Most homeowners believe their bank offers the best mortgage rates, yet many overpay by thousands without realizing it. The difference between wholesale mortgage brokers and retail lenders creates a pricing gap that can save you about $10,000 over your loan's life. Wholesale brokers access multiple lenders and operate under lower compensation caps, delivering genuinely competitive rates that retail banks simply cannot match. This article breaks down what competitive mortgage rates actually mean, why wholesale channels consistently beat retail pricing, and how you can secure the best possible deal on your mortgage in 2026.

Table of Contents

- What Are Competitive Mortgage Rates And Why Do They Matter?

- How Wholesale Mortgage Brokers Deliver Competitive Mortgage Rates

- Comparing Wholesale And Retail Mortgage Rates: What Borrowers Should Know

- How To Shop And Secure Competitive Mortgage Rates With Wholesale Brokers In 2026

- Save More On Your Mortgage With Lo Fi Rate In 2026

Key takeaways

| Point | Details |

|---|---|

| Wholesale brokers save money | Lower compensation caps and multi-lender access reduce your borrowing costs significantly. |

| Rate competition matters | Shopping multiple lenders through brokers reveals pricing differences that can save thousands. |

| Structural advantages exist | Wholesale channels operate with 2.75% caps versus retail margins of 4.5% to 6%. |

| Knowledge equals savings | Understanding competitive rates empowers better mortgage decisions and long-term financial health. |

What are competitive mortgage rates and why do they matter?

Competitive mortgage rates represent the lowest borrowing costs available across multiple lenders for your specific financial profile. These rates fluctuate daily based on market conditions, Federal Reserve policies, and individual lender pricing strategies. When you secure a competitive rate, you reduce both your monthly payment and the total interest paid over your loan's lifetime.

How lender competition lowers mortgage rates creates pricing pressure that benefits borrowers. A single lender quotes only their own pricing, which includes their profit margins and operational costs. Multiple lenders competing for your business drive rates down as each tries to win your loan. This competitive dynamic forms the foundation of wholesale mortgage pricing.

Understanding competitive rates transforms how you approach mortgage shopping. Many borrowers accept the first offer from their bank without realizing better options exist. A difference of just 0.25% on a $400,000 mortgage costs you approximately $20,000 in additional interest over 30 years. That quarter-point represents real money that stays in your pocket when you choose competitive pricing.

Competitive rates matter because they directly impact your financial flexibility. Lower monthly payments free up cash for investments, emergency savings, or quality of life improvements. Reduced closing costs mean less money needed at the table, making homeownership more accessible. The mortgage market rewards informed shoppers who understand these dynamics and take action.

Key factors that determine competitive mortgage rates include:

- Your credit score and debt-to-income ratio, which affect lender risk assessments

