TL;DR:

- Comparing multiple lenders through digital tools can save homebuyers tens of thousands of dollars over the loan term.

- Technology enables real-time rate comparison, faster approvals, and access to wholesale broker networks.

- Risks include privacy concerns and AI bias; always use transparent, licensed platforms for mortgage shopping.

Most homebuyers accept the first mortgage offer they receive, assuming all lenders charge roughly the same. That assumption is expensive. Few borrowers shop around, but those who do save approximately 11 basis points on their rate, which translates to tens of thousands of dollars over the life of a loan. Today's technology makes comparison shopping faster, less confusing, and more accessible than ever, even for buyers who have never worked with a mortgage broker before. This guide breaks down exactly how digital tools work, where the biggest savings hide, and how to protect yourself as you use them.

Table of Contents

- Why most homebuyers miss out on savings

- How technology transforms mortgage shopping

- Comparing retail lenders vs. wholesale brokers: Where tech makes a difference

- How much you can save: The real numbers

- What to watch out for: Risks and how to protect yourself

- Our take: The technology advantage belongs to the prepared, not just the tech-savvy

- Find a wholesale broker and stop leaving money on the table

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Tech saves you money | Using digital tools to shop for a mortgage can potentially save you tens of thousands of dollars on your loan. |

| Wholesale access now easier | Online comparison platforms connect you with wholesale brokers, unlocking better rates and more options. |

| Tech boosts speed and approval | Modern mortgage technology speeds up processing and can help more borrowers qualify, including those with nontraditional profiles. |

| Know the risks | AI and digital tools can introduce privacy and fairness concerns, so check each platform’s credibility and policies. |

Why most homebuyers miss out on savings

The mortgage process feels overwhelming for most people. You're juggling inspections, negotiations, moving plans, and paperwork, so when a familiar bank offers you a rate, accepting it feels like one less thing to stress over. That instinct is understandable. It's also costly.

Empirically, relatively few buyers shopped multiple lenders during the 2018 to 2020 analysis period, even though those who did consistently secured better rates. The gap isn't trivial. Understanding why comparing lenders saves money is the first step toward not leaving thousands on the table.

Here are the most common reasons buyers skip the comparison process:

- Loyalty to a familiar bank. Many buyers assume their current bank will reward their relationship with a better rate. Banks rarely do.

- Fear of multiple credit inquiries. Buyers worry that shopping around will hurt their credit score. In reality, multiple mortgage inquiries within a 14 to 45-day window are treated as a single inquiry by scoring models.

- Unfamiliarity with wholesale brokers. Most buyers have heard of Chase, Wells Fargo, or Rocket Mortgage, but have no idea that wholesale brokers can access dozens of lenders simultaneously and often beat retail pricing.

- Overwhelm. The sheer volume of loan products, terminology, and paperwork makes comparison feel impossible without guidance.

The result? Buyers stuck with rates that are a quarter point or more higher than what a broker could have found them.

"Shopping for a mortgage isn't just a financial best practice. It's potentially the single highest-return action you can take during the homebuying process, and technology has finally made it realistic for everyday buyers."

Pro Tip: If you've already received a rate from your bank, treat it as a starting point, not a final offer. Getting one additional quote from a wholesale broker costs you nothing and could reveal significant savings.

Technology changes this dynamic entirely. Platforms that aggregate broker access, AI-powered affordability calculators, and automated underwriting tools have transformed what used to take weeks of phone calls into a streamlined digital process. The savings opportunity was always there. Now the tools to access it are too.

How technology transforms mortgage shopping

Not long ago, shopping for a mortgage meant scheduling appointments at multiple banks, submitting the same paperwork repeatedly, and waiting days for a response. Today, digital mortgage tools are changing that entirely by providing real-time rate comparisons, automated pre-approvals, and direct access to wholesale broker networks.

Here's what modern mortgage technology actually does for you:

- AI-powered affordability tools analyze your income, debt, and credit profile to estimate what you qualify for in minutes, not days.

- Online broker-matching platforms like Mortgage Matchup connect buyers directly with wholesale brokers without requiring you to know the industry landscape.

