TL;DR:

- The GFE is a federal disclosure form that estimated mortgage settlement costs before 2015 and remains used for reverse mortgages today. It was replaced by the Loan Estimate in 2015 to simplify disclosures and strengthen fee protections under TRID rules. Borrowers should carefully compare GFEs and Loan Estimates as tools to negotiate better loan terms and avoid unexpected costs.

If you have ever heard a lender toss out the term "GFE" and felt a wave of confusion, you are not alone. What is GFE in mortgages, exactly? The Good Faith Estimate was a standardized disclosure form required under federal law that gave borrowers an early look at their expected loan costs before closing. While it has largely been replaced by a newer form for most loans today, understanding the GFE still matters, especially if you are taking out a reverse mortgage or trying to make sense of mortgage cost disclosures in general.

Table of Contents

- Key Takeaways

- What is GFE in mortgages: definition and regulation

- GFE vs. Loan Estimate: what changed in 2015

- What the GFE form actually showed borrowers

- When you might still receive a GFE in 2026

- How to read and use a GFE effectively

- My take on mortgage disclosures and what they actually teach you

- See what wholesale mortgage pricing looks like for your loan

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| GFE is a cost disclosure form | The Good Faith Estimate showed borrowers estimated settlement charges and key loan terms before closing. |

| Replaced for most loans in 2015 | The Loan Estimate took over for conventional mortgages under the TRID rule starting October 2015. |

| Still used for reverse mortgages | Borrowers applying for Home Equity Conversion Mortgages still receive a GFE instead of a Loan Estimate. |

| Terms held for 10 business days | Lenders were required to keep most GFE estimates firm for at least 10 business days after delivery. |

| Use it to comparison shop | A GFE gives you a side-by-side framework to compare loan offers from multiple lenders before committing. |

What is GFE in mortgages: definition and regulation

The GFE definition in mortgages starts with the Real Estate Settlement Procedures Act, better known as RESPA. Under RESPA, lenders were required to hand borrowers a standardized document that laid out the estimated costs of closing a mortgage loan. The GFE provides estimates of settlement charges as dollar amounts, along with key loan details, on a government-prescribed form with specific instructions for completion.

The good faith estimate meaning goes beyond just a list of numbers. It was designed as an apples-to-apples starting point for borrowers to compare offers from competing lenders before making any commitment. The RESPA disclosure goal was to reduce information asymmetry between lenders and borrowers and make closing costs more predictable.

On timing, the rules were specific. Lenders had to deliver the GFE within 3 business days of receiving a complete loan application. If sent by mail, it was considered received three calendar days after mailing, excluding Sundays and federal holidays.

Here is a quick look at what the GFE typically covered:

- Origination charges: Fees the lender charged for processing and underwriting your loan

- Title services and insurance: Costs for the title search, title insurance, and settlement agent fees

- Appraisal and inspection fees: Third-party charges to assess the property's value

- Government recording fees: State and local charges to officially record the property transfer

- Transfer taxes: Taxes on the transfer of ownership from seller to buyer

- Escrow prepaids: Upfront deposits for homeowner's insurance and property taxes

- Per diem interest: The daily interest charge from your closing date to the end of the month

Pro Tip: Before signing anything, request GFEs from at least two or three lenders on the same day. Since lenders must keep most estimates firm for a set period, you will have a real comparison rather than shifting numbers.

One important borrower protection in the original rules: lenders could not charge fees for appraisals or inspections before delivering the GFE and getting your written intent to proceed. Only a credit report fee could be collected before that point.

