TL;DR:

- The Closing Disclosure is a vital, legally required document that details your final mortgage terms and closing costs. Reviewing it carefully within the three-day window helps prevent costly errors, discrepancies, or surprises at closing time. Use this review period to verify all numbers, identify errors, and negotiate any necessary corrections before signing.

You're three days from closing on your new home, and a thick document lands in your email titled "Closing Disclosure." Most buyers scan it quickly, assume everything looks fine, and move on. That's a costly mistake. This document is arguably the most important piece of paper in your entire mortgage journey. A single overlooked line item can cost you hundreds or even thousands of dollars, and some errors are nearly impossible to fix after you've signed. This guide will walk you through exactly what the Closing Disclosure is, what to check, and how to protect yourself before you hand over that certified check.

Table of Contents

- What is a mortgage closing disclosure?

- When and why you receive the Closing Disclosure

- Key items to check on your Closing Disclosure

- What happens if your Closing Disclosure changes?

- Why the Closing Disclosure is your last line of defense

- The uncomfortable truth most homebuyers miss about Closing Disclosures

- Navigate your closing with confidence

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Final review tool | The Closing Disclosure lets you double-check your loan terms and costs before you sign anything. |

| Three-day rule | You must legally receive the Closing Disclosure at least three business days before your closing. |

| Spot and correct errors | Review every detail carefully as mistakes can cause costly delays or out-of-pocket expenses. |

| Compare with Loan Estimate | Use your initial Loan Estimate to make sure the final terms and numbers match or are explained. |

| Empower your decision | A careful review of your Closing Disclosure gives you the leverage to protect yourself and your investment. |

What is a mortgage closing disclosure?

The Closing Disclosure (CD) is a five-page federal form that shows you the final, locked-in terms and costs of your home loan. Think of it as the definitive contract summary before you sign everything official. According to current federal regulation, a "Closing Disclosure (CD) is a standardized document that shows the final terms of your mortgage and your closing costs," and it was created to remove guesswork from one of the biggest financial commitments most people ever make.

The CD is required under the Truth in Lending Act and RESPA Integrated Disclosure (TRID) rules, which went into effect in 2015. These rules combined two older documents into one clear form, giving buyers a single place to see everything about their loan. If you want a broader foundation of what these terms mean, this mortgage terminology guide breaks down the language in plain English.

Here's a quick breakdown of what each major section of the Closing Disclosure covers:

| Section | What it shows |

|---|---|

| Loan Terms | Loan amount, interest rate, monthly principal and interest, prepayment penalty, balloon payment |

| Projected Payments | Full estimated monthly payment, including taxes, insurance, and escrow |

| Costs at Closing | Itemized closing costs split between loan costs and other costs |

| Cash to Close | The exact dollar amount you need to bring to closing |

| Loan Disclosures | Assumptions, demand feature, negative amortization disclosures |

What makes the CD different from other mortgage documents you've already seen?

- It reflects final, locked numbers, not estimates

- It must match your earlier Loan Estimate within strict tolerances (some fees can't increase at all)

- It is legally required before you can complete closing

- It provides a direct comparison path between what was quoted and what you're actually paying

The CD is a critical piece of the consumer protection framework built into the modern mortgage process. It exists specifically because hidden fees and last-minute surprises were once common enough to harm millions of buyers.

When and why you receive the Closing Disclosure

The timing of your Closing Disclosure is not random, and it's not up to your lender's schedule. Federal law is specific: lenders must provide the Closing Disclosure at least three business days before your scheduled closing date. Those three days are your legal buffer, and they exist for one reason: to give you time to actually read the document.

Here's the standard timeline from Loan Estimate to closing:

- Loan application submitted — You apply and receive your initial Loan Estimate (LE) within three business days.

- Underwriting and processing — Your file is reviewed, appraisal is ordered, and conditions are cleared. An appraisal compliance guide can help you understand what happens during that process.

