Most homeowners assume going directly to a bank or lender guarantees the best refinance deal. That assumption can cost you thousands. Mortgage brokers access wholesale lenders and shop multiple rate options on your behalf, often securing rates 0.5-0.75% lower than retail channels. This article breaks down how brokers work, what they offer, and how to choose one that maximizes your savings. You'll learn the refinancing process step by step and discover why broker-guided refinancing often beats going solo.

Table of Contents

- Understanding the basics: What is refinancing and who are mortgage brokers?

- How brokers help you secure better refinance rates

- Brokers vs. direct lenders: Key differences and what matters for homeowners

- The refinance process with a mortgage broker: Step by step

- Choosing the right broker: What to look for and questions to ask

- Ready to refinance? Let LoFI Rate connect you to top brokers

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Brokers access lower rates | Mortgage brokers compare many lenders and often unlock wholesale refinancing rates unavailable directly to consumers. |

| Significant money savings | Using a broker can save you 0.5–0.75% on your new loan rate, amounting to thousands in savings. |

| Simplified refinance process | Brokers guide you step by step and handle complex paperwork to make refinancing stress-free. |

| Choose brokers wisely | The right broker should be transparent, highly rated, and focused on your financial interests. |

Understanding the basics: What is refinancing and who are mortgage brokers?

Refinancing is replacing your original mortgage with a new loan, often with better rates or terms. Homeowners refinance to lower monthly payments, shorten loan duration, or tap into home equity. It makes sense when current rates drop significantly below your existing rate or when your credit score improves enough to qualify for better terms.

Mortgage brokers are licensed professionals who connect borrowers with lenders. Unlike banks that offer only their own loan products, brokers work with multiple wholesale lenders to find competitive options. They handle paperwork, coordinate with underwriters, and negotiate on your behalf. This access to wholesale pricing often translates to lower rates than you'd find walking into a retail bank branch.

Many homeowners mistakenly believe brokers add unnecessary costs or complicate the process. In reality, brokers streamline refinancing by doing the rate shopping for you. They're compensated by lenders or through disclosed borrower fees, and their incentive aligns with finding you a deal that closes successfully.

Key benefits brokers provide:

- Access to multiple lenders and loan products in one place

- Wholesale rate pricing unavailable to retail customers

- Expert guidance through complex paperwork and underwriting

- Negotiation leverage that individual borrowers lack

- Time savings from consolidated rate shopping

"Brokers eliminate the guesswork by presenting vetted options tailored to your financial profile, saving you weeks of research and comparison."

How brokers help you secure better refinance rates

Brokers tap into wholesale lender networks that don't advertise directly to consumers. While a retail bank offers only its own rates, a broker compares offerings from 10, 20, or more lenders simultaneously. This competition drives rates down and gives you leverage.

Wholesale lenders price loans lower because they avoid the overhead of retail branches and marketing campaigns. Brokers pass these savings to you. The difference might seem small, but saving 0.75% on your rate can mean tens of thousands of dollars over a 30-year mortgage.

Consider a $300,000 refinance. At 6.5%, your monthly payment is roughly $1,896. Drop that rate to 5.75% through a broker, and your payment falls to $1,751. That's $145 monthly or $52,200 over the loan's life. Brokers make this possible by shopping aggressively and leveraging relationships with lenders who compete for their business.

Pro Tip: Ask brokers how many lenders they work with and whether they receive higher compensation from certain lenders. Transparency here ensures they're prioritizing your savings, not their commission.

| Scenario | Retail Lender Rate | Broker Rate | Monthly Savings | 30-Year Savings |

|---|---|---|---|---|

| $300,000 loan | 6.5% | 5.75% | $145 | $52,200 |

| $400,000 loan | 6.5% | 5.75% | $193 | $69,480 |

| $500,000 loan | 6.5% | 5.75% | $241 | $86,760 |

Brokers also help you get lower mortgage rates by identifying programs you might not know exist, like state-specific assistance or lender credits. Their expertise turns rate shopping from a confusing chore into a streamlined process. For refinance tips that save money, brokers are your best resource.

Understanding why comparing lending options matters becomes clear when you see the rate spread brokers uncover. One lender might quote 6.25% while another offers 5.5% for the same borrower profile. Brokers surface these gaps instantly.