- Automated underwriting systems process your application data faster and with fewer manual errors, shrinking approval timelines dramatically.

- Real-time rate comparison dashboards pull live pricing from multiple lenders simultaneously so you can see where your rate actually stands in the market.

The speed improvement alone is significant. FinTech lenders process loans approximately 20% faster than traditional channels, which matters in competitive housing markets where sellers favor buyers who can close quickly.

| Technology type | What it does | Benefit for buyers |

|---|---|---|

| AI affordability calculators | Estimates purchasing power based on financial profile | Faster, more accurate planning |

| Broker-matching platforms | Connects buyers to wholesale broker networks | Access to lower wholesale pricing |

| Automated underwriting | Evaluates application data algorithmically | Faster approvals, fewer manual errors |

| Rate comparison dashboards | Aggregates live rates from multiple lenders | Transparent, side-by-side pricing |

| Document upload portals | Digitizes the paperwork process | Less friction, fewer delays |

Over 30% of buyers now use AI tools to estimate affordability before they ever speak to a lender. That's a massive shift in how people enter the process, and it gives informed buyers a real advantage. When you know your numbers before the conversation starts, you're harder to oversell.

Pro Tip: Use a mortgage shopping checklist before you start. Knowing the steps in order prevents you from missing documents, jumping ahead, or accepting terms without proper context. Preparation makes tech tools work better for you. You can also learn how to compare mortgage rates effectively before committing to any lender.

The real power of these tools isn't just speed. It's access. Wholesale broker networks were once invisible to most homebuyers. Technology now surfaces them directly, putting buyers in contact with professionals who can shop dozens of lenders on their behalf rather than offering a single in-house product.

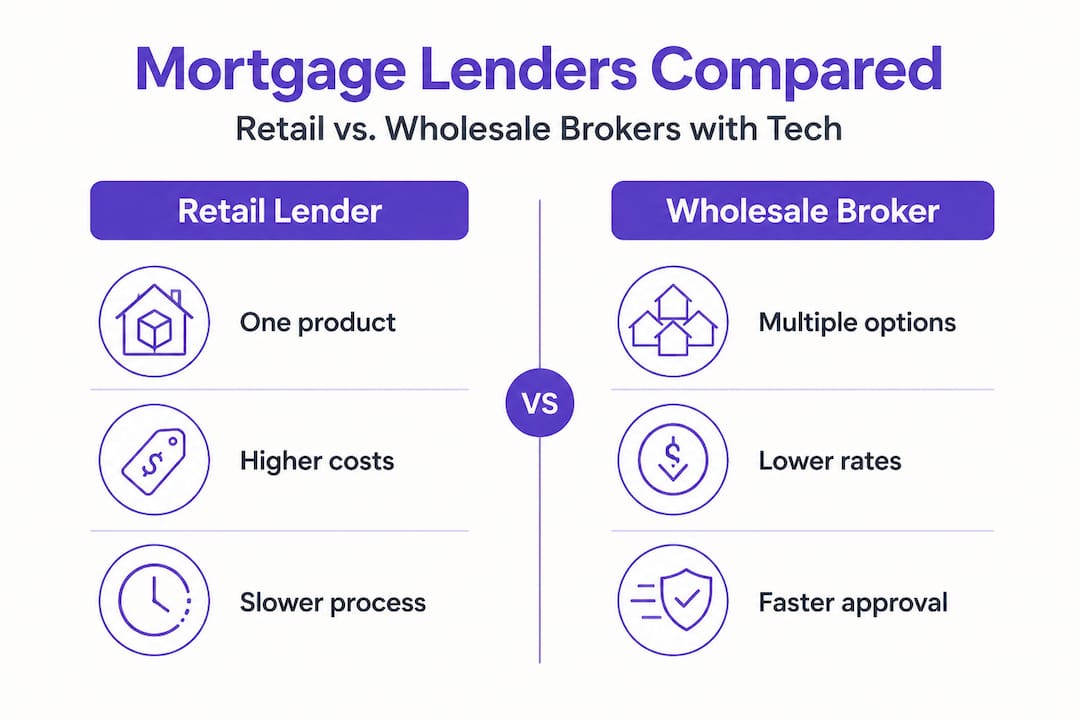

Comparing retail lenders vs. wholesale brokers: Where tech makes a difference

Understanding the difference between retail lenders and wholesale brokers is critical to getting the most out of mortgage technology.