- Closing Disclosure issued — At least three business days before closing, your lender sends the CD.

- Three-day review window — You compare the CD to your LE, ask questions, and flag any issues.

- Closing day — If everything checks out, you sign and the loan funds.

The three-day rule is one of the strongest consumer protections in the homebuying process. It prevents the old industry practice of surprising buyers at the closing table with fees they hadn't anticipated. Getting familiar with mortgage compliance basics helps you understand why this protection matters so much.

Pro Tip: If you spot an error or something that doesn't match your Loan Estimate, contact your lender in writing immediately. Don't wait until closing day. Putting your concern in an email creates a paper trail and gives your lender time to issue a corrected CD if needed. Some corrections require a new three-day period, so acting fast protects your closing date.

Understanding the full mortgage qualification process and where the CD fits within it is essential if this is your first time buying a home. And if you're concerned about your homebuying compliance rights, you have more leverage than most buyers realize.

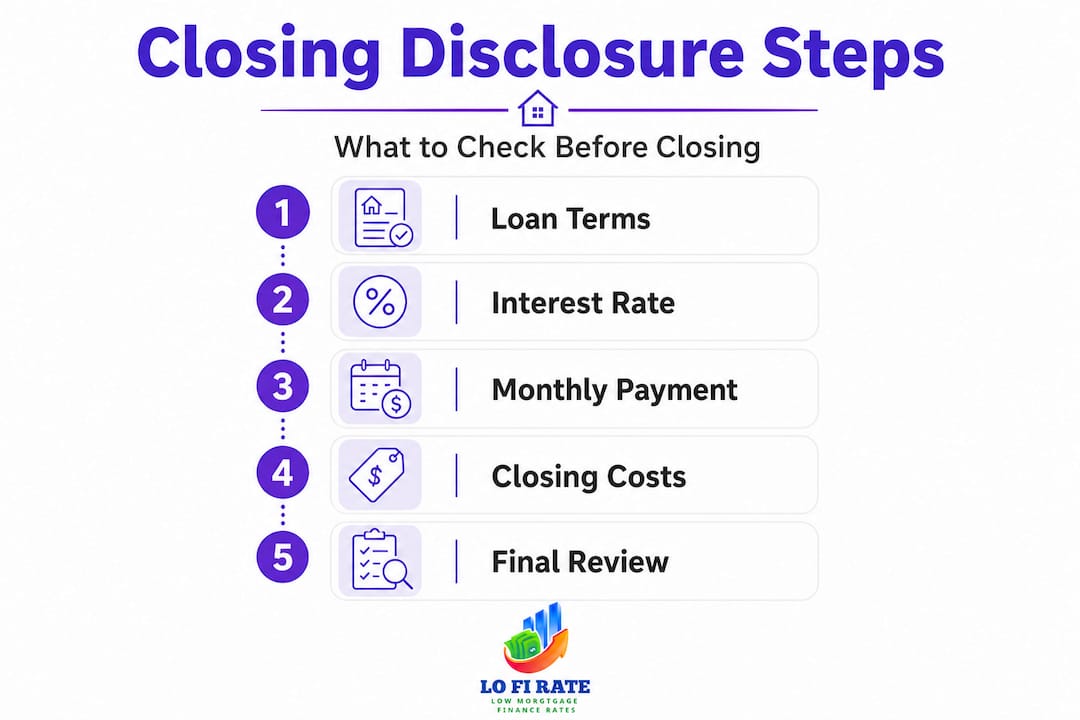

Key items to check on your Closing Disclosure

Your three-day window is not the time to relax. It's the time to work. Here's what to check, line by line. The CFPB recommends reviewing specific loan details including loan amount, loan type, interest rate, monthly payment, and whether there is a prepayment penalty, and comparing the APR with your original Loan Estimate.

