TL;DR:

- The loan-to-value ratio measures your mortgage amount relative to your property's appraised value and influences your loan approval, interest rate, and insurance costs. Understanding how to calculate LTV, the limits set by different loan programs, and its impact on costs and insurance helps borrowers make informed decisions. Monitoring and managing your LTV throughout homeownership can lead to savings through canceled mortgage insurance and better loan options.

The loan-to-value ratio is defined as your mortgage amount divided by your property's appraised value, expressed as a percentage. Lenders use this number to measure risk before approving your loan. A $360,000 mortgage on a $400,000 home produces a 90% LTV. That single figure shapes your interest rate, your insurance costs, and whether you qualify at all. Understanding it before you apply puts you in a stronger position at every step of the home buying process.

How do you calculate the loan-to-value ratio?

The formula is straightforward: divide your loan amount by the appraised property value, then multiply by 100. The Consumer Financial Protection Bureau (CFPB) and the National Association of Realtors (NAR) both use this same standard calculation.

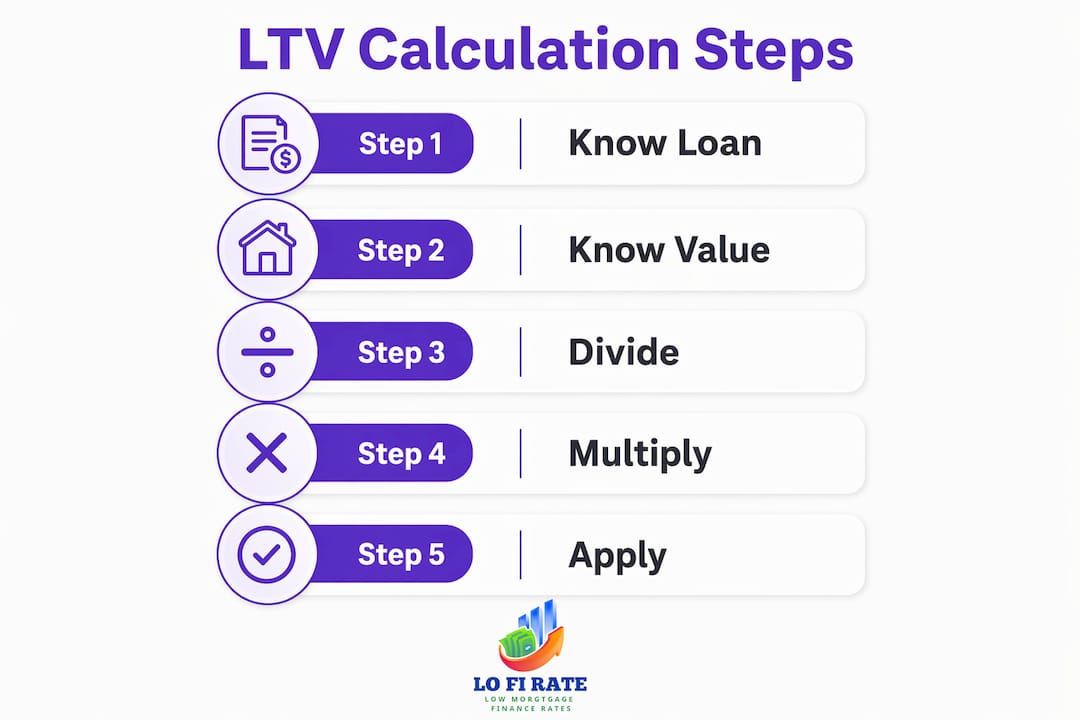

Here is how to work through it step by step:

- Get the appraised value. Your lender orders a professional appraisal. This number, not the listing price, is what lenders use.

- Confirm your loan amount. This is the amount you plan to borrow, not the purchase price.

- Divide and multiply. Loan amount ÷ Appraised value × 100 = LTV%.

- Interpret the result. An LTV below 80% is considered low risk. Above 80% typically triggers added costs.

Two quick examples show how the math plays out in real life. On a $500,000 home with a $400,000 loan, your LTV is 80%. On that same home with a $475,000 loan, your LTV jumps to 95%. That 15-point difference changes your insurance requirements and likely your interest rate.

