breakdown of what those fees look like in practice, this bridge loan fee analysis from YieldStack covers current market costs in detail.

The risks go beyond the price tag. Here are the key downsides every borrower should understand:

- Foreclosure exposure. If your home does not sell before the loan matures, the lender can foreclose on the collateral property. This is the single biggest danger in bridge financing.

- Overlapping payments. You may carry a mortgage on your current home, a bridge loan payment, and a new mortgage simultaneously. You need sufficient cash reserves to manage all three without defaulting.

- Market timing risk. If your local real estate market slows, your home may not sell at the price or speed you expected. That gap can leave you stuck with a maturing loan and no proceeds to cover it.

- Credit impact. Taking on a bridge loan increases your total debt load. That can affect your debt-to-income ratio and complicate approval for your new mortgage if both loans are active at the same time.

"Bridge loans are a temporary lifeline, not a permanent mortgage. Treat them that way." — Experian

Pro Tip: Before you commit, calculate the total cost of the bridge loan including all fees and interest at the maximum term. Then ask yourself whether your home will realistically sell within that window. If the answer is uncertain, explore alternatives first.

How do bridge loans compare to other financing options?

Bridge loans are more expensive than alternatives, but they offer speed and flexibility that other products cannot match. Approval and funding can occur in as little as two weeks, which matters when you are competing against cash buyers or facing a tight closing deadline.

A home equity line of credit, or HELOC, is the most common alternative. A HELOC lets you borrow against your current home's equity at a lower interest rate. The catch is that approval takes longer and many lenders freeze or reduce HELOCs once a property goes on the market. That timing conflict makes HELOCs unreliable for buyers who need to move quickly.

A conventional mortgage on the new property is another path, but it typically requires you to qualify while still carrying your existing mortgage. That dual-debt burden disqualifies many buyers. For a deeper look at how conventional loans are structured, this conventional loan guide from Lofirate explains the qualification criteria clearly.

| Financing Option | Typical Interest Rate | Loan Term | Speed of Funding | Key Requirement |

|---|---|---|---|---|

| Bridge loan | Higher than conventional | 6 months to 3 years | As fast as 2 weeks | Home listed for sale, equity in current property |

| HELOC | Moderate, variable | Revolving credit line | 2–6 weeks | Stable equity, home not yet listed |

| Conventional mortgage | Lower, fixed or variable | 15–30 years | 30–45 days | Income, credit, and debt-to-income qualification |

| FHA loan | Low to moderate | 15–30 years | 30–45 days | Lower credit threshold, primary residence only |

Bridge loans enable quicker home purchases in competitive markets where waiting for a sale to close first means losing the property. That speed advantage is real, but it comes at a measurable cost. If you have time and equity, a HELOC or a contingency-based conventional loan is almost always cheaper. If you are in a fast market and need to act now, a bridge loan earns its premium. You can also explore non-traditional mortgage options that may fit your situation better depending on your financial profile.

Key takeaways

A bridge loan is a short-term financing tool that solves a specific timing problem, and it only makes financial sense when you have strong equity, a realistic sale timeline, and cash reserves to cover overlapping payments.

| Point | Details |

|---|---|

| Bridge loan definition | A short-term secured loan using your current home as collateral to fund a new purchase. |

| Typical loan term | Most bridge loans run 6–12 months, with a maximum of around 3 years. |

| Repayment structure | Payments are often interest-only or deferred, with a balloon payment due at term end. |

| Biggest risk | Foreclosure on your current home if it does not sell before the loan matures. |

| Best alternative | A HELOC offers lower rates but may not be available once your home is listed for sale. |

The honest truth about when bridge loans actually make sense

I have seen homeowners take out bridge loans for the wrong reasons, and it almost always comes down to impatience rather than strategy. A bridge loan is not a solution for a slow-selling market. It is a tool for buyers who have strong equity, a realistic sale timeline, and the cash reserves to carry two properties for several months without financial strain.

The mistake I see most often is underestimating how long a home sale actually takes. Buyers assume their current home will sell in 30 days because the market feels hot. Then it sits for 90 days, the bridge loan is approaching maturity, and suddenly they are negotiating a price reduction just to close before the deadline. That pressure costs money.

My honest recommendation is this: if you have a signed purchase agreement on your current home and just need a few weeks of overlap to close on the new one, a bridge loan is a clean, efficient solution. If you are hoping your home will sell quickly but have no confirmed buyer, the risk profile shifts considerably. In that case, talk to a licensed mortgage broker before you commit. A broker who shops multiple lenders can show you whether a bridge loan is truly your best option or whether a HELOC or a contingency offer gets you to the same place at a lower cost.

The buyers who use bridge loans well treat them like a short-term business decision. They know their exit date, they have the reserves, and they have already done the math on total cost. That discipline is what separates a smart bridge loan from a stressful one.

— LoFi

Ready to explore your loan options?

If you are weighing a bridge loan against other financing paths, the smartest first step is talking to a wholesale mortgage broker who can compare multiple lenders on your behalf.

Lofirate connects homebuyers with licensed wholesale mortgage brokers who shop across multiple lenders to find competitive rates. Unlike retail lenders who offer only their own products, wholesale brokers give you real options side by side. Whether you are looking at bridge financing, a conventional loan, or something in between, Lofirate makes it easy to get a no-obligation second opinion. Visit Lofirate's loan options page to see what financing solutions are available for your situation, or go directly to lofirate.com to get started.

FAQ

What is the bridge loan definition in simple terms?

A bridge loan is a short-term secured loan that lets you buy a new home before your current one sells, using your existing home's equity as collateral. Terms typically run 6–12 months.

How does a bridge loan work for a home purchase?

You borrow against your current home's equity to fund the down payment or purchase of a new property. Once your current home sells, the proceeds repay the bridge loan balance, including interest.

What are the main risks of bridge loans?

The primary risk is foreclosure. If your home does not sell before the loan matures, the lender can foreclose on the collateral property. Overlapping mortgage payments also strain cash flow during the transition period.

How do bridge loans compare to a HELOC?

Bridge loans fund faster, sometimes within two weeks, but carry higher interest rates and fees. A HELOC offers lower rates but is often unavailable once your home is listed for sale, making it less reliable for active buyers.

What credit score do you need for a bridge loan?

Most lenders require a credit score of at least 650–700, along with sufficient equity in your current home and an active listing. The application process mirrors a standard mortgage approval.