Use this comparison table to match what you were quoted versus what you're being charged:

| Field | Loan Estimate (LE) | Closing Disclosure (CD) | Tolerance rule |

|---|---|---|---|

| Loan amount | Quoted | Final | Must match unless you changed the loan |

| Interest rate | Quoted (if locked) | Final | Must match if locked |

| APR | Estimated | Final | Cannot increase by more than 0.125% |

| Monthly payment | Estimated | Final | Should be very close |

| Origination charges | Itemized | Final | Cannot increase at all (0% tolerance) |

| Third-party services you chose | Estimated | Final | Can increase up to 10% |

| Prepayment penalty | Disclosed | Confirmed | Should match the LE |

Here are the red flags that most commonly trip up buyers:

- Origination fees that increased — These have a zero tolerance limit and should never go up from your LE

- Unfamiliar line items — Any fee that wasn't on your LE deserves a direct explanation

- Changed loan type or term — If you were quoted a 30-year fixed and the CD shows something different, stop everything

- Incorrect personal information — Wrong name spelling, wrong property address, or wrong Social Security Number can cause title issues

- APR increases beyond the allowed threshold — Even a small APR bump changes your total loan cost significantly

- Cash to close that doesn't match expectations — If the number is much higher than anticipated, find out why before closing day

Building your mortgage shopping knowledge beforehand makes the review process much faster because you'll already know what competitive pricing looks like. And understanding mortgage rate transparency helps you recognize when a fee or rate has quietly shifted in your lender's favor.

Pro Tip: Print both your Loan Estimate and your Closing Disclosure side by side. Use a yellow highlighter to mark every number you want to verify. Physically crossing each line off the list is far more reliable than scrolling through PDFs on a screen. Before your home appraisal is finalized, verify the appraised value shown on the CD matches the one in your loan file.

What happens if your Closing Disclosure changes?

Sometimes changes happen. The question is whether those changes require a new review period or not. Federal rules state that "if important terms change after you receive the initial Closing Disclosure, you may need a new (revised) Closing Disclosure and, in limited circumstances, another three-business-day review period." Not every change triggers a full reset, but the big ones do.

The three types of changes that always restart the three-day clock:

- APR increases by more than 0.125% — This signals a material change in the cost of your loan

- Loan product changes — Moving from a fixed-rate to an adjustable-rate mortgage (or vice versa)

- Addition of a prepayment penalty — Any new fee for paying off the loan early requires a fresh review

When a revised CD is issued, here's how the process flows:

- Something changes in your loan terms or costs

- Your lender prepares and sends a revised Closing Disclosure

- The new three-day clock begins from the date you receive the revised CD

- You review the revised document and compare it to the original

- Closing is rescheduled if the timing is affected

This is where understanding your mortgage contingency rights becomes particularly valuable. If your closing is delayed because of a revised CD, your purchase contract's contingency clauses may protect you from penalties.

"If important terms change after you receive the initial Closing Disclosure, you may need a new (revised) Closing Disclosure and, in limited circumstances, another three-business-day review period." — Consumer Financial Protection Bureau

Last-minute delays caused by revised CDs are frustrating but legal. The best way to prevent them is to make sure your rate is locked early, your loan type is confirmed in writing, and your lender has clearly disclosed all fees upfront. Communicate with your real estate agent and your closing attorney or title company so everyone is aligned if the timeline shifts.

Why the Closing Disclosure is your last line of defense

Once you sign at the closing table, the deal is done. There's no appeals process for a fee you missed, no easy way to recover from a wrong number you didn't catch, and no regulatory body standing by to issue you a refund. The CFPB recommends treating the Closing Disclosure as the "final exam" for the deal you're about to sign by comparing it line by line with your Loan Estimate and confirming the accuracy of the cash-to-close amount before closing day.