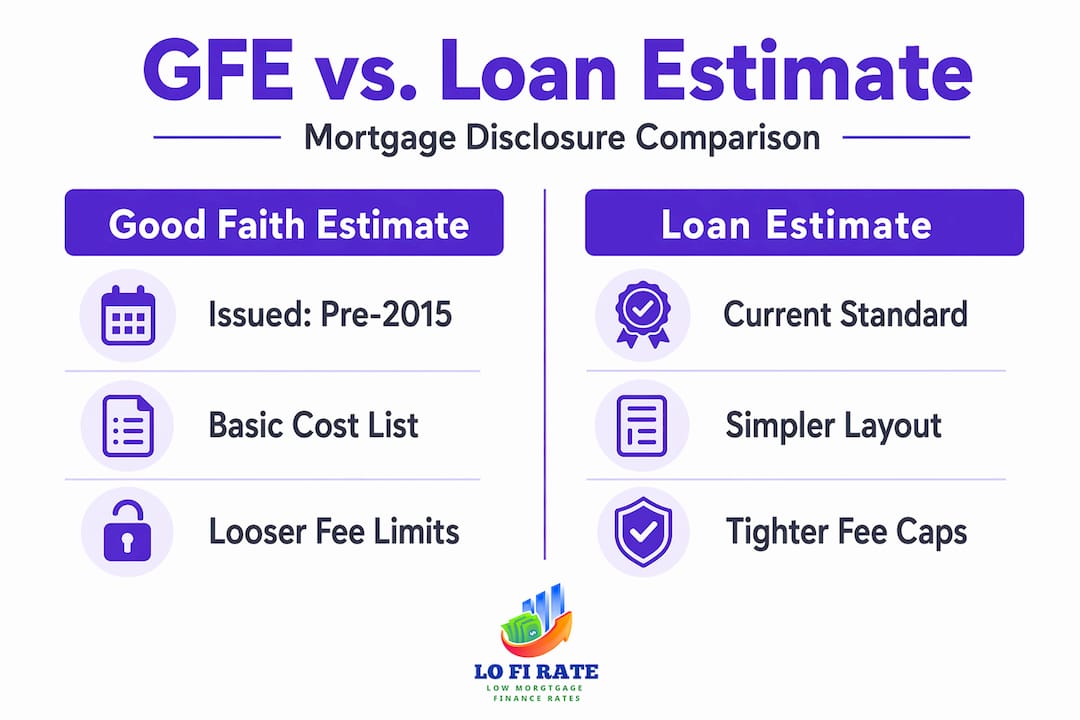

GFE vs. Loan Estimate: what changed in 2015

Understanding GFE in loans also means knowing why it was updated. Before October 2015, borrowers were handed multiple overlapping disclosure forms at different stages of the mortgage process. One came from RESPA, another from the Truth in Lending Act. They used different terminology, different formats, and different timing rules. Borrowers regularly showed up at closing surprised by fees they had not fully understood.

The TRID rule in 2015 changed that by folding the GFE and the initial Truth-in-Lending disclosure into a single three-page Loan Estimate form. The goal was simpler paperwork and clearer cost projections.

Here is how the two forms compare:

| Feature | Good Faith Estimate (GFE) | Loan Estimate |

|---|---|---|

| Effective period | Pre-October 2015 | October 2015 to present |

| Applies to | Most mortgage loans (RESPA-covered) | Most closed-end residential mortgages |

| Does NOT apply to | Reverse mortgages, HELOCs | Reverse mortgages, HELOCs, some business loans |

| Fee tolerance rules | Moderate protections with categories | Stronger caps with tiered buckets |

| Timing of delivery | Within 3 business days of application | Within 3 business days of application |

| Combined disclosures | Separate from Truth-in-Lending form | Merges initial TIL and GFE into one form |

| Terms availability window | 10 business days | 10 business days |

The biggest upgrade in the Loan Estimate was its fee tolerance structure. The Loan Estimate limits fee increases by sorting them into buckets, with some fees capped at zero tolerance for change and others allowed only a 10% cumulative increase. This gave borrowers significantly stronger protection against last-minute cost inflation at the closing table.

The transition to the Loan Estimate also improved the borrower experience by simplifying the language and layout. Instead of decoding two separate government forms, you now get one document with consistent terminology from application to closing.

What the GFE form actually showed borrowers

The mortgage good faith estimate process was built around giving you a full picture of your loan before you committed to anything. The form was broken into numbered sections, each covering a distinct cost category.

Beyond the fee categories listed earlier, the GFE also showed your expected loan terms up front. That included the initial loan amount, the interest rate, whether the rate was fixed or adjustable, whether there was a prepayment penalty, and the estimated monthly payment. If your rate could change over time, the GFE disclosed the maximum possible payment as well.

One nuance worth knowing: GFE terms had to remain available for at least 10 business days from the date provided. However, that 10-day rule had a carved-out exception. It did not apply to the interest rate, rate-dependent charges, adjusted origination charges, or per diem interest. Those items were tied to market conditions and could shift with rate fluctuations. Understanding which charges were exempt from the availability window is critical for interpreting your rate lock nuances correctly.

If your lender needed to issue a revised GFE after the initial one, they were required to document the reason. And those records had to be kept for at least 3 years after settlement to support compliance audits.

Pro Tip: When reviewing a GFE or Loan Estimate, check the closing cost categories carefully. Some fees are set by the lender and negotiable; others, like government recording fees, are fixed. Knowing the difference helps you focus your negotiating energy where it actually counts.

When you might still receive a GFE in 2026

Most homebuyers today will receive a Loan Estimate rather than a GFE. But there is one significant exception. Reverse mortgages are exempt from TRID, which means borrowers applying for a Home Equity Conversion Mortgage (HECM) still receive the original GFE form. The same applies to certain other loan types that fall outside the TRID framework.

Situations where you might still see a GFE include:

- Reverse mortgages (HECMs): The most common scenario in 2026 where a GFE is still issued

- Home equity lines of credit (HELOCs): These are also exempt from TRID and use legacy disclosures

- Certain business-purpose loans: Some loans secured by residential property but made for business use may fall outside TRID requirements

- Loans from smaller or non-covered lenders: Specific institutional types may not be subject to standard TRID rules

Legacy GFE rules remain legally in force for these loan types. If you are a senior exploring a reverse mortgage to tap your home equity, you will go through the GFE process rather than receiving a Loan Estimate. The same core protections apply: the lender must deliver the form on time, cannot charge fees before you receive it (except for a credit report), and must keep the estimates available for the required period.

