TL;DR:

- Mortgage rate protection helps buyers lock in predictable mortgage costs during volatile markets. There are two main types: rate locks and float-down options, each suited to different risk tolerances. Timing and market signals are crucial for optimizing when to secure protection.

You found the home, signed the offer, and started counting down to closing day. Then the market shifted, and your expected mortgage payment jumped by hundreds of dollars before you even got the keys. This scenario plays out more often than most buyers expect. Mortgage rate protection is the tool that stands between you and that kind of financial surprise. It gives you a way to lock in a predictable cost while your loan moves through underwriting. This guide breaks down exactly what mortgage rate protection is, the different forms it takes, and how to decide which option fits your situation.

Table of Contents

- What is mortgage rate protection?

- Types of mortgage rate protection and how they work

- When should you secure mortgage rate protection?

- Benefits and potential drawbacks of mortgage rate protection

- Why most homebuyers underestimate mortgage rate protection

- Take the next step toward rate security

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Mortgage rate protection defined | It safeguards you against rising interest rates during the homebuying process. |

| Main options: lock and float-down | Rate locks and float-downs are the most common methods for securing your rate before closing. |

| Timing matters | You should consider securing protection as soon as you sign a purchase contract in a fluctuating market. |

| Weigh benefits and costs | Protection provides peace of mind but may include fees, especially for added flexibility like float-downs. |

What is mortgage rate protection?

Mortgage rate protection is any strategy or agreement that shields you from rising interest rates between the time you apply for a loan and the day you close. Think of it like a price guarantee at a store. If you reserve an item today at today's price, you pay that price even if the store raises it tomorrow.

In the mortgage world, what is a mortgage rate matters a great deal because even a small change can cost you thousands over the life of a loan. A rate that moves from 6.5% to 7.0% on a $400,000 loan adds roughly $130 to your monthly payment. Over 30 years, that is more than $46,000 in extra interest.

The concept matters most in a volatile market, where rates can shift week to week based on economic data, Federal Reserve decisions, and global events. Mortgage rate protection helps buyers avoid surprises from those market swings by establishing a ceiling on what you will pay.

Here are the main reasons buyers use mortgage rate protection:

- Budget certainty: You know your payment before closing day arrives

- Reduced stress: No need to watch rate headlines every morning

- Negotiating confidence: You can plan your finances without guessing

- Protection during delays: Appraisals, inspections, and title work take time, and rates can move during that window

Rate protection is not just for nervous buyers. Even experienced buyers and investors use it to eliminate one more variable from a transaction that already has plenty of moving parts.

Understanding mortgage compliance explained also helps here, because lenders are required to follow specific rules about how and when they disclose rate lock terms to you. Knowing your rights keeps you from being caught off guard by fine print.

Types of mortgage rate protection and how they work

With a clear definition in mind, let's look at the actual options lenders offer to protect your rate, and see how they compare.

