TL;DR:

- A good faith estimate is a written document that itemizes expected mortgage costs, helping homebuyers compare offers before closing. It is not a binding contract, but certain fees cannot increase at closing, and it must be provided within three days of application. Using GFEs critically enables borrowers to identify fair fees, negotiate effectively, and avoid surprises at closing.

A good faith estimate (GFE) is a written document that itemizes the expected costs of a mortgage loan, giving homebuyers a clear picture of what they will pay before closing. The GFE was the standard disclosure form required under the Real Estate Settlement Procedures Act (RESPA) for most residential mortgage applications. Its core purpose is consumer protection: it forces lenders to show their hand early, so you can compare offers on equal footing rather than discovering fees at the closing table. Understanding the good faith estimate meaning puts you in control of one of the largest financial decisions of your life.

What is a good faith estimate and what does it include?

A good faith estimate breaks down every anticipated cost tied to your mortgage, from lender fees to third-party charges. Knowing what each line item represents helps you spot inflated costs and negotiate before you sign anything.

Common components found on a GFE include:

- Origination fee: The lender's charge for processing your loan, typically expressed as a percentage of the loan amount. This is one of the most negotiable fees on the document.

- Appraisal fee: Paid to a licensed appraiser to confirm the property's market value. The lender orders this, but you pay for it.

- Title insurance: Protects both you and the lender against ownership disputes. Lender's title insurance is usually required; owner's title insurance is optional but strongly recommended.

- Escrow deposits: Upfront funds collected to prepay property taxes and homeowner's insurance. These are not fees. They are your own money held in reserve.

- Credit report fee: A small charge for pulling your credit history during underwriting.

- Prepaid interest: Interest that accrues between your closing date and the end of that month.

Each of these charges tells a story. Origination fees reveal how much the lender profits directly from your loan. Title and escrow costs show which third-party vendors the lender prefers. When you spot hidden mortgage fees early, you have real leverage to push back or walk away.

Pro Tip: Request GFEs from at least three lenders on the same day. Rates and fees shift daily, so same-day comparisons give you an accurate apples-to-apples picture.

The itemized structure is the GFE's greatest strength. A lender quoting a low interest rate but charging $4,000 in origination fees may cost you more than a lender with a slightly higher rate and $800 in fees. The GFE forces that comparison into the open.

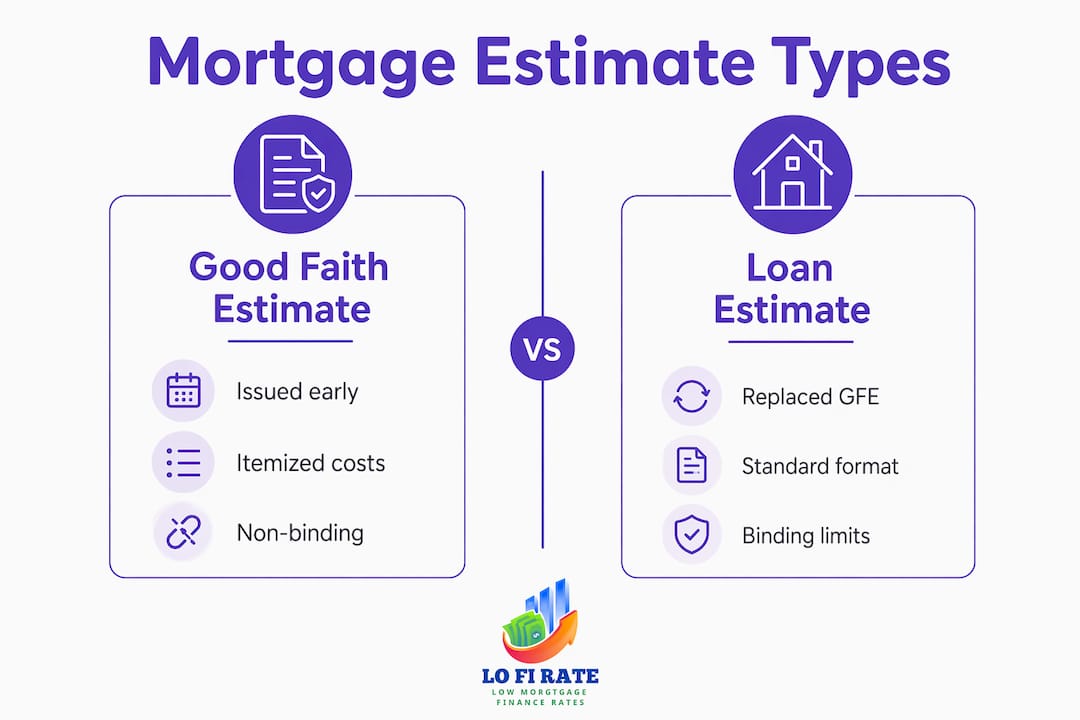

How does a good faith estimate differ from a loan estimate and a closing disclosure?