Retail lenders (banks, credit unions, direct mortgage companies) offer their own loan products at prices that include their overhead and profit margin. When you walk into a bank, you're seeing one menu. Their technology improvements have made the application process smoother, but you're still limited to what they sell.

Wholesale brokers operate differently. They work with a network of wholesale lenders who compete for your loan, which typically results in lower rates and more flexible approval criteria. The broker's job is to find the best match for your specific situation, not to push a single product.

Here's where technology makes the wholesale advantage even more accessible:

- Broker portals now let licensed wholesale brokers submit your application to multiple lenders simultaneously, reducing the time to find the best fit from days to hours.

- Digital comparison tools let brokers show you side-by-side pricing across lenders in a format you can actually read and evaluate.

- AI-driven matching helps brokers identify which lender programs are most likely to approve your specific profile, which is especially valuable for nontraditional borrowers.

- Electronic document systems allow faster verification, which means quicker commitments from wholesale lenders.

| Factor | Retail lender | Wholesale broker with tech |

|---|---|---|

| Rate competitiveness | Single product line | Multiple lenders compete for your loan |

| Self-employed approval | Typically strict guidelines | Flexible programs, 78% vs. 41% approval |

| Jumbo loan options | Limited | Access to specialty wholesale programs |

| Speed (standard loans) | Fast for simple cases | Comparable or faster via broker portals |

| Transparency | Varies | Real-time, side-by-side pricing |

The GAO mortgage market analysis found that self-employed borrowers, buyers with lower credit scores, jumbo loan seekers, and minority borrowers save significantly more through wholesale channels. VA loan borrowers, for example, saved an average of $13,000 by going through wholesale rather than retail.

Retail lenders lead on simplicity for straightforward borrowers with W-2 income and strong credit. But technology has largely closed the convenience gap for wholesale. Today, working with a broker through a digital platform is nearly as frictionless as applying directly with a retail bank, with the added benefit of rate competition.

If you're exploring your options, looking at Bankrate.com alternatives or Lend1.com alternatives can help you find platforms that surface wholesale broker connections rather than just retail quotes.

How much you can save: The real numbers

This is where things get concrete. The abstract idea of "better rates" becomes real when you see the dollar figures.

Shopping around for a mortgage can save borrowers up to $44,000 over the life of a 30-year loan on a typical home purchase. That figure comes from Realtor.com analysis of a $425,000 loan where buyers who compared multiple lenders secured rates up to 0.55 percentage points lower than those who accepted the first offer.

| Rate difference | Monthly savings | Annual savings | 30-year savings |

|---|---|---|---|

| 0.11% (avg. for shoppers) | ~$25 | ~$300 | ~$9,000 |

| 0.25% | ~$58 | ~$696 | ~$20,880 |

| 0.50% | ~$116 | ~$1,392 | ~$41,760 |

| 0.55% | ~$128 | ~$1,536 | ~$46,080 |

Estimates based on a $400,000 loan at a 7.0% baseline rate over 30 years. Actual savings vary.

Even the smallest savings from shopping, that 11 basis point average, adds up to roughly $9,000 over 30 years. Zillow research confirms that a 50 basis point difference saves buyers approximately $1,100 per year. These aren't lottery-ticket numbers. They're consistent, predictable savings that any buyer can access simply by comparing more than one offer.

Here's what makes the numbers even more compelling:

- Minority and underserved buyers see above-average savings when they access wholesale broker platforms, where lender competition is strongest.

- Buyers in higher loan amounts see proportionally larger savings from even small rate improvements.

- Refinancing homeowners can stack these savings on top of existing equity gains when they use tech-driven broker comparisons to time their refinance effectively.

Understanding how lender competition lowers rates gives you a structural advantage. When you know why competition drives rates down, you stop accepting single quotes and start expecting multiple.

The takeaway is simple: the cost of not shopping is measurable, and the tools to shop have never been more accessible or easier to use.