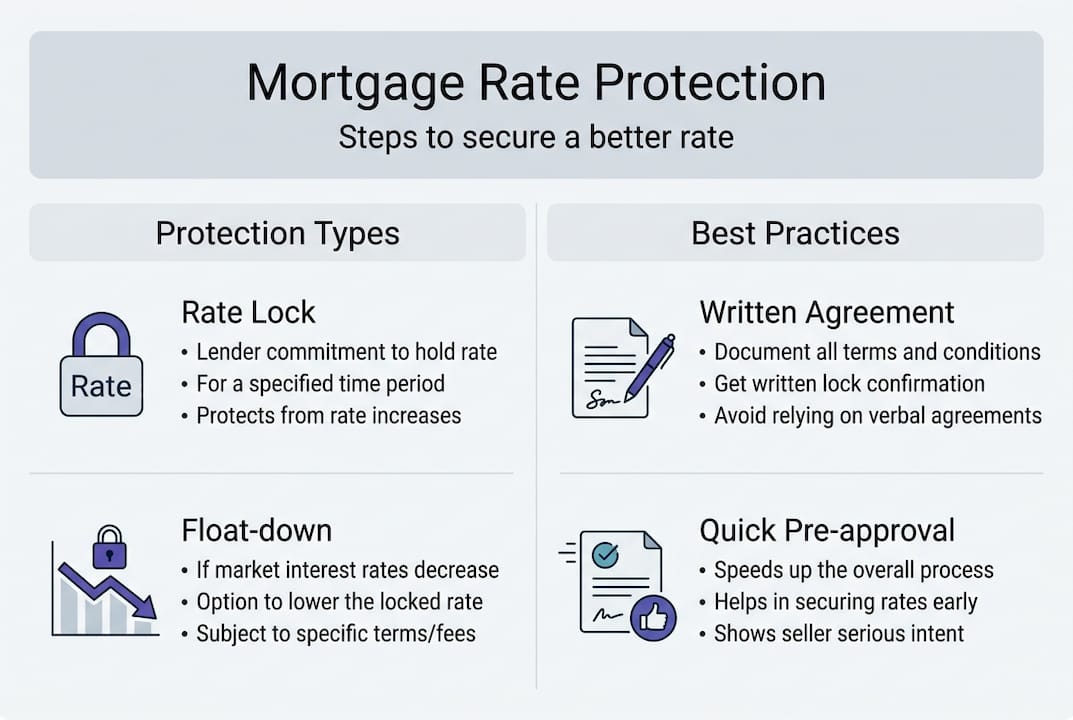

There are two primary forms of mortgage rate protection available to U.S. homebuyers: the rate lock and the float-down option. Each works differently, and the right choice depends on your timeline, your risk tolerance, and what you believe the market will do.

Rate lock: A rate lock is an agreement between you and your lender that freezes your interest rate for a set period, usually 30, 45, or 60 days. If rates rise during that window, you are not affected. If rates fall, you generally stay at your locked rate unless you negotiate otherwise.

Float-down option: A float-down is an add-on to a rate lock that allows you to take advantage of a lower rate if the market drops before closing. It offers the best of both worlds, but it typically comes with an extra fee or a slightly higher starting rate.

| Feature | Rate lock | Float-down option | No protection |

|---|---|---|---|

| Rate rises | You're protected | You're protected | You pay more |

| Rate drops | You keep locked rate | You may get lower rate | You benefit |

| Cost | Often free | Usually costs extra | No upfront cost |

| Best for | Stable or rising markets | Uncertain markets | Very short closings |

In 2026's volatile market, rate locks are especially valuable and float-downs offer extra flexibility, but may come at a cost. Here is how to choose:

- Assess your closing timeline. Longer timelines need longer lock periods, which may cost more.

- Check the fee structure. Ask your lender exactly what a float-down costs and what triggers it.

- Review market conditions. Look at market trends and mortgage rates before deciding.

- Compare across lenders. Exploring types of mortgage loans and lenders helps you find the most competitive lock terms.

Pro Tip: Always get your rate lock agreement in writing. Verbal confirmations are not binding, and you want a document that clearly states the locked rate, the expiration date, and any float-down terms.

Understanding how to use steps to secure the best rate alongside your protection strategy gives you the strongest possible position going into closing.

When should you secure mortgage rate protection?

Knowing your options, the next critical question is: when should you actually make your move to protect your rate?

Timing is everything. Lock too early and your protection may expire before closing. Lock too late and rates may have already moved against you. The sweet spot is usually right after your purchase contract is signed and your loan application is submitted.

Locking after signing a contract helps shield you from rate increases, but timing and fees should be assessed carefully. Here are the market signals worth watching before you decide:

- Federal Reserve meetings: When the Fed signals rate hikes, mortgage rates often follow within days

- Inflation reports: Higher-than-expected inflation data typically pushes rates up

- Jobs reports: Strong employment numbers can trigger rate increases

- Bond market movement: Mortgage rates track the 10-year Treasury yield closely

| Market signal | Rate impact | Recommended action |

|---|---|---|

| Fed rate hike announced | Rates likely rise | Lock immediately |

| Inflation data comes in high | Rates likely rise | Lock immediately |

| Economic slowdown signals | Rates may fall | Consider float-down |

| Stable economic data | Rates hold steady | Standard lock is fine |

Risks of waiting too long are real. If you delay locking because you expect rates to drop and they rise instead, you could face a significantly higher payment or even lose purchasing power on your budget. On the other hand, locking too early on a long closing timeline can mean your lock expires and you pay an extension fee.