One detail many buyers miss: appraisal differences from purchase price affect your actual LTV and the cash you need to close. If you agree to pay $420,000 for a home but it appraises at $400,000, your lender calculates LTV on $400,000. You either cover the gap out of pocket or renegotiate the price.

Pro Tip: Always request a copy of your appraisal report before closing. Verify the comparable sales used to set your home's value. A low appraisal can raise your LTV unexpectedly and change your loan terms.

LTV limits by mortgage type: what borrowers need to know

Different loan programs set different LTV ceilings. Knowing where each program draws the line tells you how much you need to put down and what insurance you might face.

| Loan Program | Maximum LTV | Mortgage Insurance Required? |

|---|---|---|

| Conventional | 97% | Yes, if LTV > 80% |

| FHA | 96.5% | Yes, always |

| VA | 100% | No (funding fee applies) |

| USDA | 100% | Yes (guarantee fee) |

| Jumbo | 80–90% | Varies by lender |

Conventional loans allow up to 97% LTV, while FHA loans cap at 96.5%. VA and USDA loans permit 100% financing, which means no down payment required. That sounds attractive, but both programs carry their own fees that function similarly to insurance.

The table above shows that a higher LTV ceiling does not automatically mean a cheaper loan. FHA loans require mortgage insurance for the entire loan term in most cases, regardless of how much equity you build. Conventional loans, by contrast, allow you to cancel private mortgage insurance once your LTV falls below 80%. For many buyers, that distinction makes a conventional loan the better long-term choice even if the FHA limit sounds more flexible.

Jumbo loans, which exceed conforming loan limits set by the Federal Housing Finance Agency (FHFA), typically require LTV ratios of 80–90% or lower. Lenders tighten standards on larger balances because the risk exposure is greater.

How does LTV affect your mortgage costs and insurance?

Your LTV ratio directly determines two major cost categories: your interest rate and your mortgage insurance requirement. Both can add thousands of dollars over the life of your loan.

Here is what a high LTV triggers in practice:

- Private mortgage insurance (PMI). Borrowers with LTV above 80% typically pay PMI, which adds to both upfront and monthly costs. PMI rates generally range from 0.5% to 1.5% of the loan amount annually.

- Higher interest rates. Lenders price loans based on risk. A 95% LTV signals more risk than a 75% LTV, so the rate offered is usually higher.

- Reduced negotiating power. Sellers and lenders both view a large down payment as a sign of financial stability. A low LTV strengthens your offer.

The good news: PMI cancellation is possible once your LTV drops below 80%, either through regular principal payments or rising home values. Removing PMI can save hundreds of dollars per month. You typically need to request cancellation in writing and may need a new appraisal to confirm your current LTV.

Lenders also use LTV to price loans dynamically. As you pay down your balance or your home appreciates, your LTV improves. That improvement can open the door to a refinance at a better rate. Monitoring your LTV over time is not just useful at purchase. It is a tool you can use throughout homeownership.

Pro Tip: Do not drain your savings to hit 80% LTV if it leaves you with no emergency fund. A slightly higher LTV with PMI is often more manageable than a financial crisis after closing. The best LTV balances down payment size with keeping cash reserves intact.

What nuances should you know about LTV in real estate financing?

LTV is one number, but the full picture of your mortgage risk involves several related concepts that lenders examine closely.

Combined loan-to-value (CLTV) explained

When you have more than one loan against a property, lenders calculate the combined loan-to-value ratio, or CLTV. The formula adds all loan balances together, then divides by the appraised value. A first mortgage of $300,000 plus a home equity line of credit (HELOC) of $50,000 on a $400,000 home produces a CLTV of 87.5%. That number matters when you apply for a second mortgage or refinance.

| Scenario | First Mortgage | Second Loan | Appraised Value | CLTV |

|---|---|---|---|---|

| Purchase only | $320,000 | None | $400,000 | 80% |

| With HELOC | $320,000 | $40,000 | $400,000 | 90% |

| After appreciation | $300,000 | $40,000 | $450,000 | 75.6% |

The CLTV table above shows how a rising home value can improve your combined ratio even without making extra payments. That is why tracking your property's market value matters beyond the day you close.