What to watch out for: Risks and how to protect yourself

Technology opens doors, but it also introduces risks you need to understand before you share your financial information online.

The GAO's review of mortgage market technology flagged two primary concerns: privacy risks from data sharing across digital platforms, and the potential for AI-driven tools to reflect or amplify existing lending disparities if their algorithms aren't carefully monitored. These risks don't mean you should avoid digital mortgage tools. They mean you should use them thoughtfully.

Here's what to watch for:

- Data sharing practices. Some comparison sites generate revenue by selling your information to multiple lenders, leading to a flood of unsolicited calls. Read the privacy policy before submitting your details.

- AI bias in approval models. Automated underwriting systems can inadvertently disadvantage certain borrower profiles if their training data reflects historical lending inequities. Ask your broker how their platform handles fair lending compliance.

- Misleading rate advertising. Some platforms display teaser rates that require exceptional credit, large down payments, or specific loan types. Always verify the conditions attached to any advertised rate.

- Unlicensed platforms. Not every mortgage-related website is operated by a licensed lender or broker. Check that any platform you use connects you with licensed professionals in your state.

- Pressure to decide quickly. Some digital platforms use urgency messaging to push you toward a fast decision. A good rate is worth a day of comparison, not an impulsive click.

"The platforms worth trusting are the ones that explain exactly how they work, who they share your data with, and what happens after you submit your information. Transparency is the price of your business."

Taking a few minutes to review mortgage compliance basics before you engage with any digital platform can help you ask the right questions and spot red flags before they become problems.

Our take: The technology advantage belongs to the prepared, not just the tech-savvy

Here's an opinion you won't hear from most mortgage content: the biggest beneficiaries of mortgage technology are not people who are comfortable with tech. They're people who are willing to ask one more question and get one more quote.

The tools are genuinely easy to use now. You don't need to understand how an automated underwriting engine works to benefit from one. You just need to show up on the right platform. What holds most buyers back isn't technological ability. It's the mistaken belief that the rate their bank offered is the market rate.

It isn't. Banks price loans for their profitability, not yours. Wholesale brokers, operating through technology-enabled platforms, let lenders compete for your loan, and that competition is what drives rates down. The technology doesn't create the savings. The competition does. Technology just makes the competition happen faster and more transparently.

The uncomfortable truth is that the mortgage industry has long relied on buyer inertia. Most people don't shop because the process felt painful. Now that it doesn't, the only remaining barrier is awareness. Once you know that a 30-minute comparison session could be worth $20,000 or more, you'll never accept a single quote again.

Find a wholesale broker and stop leaving money on the table

You've just read exactly how technology has shifted the mortgage landscape in favor of informed buyers. Now the question is whether you act on it.

At LoFiRate.com, we connect homebuyers and homeowners directly with licensed wholesale mortgage brokers in their state. Our platform doesn't lend money or quote rates directly. What we do is match you with a broker who can shop multiple wholesale lenders on your behalf, often finding rates that retail banks simply can't match. The consultation is transparent, there's no obligation, and you keep full control of the process. Whether you're purchasing your first home or refinancing an existing loan, getting a second opinion through a wholesale broker is one of the highest-value actions you can take right now.

Frequently asked questions

How do I use technology to compare mortgage rates easily?

Start with online comparison platforms and broker-matching sites that pull real-time rates from multiple lenders in one place, then connect with a licensed wholesale broker to explore options your bank won't show you.

Can using mortgage technology help if I'm self-employed or have a low credit score?

Absolutely. Broker-matching platforms connect nontraditional borrowers with lenders that offer flexible programs, and data shows brokers approve 78% of self-employed applicants compared to just 41% through traditional banks.

How much can I actually save by shopping for a mortgage online?

Tech-enabled mortgage shopping can save up to $44,000 over a 30-year loan, with even average shoppers saving around $9,000 by securing a rate just 11 basis points lower.

Are there risks in using AI or digital mortgage tools?

Yes. The main concerns are privacy and AI bias in automated decisions. Stick with platforms that clearly disclose their data practices and use licensed, compliant professionals to manage your application.