TL;DR:

- Your credit score significantly impacts mortgage interest rates and long-term costs.

- Lenders use different scoring models and bureaus, affecting your actual mortgage score.

- Improving payment history and reducing debt before applying can save you thousands over the loan term.

Most homebuyers assume their credit score is either "good enough" or "not good enough." The reality is far more nuanced. A 20 to 40 point difference between two borrowers can translate into a meaningfully different interest rate, and over a 30-year loan, that gap can cost tens of thousands of dollars. Yet most people never check which scoring model a lender is using, never compare rate offers across lenders, and never realize they could have qualified for a better deal. This guide breaks down exactly how credit scores shape mortgage rates, which models lenders use, and what you can do right now to put yourself in a stronger position.

Table of Contents

- What is a credit score and how do lenders use it?

- How credit scores impact mortgage rates and costs

- Which credit scoring models do lenders use?

- How to improve your credit score before applying for a mortgage

- What most homebuyers miss about credit scores and mortgage rates

- Find your best mortgage rate with expert guidance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Small score changes matter | A shift of just 20 points can cost or save you thousands on your mortgage. |

| Know your credit model | Lenders use different credit score models that can produce varied results and offers. |

| Optimize before you apply | Improving your credit 3-12 months ahead can place you in a lower rate tier and save significant money. |

| Shop around for rates | Compare multiple lenders, as each may view your credit differently and offer distinct mortgage rates. |

What is a credit score and how do lenders use it?

A credit score is a three-digit number, typically ranging from 300 to 850, that summarizes your creditworthiness based on your borrowing and repayment history. The higher the number, the less risk you represent to a lender. Simple enough. But when it comes to mortgages, the way lenders use that number is more specific than most people realize.

Mortgage lenders do not pull a single generic credit score. Instead, they pull what is called a tri-merge report, which means they request your credit file from all three major bureaus: Equifax, Experian, and TransUnion. Each bureau produces its own score, and lenders typically use the middle score of the three for approval and pricing decisions. If you are applying jointly with a co-borrower, lenders often use the lower of the two middle scores.

The scoring model used for most mortgage applications is FICO, and not just one version of it. Lenders use bureau-specific FICO versions: FICO 2 from Experian, FICO 4 from TransUnion, and FICO 5 from Equifax. These models are older than the FICO scores you see on free credit monitoring apps, which means your "consumer" score and your "mortgage" score can look very different.

"FICO dominates mortgage scoring, used by roughly 90% of lenders, through bureau-specific versions that differ from the scores consumers typically see."

Here is how credit scores affect your mortgage application in practice:

- Pre-approval eligibility: Lenders use your score to decide whether you qualify at all.

- Interest rate offers: Higher scores unlock lower rate tiers.

- Loan program access: Some programs require minimum scores to participate.

- Private mortgage insurance (PMI) requirements: Lower scores can trigger higher PMI costs.

- Loan-to-value limits: Some lenders cap borrowing amounts based on score thresholds.

Understanding these mortgage qualification steps before you apply puts you in a much better position to negotiate and compare offers with confidence.

How credit scores impact mortgage rates and costs

Now that you know how lenders calculate and use your credit score, let's see how those numbers translate into actual mortgage rates and costs.

Lenders group borrowers into rate tiers based on credit score ranges. The difference between one tier and the next might seem small on paper, but it adds up fast over 30 years. Here is a realistic look at how a $300,000 fixed-rate mortgage might be priced across score ranges:

| Credit score range | Estimated rate | Monthly payment | Total interest paid |

|---|---|---|---|

| 760 and above | 6.50% | $1,896 | $382,560 |

| 700 to 759 | 6.75% | $1,946 | $400,560 |

| 660 to 699 | 7.10% | $2,014 | $425,040 |

| 620 to 659 | 7.50% | $2,098 | $455,280 |

Note: Rates are illustrative examples for comparison purposes only and do not represent current market offers.

The gap between a 760 score and a 620 score in this example is over $72,000 in total interest. That is not a rounding error. That is a real financial outcome tied directly to a three-digit number.

Part of what drives these differences is something called loan-level price adjustments (LLPAs). These are fees set by Fannie Mae and Freddie Mac that lenders add to loan pricing based on risk factors, including your credit score. A lower score means higher LLPAs, which translate into a higher rate or more upfront fees.