Knowing this distinction matters. If a lender hands you a GFE and you were expecting a Loan Estimate, that is not necessarily a red flag. It may simply mean your loan type falls outside TRID coverage. Ask your lender directly which form applies to your loan and why.

How to read and use a GFE effectively

Reading a GFE is not complicated once you know what to look for. Here is a practical approach to getting the most out of it:

- Match every fee to a category. The GFE breaks costs into specific blocks. If you see a fee that does not fit neatly into any labeled section, ask your lender to explain it in writing.

- Check the interest rate section separately. Since rate-dependent items are not bound by the 10-day availability window, make sure you understand whether your rate is locked and for how long.

- Compare multiple GFEs on the same day. Request GFEs from different lenders simultaneously. Because the form is standardized, you can do a direct line-by-line comparison without translating between different formats.

- Flag any unexplained changes. If a lender provides a revised GFE, they are required to document the reason. Ask for that documentation if it is not offered.

- Use it with your other documents. The GFE works best alongside your mortgage shopping checklist and any follow-up disclosures to build a complete picture of your total loan cost.

Pro Tip: If you receive a GFE and the fees look dramatically lower than a competitor's, dig deeper before celebrating. Lenders sometimes underestimate third-party costs early on, knowing they can revise the GFE later. A suspiciously low estimate is a reason to ask questions, not sign faster.

The mortgage compliance framework behind the GFE was designed specifically to protect you from being blindsided at the closing table. Use every disclosure you receive as a tool for negotiation and verification, not just paperwork to file away.

My take on mortgage disclosures and what they actually teach you

I have watched the mortgage disclosure process evolve for years, and here is what I have learned: most borrowers treat the GFE and Loan Estimate as bureaucratic formalities rather than negotiating tools. That is a costly mistake.

When the GFE was the standard form, it represented a genuine leap forward in consumer protection. Before RESPA standardized the disclosure process, borrowers had almost no way to compare loan offers on equal footing. Lenders quoted fees in wildly different formats, and surprise charges at closing were routine. The GFE changed that dynamic by forcing transparency onto a standard template.

But I have also seen the GFE's limits firsthand. The fee tolerances under the original GFE rules were looser than what we have today. A lender could revise several cost categories upward without much penalty, and borrowers who did not know to push back often paid more than they should have. The move to the Loan Estimate tightened those protections substantially.

What I keep coming back to is this: the form does not protect you. You protect yourself by actually reading it, comparing it line by line with competing offers, and asking specific questions when numbers seem off. I have seen borrowers save thousands simply by pointing to a fee on a disclosure and asking "can this be reduced?" Most of the time, the answer surprised them.

Whether you receive a GFE for a reverse mortgage or a Loan Estimate for a purchase loan, treat it as a starting point for a conversation, not a final answer.

— LoFi

See what wholesale mortgage pricing looks like for your loan

Most borrowers only ever see what a single retail lender is willing to quote them. That is a bit like buying a car without checking what any other dealer charges. At Lofirate, we connect you with licensed wholesale mortgage brokers who shop multiple lenders to find competitive pricing, so you are not locked into one lender's margin.

Understanding disclosures like the GFE and Loan Estimate is step one. Step two is knowing whether the rates and fees you are being quoted are actually competitive. Through Lofirate's broker matching services, you get a no-obligation consultation with a licensed broker in your state who can show you what wholesale pricing looks like compared to what you might find at a retail bank. There is no cost to connect and no pressure to proceed.

FAQ

What is a GFE in mortgage terms?

A GFE, or Good Faith Estimate, is a standardized form lenders were required to provide under RESPA that estimated a borrower's closing costs and key loan terms. It gave buyers an early, comparable snapshot of expected settlement charges before committing to a loan.

Is the GFE still used today?

The GFE was replaced by the Loan Estimate for most residential mortgages in October 2015 under the TRID rule. It is still used for reverse mortgages and certain other loan types exempt from TRID, such as HELOCs.

How long does a lender have to deliver a GFE?

Lenders must deliver a GFE within 3 business days of receiving a complete mortgage application. If mailed, it is considered received 3 calendar days after being sent, excluding Sundays and legal public holidays.

What is the difference between a GFE and a Loan Estimate?

Both disclose estimated mortgage costs early in the loan process, but the Loan Estimate combines multiple disclosures into one form and offers stronger fee protection rules with specific tolerance caps. The GFE applied to pre-2015 loans and still applies to reverse mortgages today.

Can fees change after a lender provides a GFE?

Some fees are fixed or capped under GFE rules, while others can change within defined limits. Lenders must document and retain records of any revised GFE for at least 3 years after settlement, providing a paper trail if changes occur.