The GFE, the Loan Estimate, and the Closing Disclosure are three separate documents that serve different purposes at different stages of the mortgage process. Confusing them is one of the most common mistakes homebuyers make.

In 2015, the Consumer Financial Protection Bureau (CFPB) replaced the GFE with the Loan Estimate for most residential mortgages under the TRID rule (TILA-RESPA Integrated Disclosure). The Loan Estimate uses a standardized three-page format and must be delivered within three business days of your loan application. The GFE still applies in certain contexts, including some reverse mortgages and loans not covered by TRID.

| Document | When you receive it | Purpose | Binding? |

|---|---|---|---|

| Good Faith Estimate | Within 3 business days of application (pre-2015 loans or reverse mortgages) | Itemizes estimated loan costs | No, it is an estimate |

| Loan Estimate | Within 3 business days of application (most loans post-2015) | Standardized cost breakdown | Partially, some fees cannot increase |

| Closing Disclosure | At least 3 business days before closing | Shows final, actual loan costs | Yes, these are the real numbers |

The Closing Disclosure is the document that matters most at the finish line. It locks in the actual figures you will pay. Comparing your Loan Estimate or GFE side by side with the Closing Disclosure is the single best way to catch last-minute fee increases.

What are the legal requirements for providing a good faith estimate?

RESPA governs the GFE requirement for federally related mortgage loans. The law exists to prevent lenders from hiding costs or springing fees on borrowers at the last moment.

The key legal obligations lenders must meet include:

- Delivery timing: Lenders must provide the GFE within three business days of receiving a completed loan application. Waiting longer is a RESPA violation.

- Accuracy standards: Certain fees on the GFE cannot increase at closing. Origination charges, for example, are locked once disclosed. Third-party fees may increase, but only within defined tolerance limits.

- Written format: Verbal quotes carry no legal weight. A written GFE is the only document that creates a baseline for dispute. Written documentation is the only reliable protection against surprise charges.

- Dispute rights: If final costs exceed the GFE beyond allowable tolerances, the lender may be required to reimburse the difference. The written estimate is the legal baseline that makes this possible.

Lenders who fail to deliver accurate, timely GFEs face regulatory penalties and potential liability to the borrower. That legal pressure is exactly why the GFE exists: it aligns the lender's incentives with yours.

Pro Tip: Keep every version of your GFE or Loan Estimate. If a lender revises the document, ask specifically what changed and why. Unexplained increases in origination fees are a red flag.

The GFE regulatory framework also requires that the document use plain language and a standardized format. That standardization is what makes comparison shopping possible. Without it, lenders could bury fees in fine print or use different labels for the same charges.

How can homebuyers use good faith estimates to compare mortgage offers?

The GFE is most powerful when you treat it as a shopping tool, not just a disclosure form. Most homebuyers focus on the interest rate. The rate matters, but total loan costs over the life of the loan matter more.

Here is how to use the GFE effectively:

- Compare total estimated settlement charges, not just rates. The bottom-line number on the GFE reflects what you will actually pay to close the loan. A lower rate with high fees can cost more than a higher rate with minimal fees, depending on how long you keep the loan.

- Check which fees are fixed versus variable. Origination charges are locked. Third-party fees like title insurance can vary by provider. Ask if you can shop for your own title company.

- Question every fee you do not recognize. "Administrative fee," "processing fee," and "underwriting fee" can mean different things at different lenders. Ask for a plain-language explanation of each charge.

- Request an updated GFE if your loan terms change. If you lock a rate, switch loan programs, or change your down payment, the lender must issue a revised estimate.

- Watch for fees that appear after the initial GFE. Legitimate lenders do not add new charges late in the process. New fees appearing close to closing deserve a direct explanation.

Understanding property financing transparency is a skill that pays off at every stage of the homebuying process. The GFE gives you the raw data. Your job is to read it critically.

Pro Tip: Use a simple spreadsheet to line up GFEs from multiple lenders row by row. Identical fee categories make discrepancies obvious in seconds.

What limitations should borrowers know about good faith estimates?

A GFE is an estimate, not a contract. Final costs at closing can differ from what the document shows, and homebuyers who treat the GFE as a guaranteed price often feel blindsided.