It is also worth noting that FICO and VantageScore scores can differ by 20 to 40 points for the same borrower, which means the score you see on a free app may not reflect what a mortgage lender actually sees.

Keeping an eye on 2026 mortgage rate trends helps you time your application, but your credit score is the lever you control directly. Understanding how market trends affect mortgage rates is useful context, but your personal score determines which rate within that market you actually receive.

Pro Tip: If your score is sitting at 695, even a 10-point improvement to 705 could move you into a better rate tier and save you more than the time it takes to get there.

Which credit scoring models do lenders use?

With mortgage costs tied closely to your score, it is important to know which model is being used, and recent changes mean buyers need to pay attention.

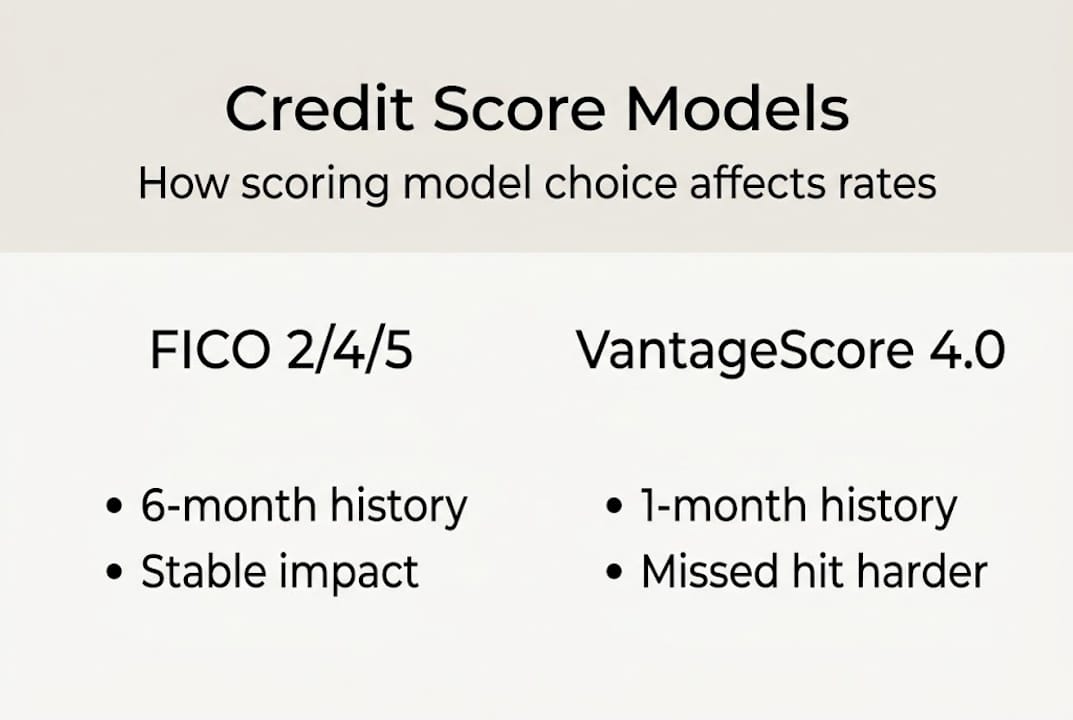

For decades, the answer was straightforward: mortgage lenders used FICO 2, FICO 4, and FICO 5. These models weight your payment history, amounts owed, length of credit history, new credit, and credit mix to produce a score. They require at least six months of credit history and at least one account reported within the past six months to generate a score at all.

That changed after 2025. VantageScore 4.0 is now an alternative for GSE loans following the FHFA's update, meaning some lenders can use it for loans backed by Fannie Mae and Freddie Mac. This matters because VantageScore 4.0 can score borrowers with as little as one month of credit history, which opens the door for people with thin credit files who previously could not qualify.

Here is how the two models compare:

| Feature | FICO 2/4/5 | VantageScore 4.0 |

|---|---|---|

| Minimum credit history | 6 months | 1 month |

| Payment history weight | 35% | 41% |

| Used by most lenders | Yes (90%+) | Growing adoption |

| GSE eligible | Yes | Yes (post-2025) |

| Trended data used | No | Yes |

The higher payment history weight in VantageScore 4.0 means a single missed payment can hurt you more under that model. On the flip side, borrowers who have been consistently on time may score slightly higher with VantageScore.