Getting a mortgage pre-approval guide early in the process puts you in a stronger position to lock quickly once your contract is signed. Pre-approval also signals to lenders that you are a serious buyer, which can give you more leverage in negotiating lock terms.

Benefits and potential drawbacks of mortgage rate protection

So what are the real advantages and trade-offs? Let's break down what you gain and what to watch out for with mortgage rate protection.

The benefits are straightforward and significant. Rate protection gives you cost certainty, which makes budgeting far easier. You can calculate your monthly payment, plan your cash reserves, and avoid the anxiety of watching rate headlines every day. For buyers on tight budgets, this predictability is not a luxury. It is a necessity.

Key benefits of mortgage rate protection:

- Payment stability: Your rate is fixed, so your payment does not change before closing

- Peace of mind: You can focus on moving logistics instead of market news

- Budget accuracy: Lenders and financial planners can give you precise numbers

- Stronger offers: Sellers take buyers more seriously when financing is locked and predictable

But there are trade-offs worth knowing. Float-downs may add to loan costs, especially if market rates do not fall, so weigh the likelihood carefully before paying for that option. A standard rate lock is usually free or built into the loan pricing, but extended locks or float-down features carry fees that can range from 0.1% to 0.5% of the loan amount.

There are also situations where protection is less critical. If your closing is scheduled in under two weeks, a rate lock may not even be necessary. If you are refinancing and the timeline is flexible, you might be able to wait for a better rate window without much risk.

Pro Tip: When comparing mortgage rates across lenders, always ask about the rate lock policy as part of your comparison. Some lenders build lock fees into the rate itself, so the comparison is not always apples to apples.

Working with a broker who understands choosing the right lender can help you identify which lenders offer the most favorable lock terms without inflating your rate to cover the cost.

Why most homebuyers underestimate mortgage rate protection

Here is the uncomfortable truth: most buyers think about rate protection only after rates have already moved against them. That is too late.

Even savvy buyers fall into the trap of overconfidence. They watch rates for weeks, convince themselves the market is heading down, and decide to float without protection. Then a surprise inflation report or a Fed statement changes everything in 48 hours. Many buyers only think about rates after they spike, not realizing how a lock or float-down can save them thousands or provide peace of mind upfront.

The other common blind spot is cost perception. Buyers hear "fee" and assume protection is not worth it, without actually running the numbers. A float-down fee of $500 on a $350,000 loan is nothing compared to the cost of a rate that moves 0.25% in the wrong direction.

The fix is simple but requires action early. Talk to your broker about rate protection options before you even make an offer. Understand navigating mortgage compliance so you know what disclosures to expect. Make the decision based on data, not gut feelings about where rates are headed. The buyers who come out ahead are the ones who treat rate protection as a standard part of the process, not an afterthought.

Take the next step toward rate security

Understanding mortgage rate protection is one thing. Putting it into practice with the right support makes all the difference.

At LoFiRate.com, we connect you with licensed wholesale mortgage brokers who can walk you through your mortgage rate options and help you find the right protection strategy for your timeline and budget. Wholesale brokers shop multiple lenders, which means you get competitive pricing and honest guidance, not just one lender's standard offer. Whether you are exploring your first home purchase or refinancing an existing loan, you can review loan options and take control of your rate today. Get started at LoFi Rate and see how straightforward securing your mortgage rate can be.

Frequently asked questions

How long can you lock in a mortgage rate?

Most rate locks range from 30 to 60 days, but vary by lender. Extensions are sometimes available for an additional fee if your closing is delayed.

Is mortgage rate protection always worth the price?

The value of a rate lock or float-down depends on the likelihood of a rate movement and any associated fees. In a rising rate environment, protection almost always pays for itself.

What happens if rates drop after I lock in?

Float-downs let you benefit from a lower rate after locking, but may cost extra. Without a float-down, you keep your original locked rate regardless of market movement.

Can first-time buyers benefit from mortgage rate protection?

Rate protection helps shield new buyers from costly surprises. It provides the payment predictability that first-time buyers need most when navigating an already complex process.