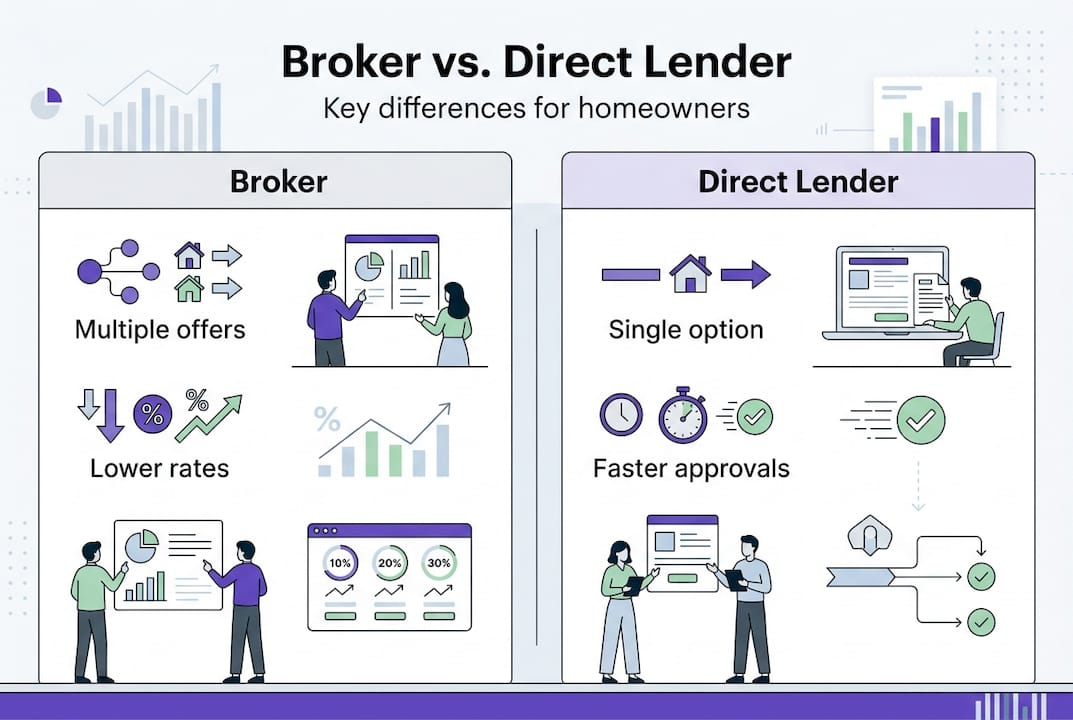

Brokers vs. direct lenders: Key differences and what matters for homeowners

Choosing between a broker and a direct lender depends on your priorities. Direct lenders offer simplicity: one application, one decision. Brokers offer choice: multiple lenders competing for your business. If you value convenience and have a strong existing bank relationship, a direct lender might suffice. If you want the absolute best rate and terms, brokers win.

Direct lenders control the entire process internally, which can speed up approvals. However, you're limited to their rate sheet and underwriting guidelines. If your financial situation is complex, a direct lender might decline you even though another lender would approve. Brokers solve this by matching you with lenders whose criteria fit your profile.

Comparing lenders can save homeowners thousands because rate differences compound over time. A broker's ability to shop 20 lenders in the time it takes you to apply with one is invaluable. You avoid the credit score dings from multiple applications since brokers submit to lenders on your behalf.

| Feature | Mortgage Broker | Direct Lender |

|---|---|---|

| Lender options | 10-30+ wholesale lenders | 1 lender (themselves) |

| Rate access | Wholesale pricing | Retail pricing |

| Loan variety | Extensive product range | Limited to their offerings |

| Personalized service | High touch, advisory role | Varies by institution |

| Approval speed | Depends on chosen lender | Often faster internally |

| Cost transparency | Disclosed fees | Sometimes hidden in rate |

When to choose a broker:

- You want the lowest possible rate and are willing to compare options

- Your financial situation is unique or slightly outside standard guidelines

- You lack time to research and apply with multiple lenders

- You value expert guidance through the refinancing process

- You're refinancing a non-standard property or loan type

When a direct lender might work:

- You have an excellent existing relationship with a bank offering competitive rates

- Your financial profile is straightforward and strong

- You prioritize speed and simplicity over rate optimization

- You've already shopped rates and confirmed the lender is competitive

For most homeowners, asking the right questions to mortgage brokers reveals whether they'll deliver better value than going direct. Brokers earn their keep by uncovering savings you'd miss on your own.

The refinance process with a mortgage broker: Step by step

Refinancing through a broker follows a clear workflow designed to maximize your savings while minimizing hassle. Here's what to expect:

-

Initial consultation: You discuss your goals, current mortgage, and financial situation. The broker assesses whether refinancing makes sense and estimates potential savings.

-

Pre-qualification: The broker pulls your credit and reviews income documentation to determine which lenders and loan products you qualify for.

-

Rate shopping: The broker submits your profile to multiple wholesale lenders and collects rate quotes. This happens quickly, often within 24-48 hours.

-

Loan comparison: You review options side by side. The broker explains trade-offs between rates, fees, and loan terms so you can make an informed choice.

-

Application submission: Once you select a lender, the broker submits your full application and coordinates document collection.

