Most borrowers sign their mortgage paperwork without ever comparing a second offer. That single decision can cost thousands of dollars over the life of the loan. Freddie Mac research shows that getting just two extra quotes saves around $600, and five quotes can push savings past $1,200. This article walks you through exactly how loan shopping works, why the type of lender you choose matters just as much as the rate you see, and the practical steps you can take right now to stop leaving money on the table.

Table of Contents

- What is loan shopping and why it matters

- Step-by-step: How to shop for mortgage loans

- Retail lenders vs. wholesale mortgage brokers: Key differences

- Who benefits most: Factors influencing loan shopping success

- Is loan shopping always worth it? When and how it pays off

- Next steps: Find your best mortgage with expert help

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| More quotes, more savings | Comparing 3-5 mortgage offers can save you up to $1,200 or more over the life of your loan. |

| Wholesale brokers offer choices | Wholesale mortgage brokers provide access to a wider range of rates and products, benefiting many borrowers. |

| Same-day comparisons matter | Getting quotes from lenders simultaneously allows for more accurate, apples-to-apples analysis. |

| APR reveals real cost | Focusing on APR instead of just interest rate ensures you understand the true financial impact of each loan. |

| Not shopping has real costs | Most borrowers who don’t shop lose out on hundreds or thousands in yearly savings. |

What is loan shopping and why it matters

Loan shopping means comparing mortgage offers from multiple lenders before committing to one. It sounds obvious, but most borrowers skip it entirely, with roughly 70% never requesting a second quote and missing out on $1,000 or more per year in potential savings. The process is simpler than most people expect, and the payoff is real.

Why do so many people skip it? A few common reasons:

- They assume all lenders offer similar rates

- They feel overwhelmed by the paperwork

- They trust their bank without questioning its pricing

- They worry that multiple applications will hurt their credit score

None of these reasons hold up under scrutiny. Empirical data from Freddie Mac and the Philadelphia Fed shows that getting four quotes can save between $600 and $1,200 per year, and that even one extra quote lowers rates by an average of 28 basis points for lower-income borrowers. Wholesale lending now accounts for 26% of all originations in 2025, up from 19% in 2020, which tells you that more borrowers are waking up to the value of shopping.

One thing many borrowers overlook: the difference between interest rate and APR. The interest rate is just the cost of borrowing. APR, or annual percentage rate, folds in lender fees, origination charges, and other costs. When you compare mortgage rates across lenders, always use APR as your benchmark. A loan with a lower rate but higher fees can easily cost more than one with a slightly higher rate and no fees.

"Shopping for a mortgage is one of the highest-return financial moves a homebuyer can make. The time investment is small. The savings are not."

Understanding why compare lenders matters is the first step. The next is knowing exactly how to do it.

Step-by-step: How to shop for mortgage loans

Shopping for a mortgage does not have to take weeks. Here is a clear process that works:

- Pull your financials together. Gather your last two years of tax returns, recent pay stubs, bank statements, and your credit score. Lenders need this to give you accurate quotes.

- Set your loan parameters. Know your target purchase price, down payment amount, and preferred loan term. This keeps every quote on the same footing.

- Request quotes from at least three to five lenders. Include both retail lenders and at least one wholesale mortgage broker. Multiple mortgage quotes give you real leverage in negotiations.

- Get all quotes on the same day. Rates move daily. Comparing a quote from Monday to one from Thursday is not a fair comparison.

- Compare APR, not just the rate. Look at the Loan Estimate form each lender provides. It standardizes the numbers so you can do a true apples-to-apples review.

- Ask the right questions. Use a checklist of questions for mortgage brokers to make sure you understand every fee and condition.

- Negotiate. Once you have competing offers, use them. Lenders will often match or beat a competitor's pricing when they know you are serious.

Pro Tip: If you are self-employed, an investor, or have a jumbo loan need, a wholesale broker is often your best starting point. Brokers access 50 or more lender options for jumbo loans alone, giving you far more flexibility than a single retail bank can offer. Borrowers with credit scores between 620 and 680 also tend to find better options through brokers.