- Current market interest rate environment and economic indicators

- Loan-to-value ratio and down payment amount on your property

- Property type, location, and intended use as primary residence or investment

- Lender's current capacity and appetite for new loan originations

How wholesale mortgage brokers deliver competitive mortgage rates

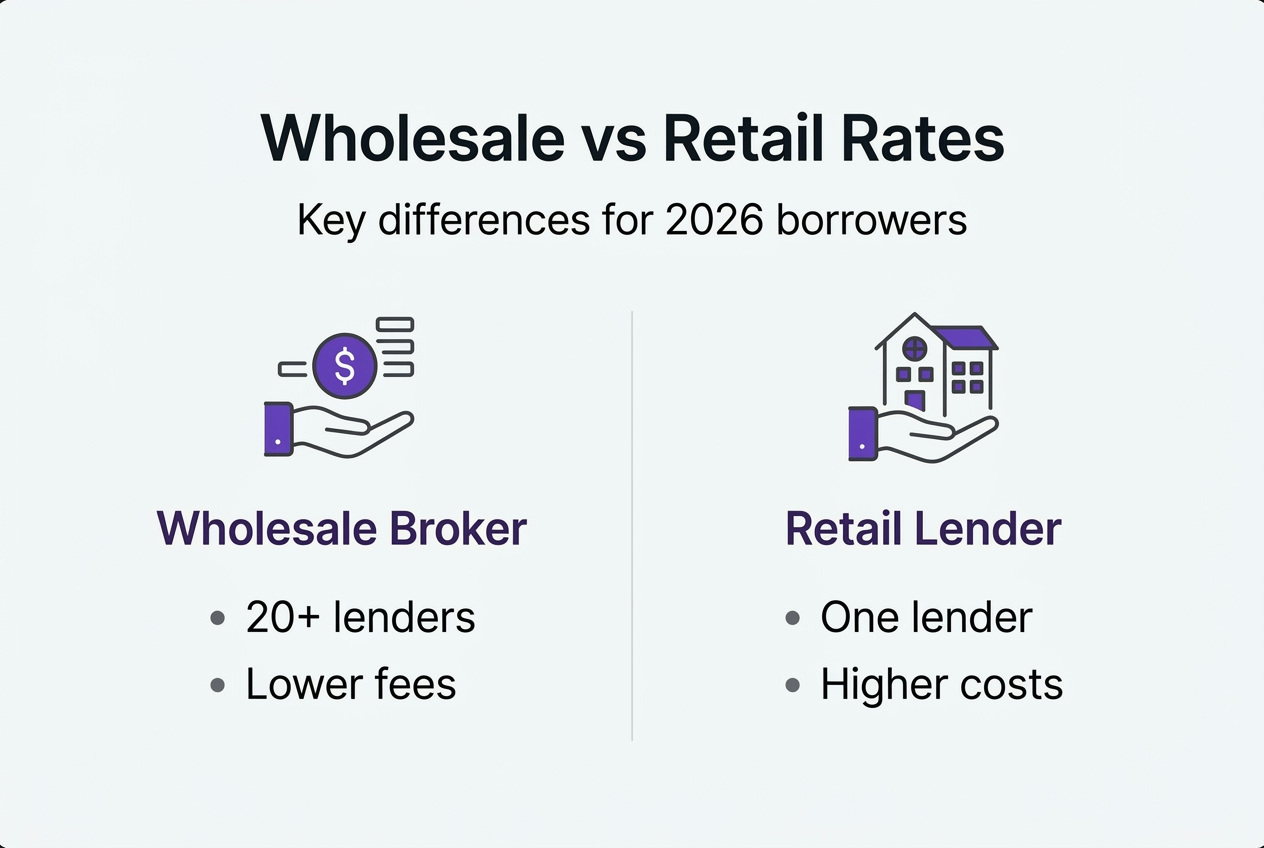

Wholesale mortgage brokers operate fundamentally differently than retail lenders, creating structural advantages that translate into better pricing for you. A retail lender employs loan officers who can only offer that institution's rates and products. A wholesale broker partners with dozens of lenders, shopping your scenario across multiple rate sheets to find the best match.

This multi-lender access creates genuine competition for your business. Lenders know brokers can easily move your application to a competitor, incentivizing aggressive pricing. The wholesale mortgage channel consistently delivers superior outcomes, saving borrowers about $10,000 on average compared to retail channels. That savings comes from lower rates, reduced fees, or a combination of both.

Compensation structures explain much of this pricing advantage. Mortgage brokers' compensation is capped at 2.75% of the loan amount, while retail lender margins typically range from 4.5% to 6%. This difference represents thousands of dollars that either goes to the lender's profit or stays with you through better pricing. Federal regulations enforce these caps to protect consumers from excessive fees.

Wholesale brokers also provide flexibility that retail officers cannot match. If one lender's underwriting proves problematic, brokers can pivot to another without restarting your application. When shopping with wholesale brokers, you gain access to specialized loan products and niche lenders that excel in specific scenarios like self-employment income or investment properties.

| Feature | Wholesale Broker | Retail Lender |

|---|---|---|

| Lender Access | 20 to 50+ lenders | Single institution only |

| Compensation Cap | 2.75% maximum | 4.5% to 6% margins |

| Rate Flexibility | Shops multiple rate sheets | Limited to one rate sheet |

| Product Variety | Extensive specialized options | Standard product menu |

| Pricing Transparency | Required fee disclosures | Often bundled or hidden |

Pro Tip: Ask your broker how many lenders they actively use and request to see rate comparisons from at least three different wholesale partners. This transparency confirms they're genuinely shopping your loan rather than steering you to their highest-paying lender relationship.

Comparing wholesale and retail mortgage rates: What borrowers should know

The pricing gap between wholesale and retail channels stems from operational differences that affect your bottom line. Retail lenders maintain expensive branch networks, large marketing budgets, and shareholder profit expectations. These costs get passed to borrowers through higher interest rates and origination fees. Wholesale lenders operate leaner operations focused solely on loan production, eliminating many overhead expenses.

Lower margins in the wholesale channel translate directly into lower interest rates, lower closing costs, or a combination of both. A typical scenario might show a retail bank quoting 6.5% with $3,000 in lender fees, while a wholesale broker finds 6.25% with $1,500 in fees for the identical borrower profile. Over 30 years, that quarter-point rate difference plus reduced fees saves approximately $18,000.

Retail lenders also lack incentive to offer their best pricing upfront. Their loan officers earn commissions based on the margin between the rate you accept and the rate the lender could have offered. This creates a conflict of interest where better deals for you mean lower compensation for them. Wholesale brokers earn flat fees regardless of rate, aligning their interests with yours.

When comparing lending options, focus on the annual percentage rate, which includes both interest and fees, for accurate comparisons. A lower rate with high fees might cost more than a slightly higher rate with minimal fees. Run the numbers for your expected holding period, since you may refinance or sell before 30 years.

| Cost Component | Typical Wholesale | Typical Retail | Your Savings |

|---|---|---|---|

| Interest Rate | 6.25% | 6.50% | 0.25% lower |

| Origination Fees | $1,500 | $3,000 | $1,500 saved |

| Total Interest (30yr, $400k) | $520,000 | $540,000 | $20,000 saved |

| Monthly Payment | $2,462 | $2,528 | $66 monthly |

Consider these factors when evaluating wholesale versus retail mortgage options:

- Total closing costs including all lender and third-party fees

- Loan estimate transparency and willingness to explain each line item

- Rate lock policies and protection against market rate increases

- Underwriting flexibility for unique income or credit situations

- Timeline for closing and lender's track record for on-time closings

Pro Tip: Request loan estimates from both a wholesale broker and your bank on the same day, then compare them side by side. The benefits of comparing lenders become immediately obvious when you see the pricing differences in writing. Many borrowers discover they can negotiate better terms once armed with competing offers.