-

Underwriting: The lender reviews your financials, orders an appraisal, and verifies employment. The broker troubleshoots any issues that arise.

-

Closing: You sign final documents, and the new loan pays off your existing mortgage. The broker ensures all details are correct before closing.

Each step in the broker-guided process ensures you access and compare leading offers without juggling multiple lender relationships yourself. Brokers manage timelines, chase down paperwork, and keep everyone on track.

Pro Tip: Keep all required documents handy for faster approval. This includes recent pay stubs, tax returns, bank statements, and your current mortgage statement. Organized borrowers close weeks faster.

You maintain control at every decision point. The broker presents options, but you choose the lender and loan terms. If something feels off, you can pause or switch directions. This flexibility, combined with expert guidance, makes broker-assisted refinancing less stressful than going solo.

Understanding mortgage qualification requirements before starting helps you gather the right documents upfront. Brokers often provide checklists tailored to your situation, streamlining the entire process.

Choosing the right broker: What to look for and questions to ask

Not all brokers deliver equal value. The right broker saves you money and provides transparent, ethical service. The wrong one might steer you toward loans that benefit their commission over your savings. Here's how to separate the two.

Start by verifying licensing. Every state requires mortgage brokers to hold active licenses. Check your state's regulatory database to confirm the broker is in good standing with no disciplinary actions. Experience matters too. Brokers who've closed hundreds of loans understand lender quirks and underwriting nuances that newer brokers miss.

Transparency about compensation is non-negotiable. Ask how the broker gets paid and whether certain lenders offer higher commissions. The right broker helps you navigate options and find better deals without hidden agendas. If a broker hesitates to explain their fee structure, walk away.

Five smart questions to ask any broker:

- How many wholesale lenders do you work with, and can you show me a list?

- What are your fees, and are they negotiable or included in the loan?

- Can you provide references from recent refinance clients?

- How do you handle situations where my application is denied by one lender?

- What's your average time from application to closing?

Red flags to watch for:

- Pressure to lock a rate immediately without time to compare

- Vague answers about fees or lender relationships

- Promises of rates that seem too good to be true

- Lack of communication or missed deadlines

- No online reviews or verifiable track record

Positive signals:

- Detailed written estimates with all costs disclosed

- Willingness to explain loan options without jargon

- Proactive communication and responsiveness

- Strong online reviews and referrals from trusted sources

- Membership in professional organizations like NAMB

"A trustworthy broker educates you on trade-offs, respects your timeline, and prioritizes your long-term financial health over a quick commission."

Understanding what mortgage brokers do helps you evaluate whether a specific broker is delivering on their role. Great brokers act as advisors, not salespeople. They answer questions patiently, provide multiple scenarios, and never rush your decision.

Interview at least two brokers before committing. Compare their rate quotes, fee structures, and communication styles. The broker who takes time to understand your goals and explains options clearly is usually the best choice. Trust your instincts. If something feels off, keep looking.

Ready to refinance? Let LoFI Rate connect you to top brokers

You now understand how brokers unlock lower refinance rates and guide you through the process. The next step is connecting with a licensed broker who can shop wholesale lenders on your behalf. LoFI Rate specializes in matching homeowners with experienced brokers who prioritize your savings and provide transparent, no-obligation consultations.

Whether you're looking to lower your monthly payment, shorten your loan term, or tap into home equity, LoFI Rate's broker matching services connect you with professionals who have access to competitive wholesale pricing. Explore refinance loan options tailored to your financial situation and discover how much you could save. Getting started takes minutes, and there's no commitment until you find a rate and terms that work for you.

Don't leave money on the table by accepting the first rate you're quoted. Let LoFI Rate help you access low mortgage rates through brokers who compete for your business. Request your free consultation today and take control of your refinancing journey with confidence.

Frequently asked questions

What does a mortgage broker do during refinancing?

A broker shops multiple lenders to find the best rates and terms for your refinance while handling most of the paperwork. Brokers search for competitive rates among wholesale lenders on your behalf, saving you time and money.

How much can using a broker save on mortgage refinancing?

Many homeowners save up to 0.75% on rates by working with brokers instead of going directly to lenders. On a $300,000 loan, that's over $50,000 in interest savings over 30 years.

How do brokers get paid for refinance transactions?

Brokers usually receive compensation from lenders after closing or sometimes charge a small fee to the borrower, always disclosed up front. Broker compensation comes from either source and must be transparent.

Do I have to pay extra fees when working with a broker?

Sometimes a broker fee applies, but the overall savings from lower rates usually offset the cost. Broker fees may apply but are often outweighed by interest savings over the loan term.

Can I refinance with bad credit using a broker?

Brokers have access to lenders with varied credit requirements, increasing your chances of approval even with lower scores. They match your profile to lenders most likely to approve your application, though rates may be higher with damaged credit.