One edge case worth noting: construction loans. For those, retail lenders often have more streamlined programs. Knowing which mortgage loan types fit your situation helps you target the right lender from the start.

Key stat: Borrowers who shop and compare save an average of 11 basis points on their rate. On a $400,000 loan, that is roughly $44 per month, or more than $500 per year.

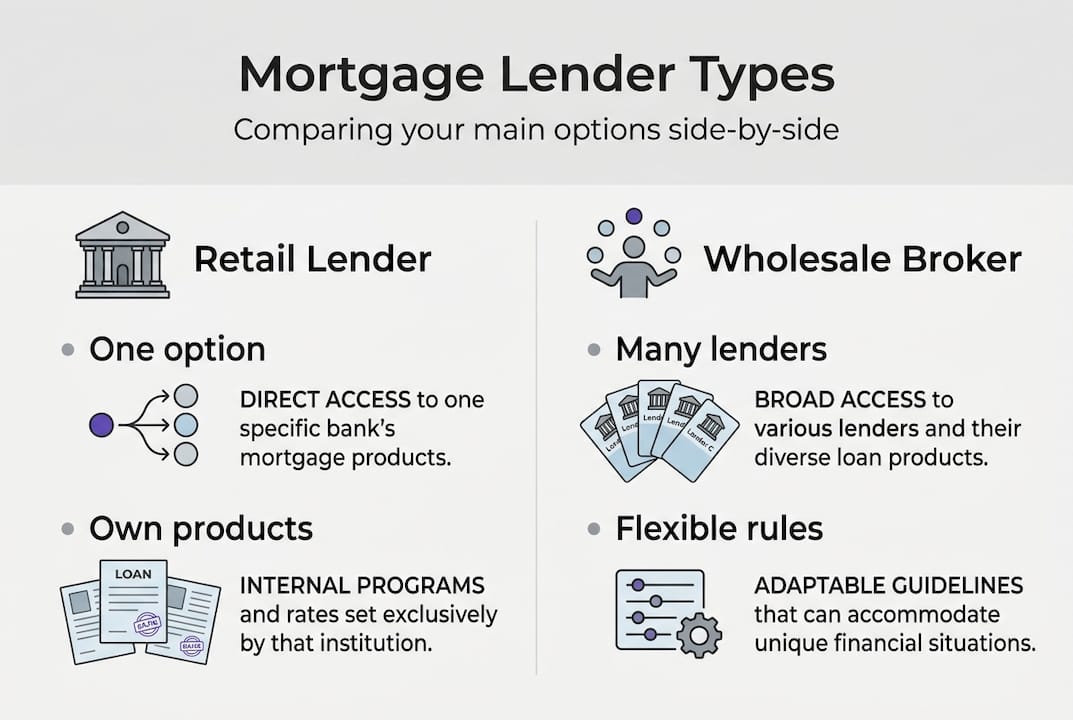

Retail lenders vs. wholesale mortgage brokers: Key differences

Once you know how to shop, the next question is which lender types to target. The distinction between retail and wholesale is one of the most important things a borrower can understand.

A retail lender is a bank, credit union, or direct lender that offers its own loan products at its own pricing. You get one menu. A wholesale mortgage broker works with dozens of lenders and shops your loan file across all of them to find the best fit. The broker does not set the rate. The lender does. But the broker's access to multiple lenders creates real competition.

| Feature | Retail lender | Wholesale broker |

|---|---|---|

| Lender options | One (their own) | Many (10 to 100+) |

| Rate competition | Limited | High |

| Best for | Simple, standard loans | Complex income, jumbo, credit challenges |

| Flexibility | Lower | Higher |

| Market share (2025) | Majority | 26% and growing |

Wholesale brokers shine in situations where your financial profile does not fit a cookie-cutter mold. Self-employed borrowers, real estate investors, and buyers with non-traditional income all benefit from a broker's wider network. For shopping mortgage lenders effectively, including a broker in your comparison is almost always worth it.

