TL;DR:

- Title insurance protects property owners and lenders from financial losses due to ownership defects hidden in public records. It involves a thorough search process before closing and provides ongoing legal defense and financial coverage for as long as ownership continues. Buyers can shop for providers, and an owner's policy is essential for comprehensive protection, especially in higher-risk transactions.

Title insurance is defined as a policy that protects property owners and mortgage lenders from financial loss caused by defects in a property's ownership history. Unlike car or health insurance, which guard against future events, title insurance covers problems that already existed before you bought the property but were not discovered until later. You pay a one-time premium at closing, and that coverage lasts for as long as you or your heirs hold an interest in the property. For homebuyers and real estate investors, understanding what title insurance covers is one of the most practical steps toward protecting a major financial asset.

What is title insurance and why does it matter?

Title insurance is the industry's standard term for a policy that defends your legal right to own a property. The National Association of Realtors classifies it as protection against losses from title problems that a title search may miss at closing. That distinction matters because no title search, however thorough, can guarantee that every historical defect has been found.

The core value of title insurance sits in two places. First, it funds the legal defense if someone challenges your ownership. Second, it pays out settlements or losses if a covered defect is proven. Without it, you would pay those costs out of pocket, which can run into tens of thousands of dollars in a contested case.

Title insurance also differs sharply from homeowners insurance. Homeowners insurance covers physical damage to your property, such as fire, theft, or storm damage. Title insurance covers legal and financial claims tied to the property's ownership history. You need both, and they serve entirely different purposes.

Pro Tip: Ask your closing agent to show you the commitment letter before closing day. It lists every known defect the title company found and plans to resolve before issuing your policy.

How does title insurance work before and after closing?

The process behind title insurance starts long before you sign any documents. Title companies complete about 135 thorough steps before closing to verify clear property ownership and correct any issues found. That number reflects the real scope of the work involved.

Those steps include:

- Searching public records going back decades, sometimes centuries, to trace ownership.

- Identifying unpaid liens, judgments, or tax obligations attached to the property.

- Verifying that all prior deeds were properly signed and recorded.

- Confirming that no boundary disputes or easement conflicts exist.

- Correcting or "curing" any defects found before the policy is issued.

After that curative work is done, the underwriter issues the policy. The underwriter then stands behind the search and guarantees legal defense and financial coverage if an undiscovered defect surfaces later. This is the key distinction between title insurance and a simple title search. A title search alone gives you information. Title insurance gives you a financial backstop if that information turns out to be incomplete.

The legal defense component is often overlooked. If a creditor files a lien claim or an unknown heir challenges your ownership, your title insurer assigns legal counsel and covers the cost of fighting that claim. That protection alone justifies the premium for most buyers.

What are the two types of title insurance policies?