For borrowers with limited credit history, the model switch can be the difference between qualifying and not qualifying at all. For established borrowers, it can mean a different rate offer depending on which model the lender chooses.

Pro Tip: Ask your lender directly which scoring model they are using. Then explore lender alternatives and models to understand whether a different lender using a different model might offer you a better deal.

How to improve your credit score before applying for a mortgage

After understanding the models and what they mean for your rates, here is how you can actively improve your credit profile for the best mortgage deals.

Your credit score is built from five main factors: payment history, amounts owed, length of credit history, new credit inquiries, and credit mix. Payment history carries 41% weight under VantageScore and 35% under FICO, making it the single most influential factor in either model.

Here are the most effective steps to raise your score before applying:

- Pay every bill on time, every month. Even one 30-day late payment can drop your score significantly. Set up autopay for minimums if needed.

- Lower your credit card utilization. Aim to use less than 30% of your available credit limit. Under 10% is even better for scoring purposes.

- Avoid opening new credit accounts. Each new application triggers a hard inquiry, which can temporarily lower your score.

- Dispute errors on your credit report. Pull your free reports from AnnualCreditReport.com and check for inaccuracies. Errors are more common than people expect.

- Keep your oldest accounts open. Closing old accounts shortens your average account age, which can hurt your score.

- Become an authorized user. If a family member has a long-standing account with low utilization, being added as an authorized user can boost your score quickly.

Pro Tip: Even a modest score improvement can move you into a lower rate bucket. Start comparing mortgage rates before and after your credit work to see the real dollar impact. And when you are ready to apply, comparing lenders is just as important as improving your score.

Ideally, begin this prep work 3 to 12 months before you plan to apply. The longer your runway, the more options you have.

What most homebuyers miss about credit scores and mortgage rates

Equipped with actions to improve your score, it is worth considering a few counterintuitive truths most borrowers never hear.

The first is about the 800 obsession. Many buyers push hard to crack 800, believing it unlocks the best possible rate. But most lenders stop differentiating at around 760. Once you clear that threshold, you are already in the top rate bucket. Grinding from 765 to 810 will not move your mortgage rate at all. That energy is often better spent on other parts of your financial profile.

The second is about bureau and model differences. FICO and VantageScore can differ by 20 to 40 points for the same borrower, and different bureaus may report different information. A buyer who thinks their score is 730 based on a free app might find their mortgage score is 695, which puts them in a different rate tier entirely.

The third truth is about lender competition and rates. Your credit score is one input, but it is not the only lever. Two lenders looking at the same borrower with the same score can offer meaningfully different rates based on their own pricing, lender network, and overhead. One buyer we know had a 718 score and received rate offers that varied by nearly half a percentage point just by shopping across lenders. Over 30 years, that difference was worth more than $30,000. The score got him in the door. The shopping got him the deal.

Find your best mortgage rate with expert guidance

With these insights in mind, here is how you can make your next mortgage move more confidently.

You now understand how credit scores shape rate offers, which models lenders use, and how to improve your profile before applying. The next step is putting that knowledge to work with the right support.

At LoFiRate.com, we connect homebuyers and homeowners with licensed wholesale mortgage brokers who shop multiple lenders on your behalf. Unlike retail lenders who show you only their own pricing, wholesale brokers access a broader network to find competitive loan options tailored to your credit profile. Our broker matching services are free, transparent, and come with no obligation. Whether you are buying your first home or refinancing, getting a second opinion on your rate could be one of the most valuable steps you take.

Frequently asked questions

What is the minimum credit score needed for a mortgage in 2026?

Most lenders require at least a 620 credit score for conventional loans, but FICO-based cutoffs vary by program, and some government-backed loans allow scores as low as 580 with additional requirements.

How much difference does 20 points make in my credit score?

A 20-point difference can shift you into a different rate tier, and 20 to 40 point gaps between scoring models mean the score you see may not match what your lender sees, potentially costing thousands over the loan term.

Do all lenders use the same credit score model for mortgages?

No. Most lenders use specific FICO versions, but VantageScore 4.0 is now GSE-eligible following the 2025 FHFA update, so the model used can vary depending on the lender and loan type.

How soon before applying for a mortgage should I start improving my credit?

Start at least 3 to 12 months before applying. VantageScore scores thin files in as little as one month, but building a strong payment history takes consistent effort over time to move the needle meaningfully.