That said, retail lenders are not always the wrong choice. If you have a straightforward W-2 income, strong credit, and a conventional loan amount, a retail lender may move faster and with less friction. The key is not to default to one type without comparing. Access to competitive mortgage rates often comes from putting both types in direct competition with each other.

Who benefits most: Factors influencing loan shopping success

Not every borrower sees the same results from shopping. Research shows clear patterns in who gains the most.

Borrowers who tend to save the most:

- Urban buyers with access to more lenders and fintech platforms

- Creditworthy borrowers who qualify for a wider range of products

- Buyers using simultaneous search, meaning they request all quotes at once rather than sequentially

- Tech-comfortable borrowers who use online platforms to compare offers quickly

Empirical research also shows that minority borrowers and lower-income buyers shop less frequently, which means they miss out on savings at a higher rate. Fintech platforms are starting to close that gap by making the process faster and more accessible.

Pro Tip: Simultaneous searching, where you request quotes from multiple lenders at the same time rather than one at a time, is the most effective strategy. It keeps all offers current and gives you real negotiating power. Sequential shopping, where you go to one lender, wait, then try another, wastes time and makes comparisons harder.

Mortgage rate transparency is improving, but it still requires effort on your part. The borrowers who take that extra step consistently end up with lower mortgage rates than those who accept the first offer they receive.

Is loan shopping always worth it? When and how it pays off

Loan shopping delivers the biggest returns in specific situations. Here is a breakdown:

| Loan scenario | Shopping impact | Best approach |

|---|---|---|

| High loan amount (jumbo) | Very high | Wholesale broker first |

| Self-employed or complex income | Very high | Wholesale broker |

| Credit score 620 to 680 | High | Broker plus retail comparison |

| Standard W-2, conventional loan | Moderate | Retail plus one broker quote |

| Construction loan | Lower | Retail lender focus |

| Refinance | High | Same-day quotes, avoid blended rate traps |

One refinance pitfall worth calling out: the blended rate trap. Some lenders present a refinance offer that blends your existing rate with a new one, making the deal look better than it is. Always calculate the true new rate on the full balance. Refinance tips from experienced brokers can help you spot this quickly.

"The borrowers who save the most are not necessarily the ones with the best credit. They are the ones who asked for more than one quote."

For a full view of what is available to you, reviewing your loan options before you start shopping gives you a clearer picture of where you stand and what to ask for.

Next steps: Find your best mortgage with expert help

You now know that loan shopping is not complicated. It is a process, and the right tools make it faster. At LoFiRate.com, we connect you directly with licensed wholesale mortgage brokers in your state who can shop multiple lenders on your behalf. You get real competition working in your favor, not just one bank's pricing.

Whether you are buying your first home or refinancing an existing loan, exploring your mortgage broker matching options takes minutes and costs nothing. There is no obligation, no pressure, and no guesswork. Browse available loan options and request a free consultation to see what wholesale access can do for your rate. The savings are real. The process is simple. The only question is whether you are ready to stop overpaying.

Frequently asked questions

How many loan quotes should I get when shopping for a mortgage?

Most experts recommend comparing 3 to 5 quotes. Freddie Mac data shows that five quotes can save borrowers $1,200 or more over the life of the loan compared to accepting the first offer.

Does a mortgage broker always get you the lowest rate?

Not automatically, but brokers access far more lender options than a single retail bank. For complex income situations or jumbo loans, brokers consistently surface more competitive pricing than retail lenders alone.

Will loan shopping hurt my credit score?

No. Multiple mortgage inquiries made within a short window, typically 14 to 45 days, are treated as a single inquiry by credit bureaus, so your score takes minimal impact.

What's the difference between APR and interest rate when loan shopping?

The interest rate reflects only the cost of borrowing. APR includes fees and other charges, making it the more accurate number to compare when evaluating total loan cost across lenders.