TL;DR:

- A loan estimate is a standardized three-page document provided within three business days that details proposed mortgage terms, estimated payments, and closing costs. It is an essential comparison tool that should be viewed as a starting point, not a final, binding offer, allowing borrowers to negotiate better terms. Comparing multiple estimates within a 10-day window helps borrowers secure more favorable mortgage rates and avoid costly surprises at closing.

A loan estimate is a standardized three-page form that every mortgage lender must give you within three business days of receiving your application. It spells out your proposed loan terms, estimated monthly payments, projected closing costs, and the total cash you will need at closing. Before you sign anything or pay any significant fees, this document is your clearest window into what a mortgage will actually cost you.

Most homebuyers glance at the interest rate and move on. That is a costly mistake. The loan estimate contains at least a dozen figures that directly affect your budget, your negotiating position, and your ability to compare competing lenders on equal footing. Understanding each section of this form is one of the most practical financial skills you can develop before buying a home.

What is a loan estimate and what does it include?

A loan estimate is issued under TILA-RESPA Integrated Disclosure rules, a federal framework designed to make mortgage disclosures uniform across every lender in the country. That standardization is the point. Whether you apply at a large bank, a credit union, or through a wholesale broker, the form looks identical, which makes side-by-side comparison straightforward.

The core figures on page one

Page one of the form carries the most critical numbers. You will find the loan amount, the interest rate, the annual percentage rate (APR), and your projected monthly payment, which includes principal, interest, estimated property taxes, homeowner's insurance, and mortgage insurance if applicable. The APR is always higher than the interest rate because it folds in lender fees, giving you a truer picture of annual borrowing cost.

Closing costs and cash to close

Page two breaks down every fee attached to the loan. These fall into three categories: fees that cannot change at closing, fees that can increase by up to 10%, and fees that can change without limit. Knowing which category each fee belongs to tells you exactly where a lender has flexibility and where you can push back.

Page three contains the Estimated Cash to Close, which is the single most underused figure on the entire document. It calculates your down payment plus closing costs, then subtracts any deposits you have already paid and any seller credits you have negotiated, and adds other adjustments. Focusing only on the monthly payment while ignoring this number is how buyers arrive at the closing table short on funds.

Pro Tip: Ask your lender to walk you through the "Services You Can Shop For" section on page two. These are third-party fees, such as title insurance and settlement services, where you have the legal right to choose your own provider and potentially save hundreds of dollars.