Key limitations to understand:

- Estimates are not guarantees. The GFE reflects the lender's best projection at the time of application. Market conditions, property issues, or underwriting findings can change the final numbers.

- Third-party fees can increase. Charges from title companies, appraisers, and attorneys are not fully controlled by the lender. These fees carry wider tolerance limits and can rise between the GFE and closing.

- Co-provider fees may be missing. A single GFE can omit fees from additional service providers involved in your transaction. Missing co-provider fees are a common source of closing-day surprises. Always ask whether all expected charges are included.

- GFEs do not apply to every loan type. Certain loan products and transaction types fall outside standard GFE requirements. If you are unsure whether your loan requires a GFE, ask your lender directly.

- Verbal quotes are not enforceable. A lender who quotes you a fee over the phone has made no legal commitment. Only the written document creates a baseline for any dispute.

The gap between estimate and final cost is where borrowers lose money. Knowing these limitations in advance lets you ask the right questions before you reach the closing table.

Key Takeaways

A good faith estimate is a legally required written disclosure that itemizes projected mortgage costs, giving homebuyers the information they need to compare lenders and avoid surprise fees at closing.

| Point | Details |

|---|---|

| GFE definition | A written, itemized projection of expected mortgage costs required under RESPA. |

| Replaced by Loan Estimate | For most loans after 2015, the Loan Estimate replaced the GFE under the CFPB's TRID rule. |

| Not a guarantee | Final closing costs can differ from GFE amounts; only the Closing Disclosure shows actual charges. |

| Compare total costs | Evaluate total estimated settlement charges across lenders, not just the interest rate. |

| Get it in writing | Verbal quotes carry no legal weight; only a written GFE creates dispute protection. |

What I have learned from watching homebuyers read their GFEs

Most homebuyers I have seen go through the mortgage process make the same mistake: they flip straight to the interest rate and ignore the fee section entirely. That habit costs real money. A lender charging $3,000 more in origination fees than a competitor is essentially offering a worse deal, even if the rate looks identical on paper.

The other pattern I notice is that homebuyers treat the GFE as a formality rather than a negotiating tool. Fees are not fixed in stone. Lenders expect informed borrowers to push back. When you ask a lender to explain a $500 "administrative fee" in plain terms, you often find it disappears or shrinks. That only happens if you read the document carefully enough to ask the question.

The shift from the GFE to the Loan Estimate in 2015 made comparison shopping easier. The standardized format means you can line up two Loan Estimates and compare them line by line in minutes. But the underlying principle has not changed: the written estimate is your best protection, and reading it critically is the most valuable thing you can do before you commit to a loan.

My honest advice is this: never let a lender rush you past the estimate. You have a legal right to review it. Use that right.

— LoFi

How Lofirate helps you compare mortgage offers with confidence

Reading a GFE is only useful if you have multiple offers to compare. Most retail lenders show you only their own pricing, which means you have no baseline to judge whether the fees are fair.

Lofirate connects homebuyers and homeowners with licensed wholesale mortgage brokers who shop multiple lenders on your behalf. That means you get competing GFEs and Loan Estimates without filling out a dozen separate applications. Wholesale brokers have access to pricing that retail bank branches do not offer directly to consumers. If you want to see what your mortgage loan options actually look like across multiple lenders, Lofirate makes that comparison straightforward and obligation-free. Visit Lofirate to connect with a licensed broker in your state and get a second opinion on your current offer.

FAQ

What is the good faith estimate definition in mortgage lending?

A good faith estimate is a written document that itemizes the projected costs of a mortgage loan, required under RESPA for federally related mortgages. It gives borrowers a cost breakdown before they commit to a lender.

Is a good faith estimate binding on the lender?

A GFE is not a binding contract, but certain fees disclosed on it cannot increase at closing. Origination charges are locked, while third-party fees may change within defined tolerance limits.

What replaced the good faith estimate for most mortgages?

The Loan Estimate replaced the GFE for most residential mortgages in 2015 under the CFPB's TRID rule. The GFE still applies to some reverse mortgages and loans outside TRID coverage.

How do I read a good faith estimate effectively?

Focus on the total estimated settlement charges, not just the interest rate. Compare the same fee categories across multiple lenders and ask for plain-language explanations of any charge you do not recognize.

What happens if my final costs exceed the good faith estimate?

If final costs exceed the GFE beyond allowable tolerances, the lender may be required to cover the difference. Written estimates are the legal baseline that makes any dispute resolution possible.