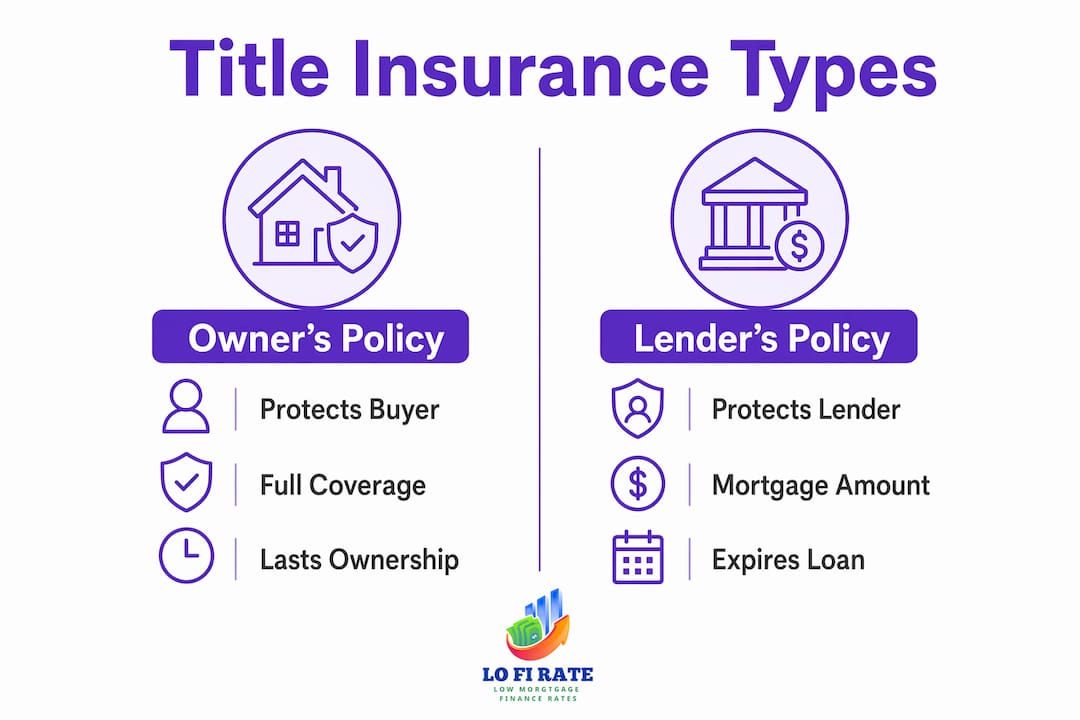

Two main types of title insurance exist: the owner's policy and the lender's policy. Each protects a different party and operates under different terms.

| Policy Type | Who It Protects | Coverage Amount | Duration |

|---|---|---|---|

| Owner's policy | The homebuyer | Full purchase price | Lasts as long as you own the property |

| Lender's policy | The mortgage lender | Outstanding loan balance | Expires when the loan is paid off |

The lender's policy is almost always required when you take out a mortgage. It protects the bank's financial interest in the property, not yours. If a title defect surfaces and you lose the property, the lender recovers its loan balance. You recover nothing without your own owner's policy.

The owner's policy is technically optional in most states, but skipping it is a significant financial risk. It covers your full purchase price and pays for legal defense if your ownership is challenged. For real estate investors who hold multiple properties, the owner's policy is a non-negotiable part of the acquisition cost.

Enhanced owner's policies are also available. An enhanced owner's policy costs about 20% more than a standard policy but provides broader coverage, including protection against zoning disputes, off-record matters, and even some post-ownership forgery claims. Buyers in high-risk markets or those purchasing older properties should weigh whether that added coverage fits their situation.

What does title insurance cover?

Title insurance covers a wide range of defects that standard property inspections cannot detect. The National Association of Realtors identifies the most common covered defects as:

- Forged documents: A prior deed or release of lien was signed by someone impersonating the true owner.

- Unknown heirs: A deceased prior owner had heirs who were never notified of the sale and now claim ownership.

- Unpaid liens: A contractor, tax authority, or lender placed a lien on the property that was never paid or released.

- Clerical errors: A recording mistake in the county records created a gap or conflict in the chain of title.

- Boundary disputes: A neighbor or municipality claims a portion of the land based on a conflicting survey or historical record.

Each of these defects can surface years after closing. A contractor lien from a renovation done by a prior owner, for example, may not appear in public records until the contractor files a claim. Without title insurance, you would owe that debt even though you had no part in creating it.

The financial exposure is real. Boundary disputes can require surveys, legal filings, and court appearances. Heir claims can freeze your ability to sell or refinance. Forged deed cases can result in complete loss of ownership. Title insurance covers legal costs and settlements in all of these scenarios.

Pro Tip: If you are buying a property that was recently inherited or sold through an estate, request an enhanced owner's policy. Estate sales carry a higher risk of unknown heir claims and documentation errors.

Real estate investors face compounded risk because they often acquire properties quickly, sometimes through foreclosure or off-market channels where title history is less clean. The benefits of title insurance for investors include ongoing protection across the full holding period, not just at the moment of purchase.

How much does title insurance cost, and can you shop for it?

Title insurance involves a single premium paid at closing, with no recurring monthly or annual payments. That one-time cost varies based on state regulations, the purchase price of the property, and the provider you choose.

The National Association of Insurance Commissioners confirms that costs vary by state and provider, and that shopping around can reduce your closing costs. That is a point most buyers miss entirely.

Key factors that affect your premium:

- State regulations: Some states set fixed rates for title insurance. Others allow providers to compete on price.

- Property purchase price: Premiums scale with the value of the property being insured.