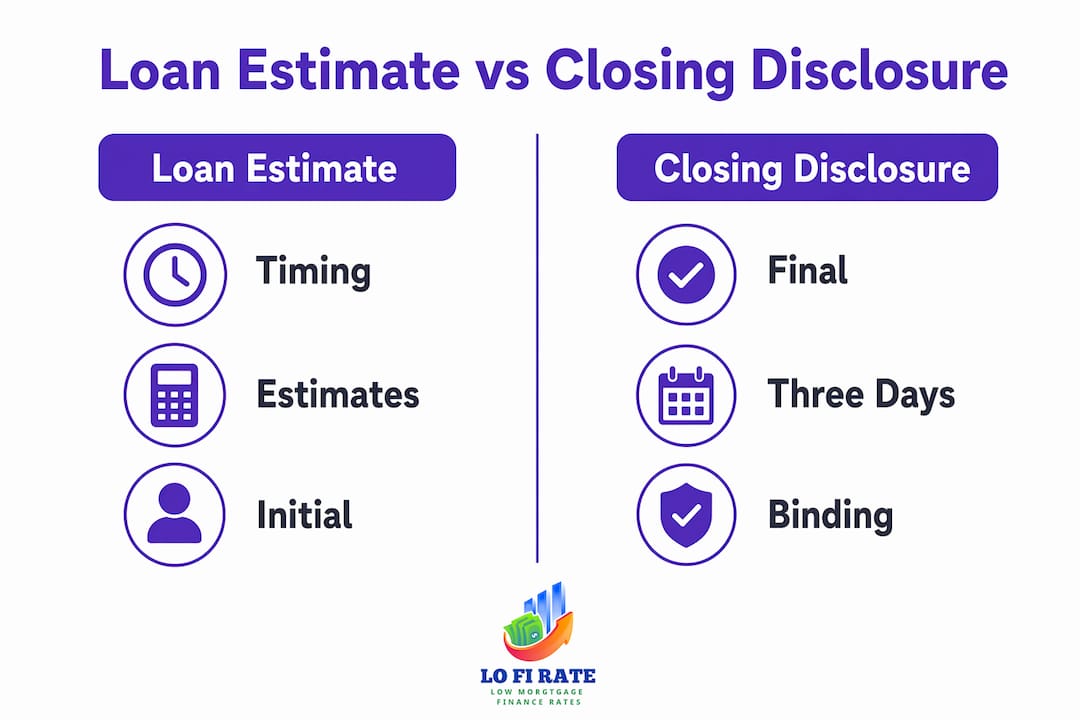

How does a loan estimate differ from the Closing Disclosure?

The loan estimate and the Closing Disclosure serve different purposes at different stages of the mortgage process. Confusing the two leads borrowers to make decisions based on the wrong document at the wrong time.

The Closing Disclosure arrives at least three business days before your scheduled closing date. It reflects the final, locked terms of your loan. By that point, most of the negotiating is over. The loan estimate, by contrast, arrives early in the process and represents proposed terms that can still change.

| Feature | Loan Estimate | Closing Disclosure |

|---|---|---|

| When you receive it | Within 3 business days of application | At least 3 business days before closing |

| Purpose | Compare lenders and plan your budget | Confirm final loan terms before signing |

| Binding on lender | No, figures can change | Yes, reflects locked final terms |

| Best use | Shopping and negotiating | Verifying no surprises at closing |

Revised loan estimates can also appear during the process. Under federal rules, changes in interest rate locks or significant changes to your loan terms can trigger a new version. When you receive a revised estimate, compare it line by line against the original. Any unexplained increase in fees deserves a direct question to your lender before you proceed.

The CFPB advises borrowers to treat the loan estimate as a review document, not final paperwork. That framing matters. Every number on it is an invitation to ask questions, not a figure to accept passively.

Why comparing multiple loan estimates saves you real money

Requesting a single loan estimate and accepting it is the mortgage equivalent of buying the first car you test drive. Freddie Mac recommends requesting multiple estimates from different lenders to compare within the 10-business-day validity window. That window exists precisely to encourage shopping.

The mechanics of effective comparison require discipline. Here is how to do it correctly:

- Apply to at least three lenders on the same day or within a two-day window. Loan estimates reflect market conditions at the time of application. A rate environment that shifts between Monday and Friday can make two estimates look different even when the lenders are equally competitive.

- Request the same loan parameters from every lender. Same loan amount, same loan type (30-year fixed, 15-year fixed, or adjustable), same down payment percentage. Freddie Mac notes that comparing identical loan parameters is the only way to avoid misleading apples-to-oranges results.

- Compare the APR, not just the interest rate. A lender offering a slightly lower rate but charging two points in origination fees may cost you more over five years than a lender with a slightly higher rate and minimal fees.

- Add up Section A fees on page two. Section A, labeled "Origination Charges," is where lenders have the most direct control over their pricing. A lower rate paired with high origination charges is a trade-off, not a discount.

- Check the Estimated Cash to Close on every estimate. Two lenders may quote nearly identical monthly payments while requiring very different amounts of cash upfront. That gap can be thousands of dollars.

Pro Tip: Multiple mortgage applications within a 45-day window are treated as a single credit inquiry by FICO scoring models. Shopping aggressively will not damage your credit score.

Comparing offers side by side is one of the most direct ways to save thousands on your mortgage. Borrowers who collect three or more estimates consistently secure better terms than those who accept the first offer. The loan estimate form exists specifically to make that comparison possible.

Common mistakes borrowers make with loan estimates

Understanding what a loan estimate is only gets you halfway. Knowing where borrowers go wrong with it gets you the rest of the way.

- Treating it as a binding approval. A loan estimate is not a commitment to lend. It is a proposed set of terms and costs that can change based on appraisal results, underwriting findings, or rate fluctuations. Never cancel a competing application because you received one estimate you liked.

- Ignoring the expiration date. Loan estimates are valid for 10 business days from the issue date. If you wait too long to respond, the lender can revise the terms. Track the date on every estimate you receive.