How to shop and secure competitive mortgage rates with wholesale brokers in 2026

Securing the best possible mortgage rate requires a systematic approach to shopping and comparison. Follow these steps to maximize your savings through wholesale broker access:

- Check your credit reports from all three bureaus and dispute any errors at least 60 days before applying, since corrections take time to process.

- Gather financial documentation including two years of tax returns, recent pay stubs, bank statements, and any asset verification needed for your down payment.

- Research and contact at least three licensed wholesale mortgage brokers in your state, asking each about their lender network size and specialty areas.

- Request loan estimates from each broker for the same loan amount, down payment, and property type to ensure accurate comparisons.

- Compare not just rates but also closing costs, rate lock periods, and estimated timeline to closing for each offer.

- Ask detailed questions about rate lock policies, including whether you can relock if rates drop and what fees apply for extensions.

- Verify the broker's license status with your state regulator and check for any disciplinary actions or consumer complaints.

Wholesale mortgage brokers provide choice and adaptability to market conditions, unlike retail officers limited to single rate sheets. This flexibility proves especially valuable when rates fluctuate or when your financial situation presents unique challenges. A skilled broker knows which lenders handle self-employment income most favorably or which ones offer the best pricing for investment properties.

Timing your rate lock strategically can save additional money. Rates change daily, sometimes multiple times per day during volatile periods. Most brokers offer rate locks ranging from 30 to 60 days, with longer locks costing more. Lock when you're comfortable with the rate and confident you'll close within the lock period, since extensions typically cost 0.125% to 0.25% of your loan amount.

When shopping wholesale mortgage lenders, pay attention to the broker's communication style and responsiveness. You want someone who explains options clearly, returns calls promptly, and proactively manages your timeline. Technical expertise matters, but so does the relationship, since you'll work closely together for 30 to 45 days.

Pro Tip: Ask brokers specifically about their compensation on your loan and whether they receive any backend payments from lenders. Transparent brokers disclose this information readily and can explain how their fees compare to retail alternatives. Understanding mortgage qualification steps helps you prepare documentation and avoid delays that could cause your rate lock to expire.

Save more on your mortgage with Lo Fi Rate in 2026

Now that you understand how competitive mortgage rates work and why wholesale brokers deliver superior value, take the next step toward significant savings. Lo Fi Rate connects you with licensed wholesale mortgage brokers who shop dozens of lenders to find your best possible rate and terms. Unlike retail banks limited to their own pricing, our broker network accesses wholesale rates that can save you thousands over your loan's life.

Our platform simplifies the mortgage shopping process while maintaining complete transparency. You'll receive personalized rate quotes from multiple lenders, clear explanations of all fees and costs, and expert guidance through every step of the application process. Whether you're purchasing your first home, upgrading to a larger property, or refinancing to lower your current rate, Lo Fi Rate provides the wholesale access and professional support you need.

Visit Lo Fi Rate today to explore your mortgage financing options and discover how much you can save with competitive wholesale pricing.

Frequently asked questions

What is the main difference between wholesale and retail mortgage rates?

Wholesale mortgage rates come from brokers who shop multiple lenders and operate under 2.75% compensation caps, while retail rates come from banks with higher profit margins of 4.5% to 6%. This structural difference typically saves wholesale borrowers about $10,000 over the loan's life through lower rates and reduced fees.

How can I verify that I'm getting a truly competitive mortgage rate?

Request loan estimates from at least three different sources on the same day, including both wholesale brokers and retail lenders. Compare the annual percentage rate, which includes all fees, rather than just the interest rate. Check current market rate averages on financial websites to ensure your quotes align with prevailing conditions.

Does my credit score affect how competitive my mortgage rate will be?

Your credit score significantly impacts the rates lenders offer, with scores above 740 typically qualifying for the best pricing. Each 20-point drop in score can increase your rate by 0.25% to 0.5%. Wholesale brokers can sometimes find lenders who price more favorably for specific credit profiles, giving you an advantage over single-lender options.

When is the best time to lock in my mortgage rate?

Lock your rate when you're satisfied with the pricing and confident you'll close within the lock period, typically 30 to 60 days. Avoid locking too early if rates are trending downward, but don't wait too long if rates are rising. Many brokers offer float-down options that let you capture lower rates if they drop after locking, though this feature may cost extra.

What closing costs should I expect with competitive wholesale mortgage rates?

Typical wholesale closing costs range from 2% to 5% of your loan amount, including origination fees of $1,500 to $2,500, appraisal fees of $400 to $600, title insurance, and various third-party charges. Wholesale brokers often deliver lower lender fees than retail banks, though third-party costs remain similar. Always review your loan estimate carefully and ask about any charges you don't understand.