- Standard vs. enhanced coverage: Enhanced policies carry a higher premium, typically around 20% more.

- Provider fees: Title companies charge additional fees for searches, settlements, and document preparation that are separate from the insurance premium itself.

Many buyers assume they must use the title company recommended by the seller or real estate agent. That assumption is wrong. Buyers have the right in many states to select their own title insurance provider. Exercising that right can lower your closing costs and give you access to better service.

Understanding which closing costs are fixed and which are negotiable is a practical skill. Lofirate's guide to closing costs for homebuyers breaks down exactly which fees you can push back on and which ones are set by law. Knowing that distinction before you sit at the closing table puts real money back in your pocket.

For a broader view of how real estate ownership protects your financial interests, including the role title insurance plays in securing those interests, it helps to understand the full picture of property ownership costs and benefits.

Key Takeaways

Title insurance is a one-time purchase at closing that protects your legal ownership rights and covers legal defense costs for defects that existed before you bought the property.

| Point | Details |

|---|---|

| One-time premium | You pay once at closing; coverage lasts as long as you own the property. |

| Two policy types | Owner's policy protects you; lender's policy protects your mortgage lender. |

| 135-step process | Title companies complete about 135 steps before closing to verify and clear title. |

| Shop for providers | Many states allow buyers to choose their own title insurer, which can lower costs. |

| Enhanced coverage | An enhanced owner's policy costs about 20% more but covers broader risks including fraud and zoning disputes. |

Why I think most buyers underestimate title insurance

Most buyers treat title insurance as a line item on the closing disclosure, something to sign off on and forget. That is the wrong way to look at it.

The real value is not in the policy document. It is in the 135-step investigation that happens before the policy is ever issued. Title companies are doing forensic work on your behalf, tracing ownership through decades of public records, clearing liens, and fixing errors before they become your problem. That process eliminates most claims before they can ever happen. The insurance is the backstop for what the search cannot catch.

I have seen buyers skip the owner's policy to save a few hundred dollars at closing, only to face a lien claim or boundary dispute years later with no coverage. The math never works in their favor. A one-time premium that covers the full purchase price and provides legal defense for the life of your ownership is one of the most cost-efficient protections in real estate.

The shopping angle is also underused. Buyers who compare title insurance providers in states that allow it often find meaningful price differences for identical coverage. That is not a small thing when you are already stretching to cover a down payment and closing costs. Lofirate's resource on transparent mortgage pricing is a good starting point for understanding how title insurance fits into your total loan cost picture.

Title insurance is not glamorous. It is not the part of homebuying that anyone gets excited about. But it is the part that protects everything else you worked for.

— LoFi

How Lofirate helps you close with confidence

Buying a home means managing a lot of moving parts at once, and title insurance is just one piece of the closing cost puzzle.

Lofirate connects homebuyers and real estate investors with licensed wholesale mortgage brokers who shop multiple lenders to find competitive rate options. That means you get a second opinion on your mortgage pricing before you commit. Wholesale brokers also understand closing costs in detail, including how to evaluate title insurance charges and identify fees that may be negotiable. Visit Lofirate to request a no-obligation consultation and see what a lower rate could mean for your total purchase cost. You can also review available loan options to find the right fit for your situation.

FAQ

What is the title insurance definition in simple terms?

Title insurance is a policy that protects property buyers and lenders from financial loss caused by defects in a property's ownership history that existed before the purchase. Coverage is purchased once at closing and lasts for the duration of ownership.

Do I need title insurance if I pay cash for a home?

A lender's policy is not required without a mortgage, but an owner's policy is still strongly recommended. Cash buyers face the same risks from forged deeds, unknown heir claims, and unpaid liens as financed buyers.

How does title insurance differ from homeowners insurance?

Homeowners insurance covers physical damage to your property from events like fire or theft. Title insurance covers legal and financial claims tied to ownership history, such as liens, boundary disputes, and document fraud.

Can I choose my own title insurance company?

Many states allow buyers to select their own title insurance provider rather than using the seller's or agent's recommended company. Shopping providers in those states can reduce your closing costs.

How long does title insurance coverage last?

An owner's title insurance policy lasts for as long as you or your heirs hold an interest in the property. A lender's policy expires when the mortgage loan is paid off.