LTV is one factor, not the whole story

Lenders evaluate LTV alongside credit scores and debt-to-income ratios when reviewing your application. A strong LTV does not guarantee approval if your credit score is below the program minimum or your monthly debts consume too much of your income. Mortgage underwriting is a complete financial picture, not a single metric.

Negative equity is the scenario where your LTV exceeds 100%. This happens when property values fall after purchase. A homeowner who bought at peak pricing with a small down payment can find themselves owing more than the home is worth. During the 2008 housing crisis, millions of American homeowners experienced this. It limits your ability to sell, refinance, or access equity until values recover.

Poor credit scores or high debt-to-income ratios can override an otherwise favorable LTV. Lenders look at the complete application. Knowing your LTV is a strong starting point, but it works best when paired with a solid credit profile and manageable monthly obligations. Check your mortgage qualification steps before you assume a good LTV alone will carry your application.

Key takeaways

The loan-to-value ratio is the single most direct measure of mortgage risk, and understanding it gives you real leverage when negotiating rates, choosing loan programs, and planning your down payment.

| Point | Details |

|---|---|

| LTV formula | Divide your loan amount by the appraised value, then multiply by 100. |

| 80% threshold | Staying at or below 80% LTV avoids PMI and typically secures better rates. |

| Loan program limits | Conventional allows 97%, FHA 96.5%, and VA or USDA up to 100% LTV. |

| CLTV matters too | Multiple loans are combined to calculate total exposure against your property value. |

| PMI cancellation | Request PMI removal in writing once your LTV drops below 80% through payments or appreciation. |

Why i think most buyers focus on LTV the wrong way

Most homebuyers treat 80% LTV like a finish line. Get there and you win. That framing misses the point entirely.

I have seen buyers stretch every dollar to hit 80% down, only to close with no cash buffer for repairs, moving costs, or a job disruption. PMI on a $400,000 loan might cost $150–$200 per month. That is real money, but it is not a financial emergency. Wiping out your savings to avoid it can be.

The smarter approach is to treat LTV as a dial, not a switch. A 90% LTV with a strong credit score and six months of reserves is a healthier financial position than an 80% LTV with nothing left in the bank. Lenders know this too. That is why they look at the full picture.

What I find most underused is the post-purchase LTV check. Most homeowners never look at their LTV again after closing. But if your home appreciates significantly, you may already be below 80% without making a single extra payment. That means you can request PMI cancellation and redirect that money toward your principal or savings. A quick appraisal can pay for itself many times over.

Watch out for appraisal gaps on the buy side and CLTV surprises if you ever open a HELOC. Both can shift your numbers in ways that catch buyers off guard. When in doubt, talk to a licensed mortgage broker who can model the scenarios specific to your situation.

— LoFi

Put your LTV knowledge to work with Lofirate

Understanding your LTV ratio is the foundation. Finding a loan that rewards it is the next step.

Lofirate connects you with licensed wholesale mortgage brokers who shop multiple lenders to find rates that match your LTV profile. Retail lenders offer one price. Wholesale brokers compare many. That difference can mean a lower rate, reduced insurance costs, or a loan program better suited to your down payment size. Whether you are buying your first home or refinancing to remove PMI, Lofirate makes it easy to get a second opinion with no obligation. Explore your loan options at Lofirate or visit Lofirate's main platform to connect with a broker in your state today.

FAQ

What is the loan-to-value ratio in simple terms?

The loan-to-value ratio is your mortgage amount divided by your home's appraised value, expressed as a percentage. A $320,000 loan on a $400,000 home equals an 80% LTV.

What LTV ratio do lenders prefer?

Most lenders prefer an LTV of 80% or lower. At that threshold, you avoid private mortgage insurance and typically qualify for better interest rates.

Does a higher down payment always lower your LTV?

Yes. A larger down payment reduces the loan amount relative to the property value, which directly lowers your LTV and reduces lender risk.

Can your LTV change after you buy the home?

Your LTV changes as you pay down your principal or as your home's market value shifts. Rising home values can push your LTV below 80%, making you eligible to cancel PMI.

What is the difference between LTV and CLTV?

LTV measures one loan against your property value. CLTV adds all loans, including a first mortgage and any home equity line of credit, then divides by the appraised value to show total debt exposure.