Here's a quick review checklist to use during your three-day window:

- Verify your full legal name and the property address on page one

- Confirm the loan amount matches what you agreed to in writing

- Check the interest rate is what was locked or last confirmed

- Scan the projected payments table to make sure nothing has been added to escrow without notice

- Review closing costs section A through H line by line

- Compare cash to close on the CD versus what your lender told you verbally or in writing

- Look for any fees labeled as "lender credits" and make sure they match your LE exactly

- Check the APR and confirm it falls within tolerance of your original estimate

If your mortgage origination process was handled smoothly, most of these numbers will match. But the ones that don't match are exactly why this checklist exists.

Pro Tip: Even the spelling of your name matters here. A name mismatch between your Closing Disclosure, your government-issued ID, and the title insurance policy can create delays on closing day or legal complications later. It takes two minutes to check and potentially hours to fix if you wait until you're sitting at the closing table.

The bottom line is that your home appraisal is done, your underwriting is approved, and your bags are packed for moving day. Don't let a skipped line item undo all of that preparation in the final stretch.

The uncomfortable truth most homebuyers miss about Closing Disclosures

Here's what years of watching the mortgage process have taught us: most buyers are completely exhausted by the time their Closing Disclosure arrives. They've fought through inspection negotiations, chased down bank statements, dealt with underwriting conditions, and coordinated moving trucks. By the time that PDF lands in their inbox, the emotional energy is gone. They scan it for a minute, assume the numbers "look about right," and move on.

That exhaustion is expensive.

We've seen buyers miss origination fee increases of $400, $600, even over $1,000 because they didn't compare their Closing Disclosure to their original Loan Estimate. That money is recoverable if you catch it before signing. After signing, it's gone. The sad part is that the three-day review period exists precisely for this situation, but most buyers treat it as a waiting room instead of a working room.

The Closing Disclosure is also, quietly, your last real negotiation moment. If you spot a fee that looks inflated or a credit that didn't show up, you can raise it. Lenders don't want delays either. They'd rather fix a line item than restart the clock. Most buyers don't realize they have that leverage because no one frames the CD as a negotiation document. It is one.

The bigger picture here connects to mortgage consumer protection broadly. The TRID rules, the three-day window, the tolerance thresholds on fees — all of it was built to protect you. But those protections only work if you actually use them. A regulation you don't activate is just a regulation. Use your review window. Slow down. Read every line. Ask every question. This is your home. The paperwork deserves the same attention as the open house.

Navigate your closing with confidence

Armed with what you now know about Closing Disclosures, here's how you can make your closing experience even better and more affordable.

Getting the best mortgage starts well before closing day. At LoFiRate.com, we help homebuyers and homeowners access competitive rates through licensed wholesale mortgage brokers who shop multiple lenders on your behalf. That means by the time your Closing Disclosure arrives, the numbers inside it should reflect genuinely competitive pricing, not inflated retail markups.

If you're still exploring your loan options or want a second opinion on whether your current lender is giving you the best deal, we make it easy to connect with a licensed broker in your state. Our broker matching service is no-obligation and transparent, built specifically to help buyers like you avoid overpaying. Closing confidently starts with the right loan from the beginning.

Frequently asked questions

What is the main purpose of a Closing Disclosure?

It clearly outlines your final loan terms and total closing costs, so you can review for errors and understand exactly what you're agreeing to before signing.

When must my lender provide the Closing Disclosure?

Your lender is required to give you the Closing Disclosure at least three business days before your closing date, giving you time to review it carefully.

What should I compare between my Loan Estimate and Closing Disclosure?

Focus on loan amount, interest rate, monthly payment, APR, points, credits, and closing costs. Make sure these fields match your Loan Estimate or that you fully understand any differences before signing.

Can my Closing Disclosure change after I receive it?

Yes. If important terms change, you may need a revised Closing Disclosure and perhaps another three-day review period, which can push your closing date back.

What if I find an error on my Closing Disclosure?

Contact your lender immediately in writing and ask for a correction. Even minor errors can cause delays at the closing table or create legal complications with your title after closing.