- Focusing only on the monthly payment. Monthly payment is one data point. The Estimated Cash to Close, the total interest paid over the loan term, and the breakeven point on any discount points paid are equally important figures. A real estate attorney or HUD-approved housing counselor can help you interpret these numbers if the math feels overwhelming.

- Not asking about discrepancies. If a fee on your loan estimate looks higher than what a lender quoted verbally, ask for a written explanation. Lenders are required to honor certain fee categories within defined tolerances.

- Skipping the comparison entirely. Many first-time buyers apply to one lender, receive one estimate, and proceed. This forfeits the negotiating leverage that comparing mortgage offers provides. Even a 0.25% rate difference on a $400,000 loan adds up to tens of thousands of dollars over 30 years.

Understanding the difference between a loan estimate and a Closing Disclosure also prevents last-minute surprises at the closing table. Review both documents carefully and flag any fees that appear on the Closing Disclosure but were absent from your original estimate.

Key takeaways

A loan estimate is your primary tool for understanding, comparing, and negotiating mortgage costs before you commit to any lender.

| Point | Details |

|---|---|

| Definition and timing | A standardized three-page form delivered within 3 business days of your mortgage application. |

| Cash to Close is critical | This figure bundles down payment, closing costs, and adjustments. Never ignore it in favor of monthly payment alone. |

| Not a binding offer | Terms can change. Treat every estimate as a starting point for questions and comparison, not a final approval. |

| Shop within 10 days | Loan estimates expire after 10 business days. Request multiple estimates simultaneously for accurate comparison. |

| APR beats interest rate | APR includes lender fees and gives a truer cost of borrowing than the interest rate alone. |

Why most borrowers leave money on the table with loan estimates

Most borrowers I have seen go through the mortgage process treat the loan estimate like a receipt. They look at the total, nod, and file it away. That approach costs real money.

The form is actually a negotiating document. When you bring a competing loan estimate to a lender and ask them to match or beat a specific line item, you are using the tool exactly as it was designed. Lenders expect this. Many will adjust origination fees or offer a rate match rather than lose your business.

The figure I always tell borrowers to focus on first is the Estimated Cash to Close, not the monthly payment. Monthly payments feel manageable in the abstract. Cash to Close is the number that determines whether you can actually get to the closing table. I have seen buyers fall in love with a low monthly payment quote, only to discover they were $8,000 short on closing day because they never read page three.

Timing also matters more than most people realize. Applying to multiple lenders on the same day is not aggressive. It is the standard practice that financially savvy buyers use to create real competition for their business. The 45-day credit inquiry window from FICO removes the only excuse most borrowers give for not shopping around. Use it.

The closing costs breakdown on page two also deserves more attention than it typically gets. Third-party fees in the "Services You Can Shop For" section are negotiable by definition. Most buyers accept the lender's preferred vendors without question. That is a missed opportunity on every single transaction.

— LoFi

Get multiple loan estimates through Lofirate

Lofirate connects homebuyers and homeowners with licensed wholesale mortgage brokers who shop multiple lenders on your behalf. Instead of applying to one retail bank and accepting their pricing, you get access to a broader set of rate options through a single, no-obligation consultation. Wholesale brokers have access to lender pricing that is not available at the retail counter, which means the loan estimates you receive through this channel often reflect more competitive terms. If you are ready to compare real numbers and make a confident financing decision, explore your loan options or connect with a broker through Lofirate today.

FAQ

What is a loan estimate in a mortgage?

A loan estimate is a standardized three-page document that lenders must provide within three business days of your mortgage application. It outlines your proposed loan terms, estimated monthly payments, closing costs, and total cash needed to close.

How long is a loan estimate valid?

Loan estimates are valid for 10 business days from the date they are issued. After that window closes, the lender can revise the terms, so respond or request competing estimates within that period.

Is a loan estimate a binding commitment from the lender?

No. A loan estimate is a proposed set of terms, not a final approval or a binding offer. Terms can change based on appraisal results, underwriting decisions, or rate movements before closing.

How does a loan estimate differ from a Closing Disclosure?

The loan estimate arrives early in the process and reflects estimated terms. The Closing Disclosure arrives at least three business days before closing and reflects the final, locked terms of your loan.

How many loan estimates should I request?

Request at least three estimates from different lenders using identical loan parameters. Applying within the same short window and following a mortgage shopping checklist gives you the most accurate comparison and the strongest negotiating position.