TL;DR:

- A rate lock is a lender's written commitment to hold your mortgage interest rate during a specified period, protecting you from market rate increases. It is best to lock after your offer acceptance and select a period covering your closing date plus buffer days to avoid delays. Most locks are free for 30 to 45 days, but longer periods incur fees, and comparing total lock packages prevents unexpected costs.

A rate lock is a written agreement between you and your lender that guarantees your mortgage interest rate will not increase during a specified period while your loan is processed and closed. This protection matters because mortgage rates can shift daily based on Federal Reserve policy, bond market movements, and broader economic data. Without a rate lock, the rate you see when you apply could be meaningfully higher by the time you reach closing. Understanding how rate locks work is one of the most practical steps any homebuyer can take to protect their budget.

What is a rate lock in a mortgage?

A mortgage rate lock is a lender's formal commitment to hold your quoted interest rate for a defined window of time, typically between 30 and 60 days. According to PNC, a rate lock protects you from rising interest rates by guaranteeing your current mortgage rate during the lock period until closing. That guarantee has real dollar value. On a $400,000 loan, a half-point rate increase translates to roughly $120 more per month and over $43,000 in additional interest across a 30-year term.

Rate locks are not automatic. U.S. Bank notes that locks typically become available after your loan is initially approved and while the loan is being finalized, commonly requiring an accepted purchase agreement. Most lenders will not allow you to lock a rate on a property you have not yet contracted to buy. This timing requirement means you need to move quickly once your offer is accepted.

The lock package itself is more than just a rate. Laurel Road explains that a rate lock package includes the interest rate, any discount points, the lock term length, and applicable fees, all of which affect total cost. Two lenders quoting the same rate on the same day can produce very different total costs depending on the points and fees bundled into the lock.

How does a mortgage rate lock work step by step?

The rate lock process follows a predictable sequence once you are under contract on a home. Here is how it typically unfolds:

- Submit your loan application. Your lender collects income documents, credit history, and property details. This is the foundation for your loan approval and the starting point for any rate discussion.

- Receive initial loan approval. Once the lender reviews your file and issues a conditional approval, you become eligible to lock. This usually happens within a few days to two weeks of application.

- Request the rate lock in writing. Ask your loan officer to lock your rate and confirm the lock in writing, including the rate, points, lock expiration date, and any associated fees. Verbal agreements are not sufficient.

- Underwriting reviews your file. During this phase, the lender verifies all documentation. Any significant changes to your loan details, such as a change in property type or loan amount, can affect the lock's validity.

- Close before the lock expires. Cadence Bank warns that a rate lock is a contract with deadlines. If your closing is delayed, you may need an extension, which can add fees or trigger repricing.

Most lenders provide free rate locks for 30 to 45 days. Longer locks, covering 60 days or more, can cost between 0.125% and 0.5% of the loan amount. That cost is worth calculating upfront if your closing timeline is uncertain.

Pro Tip: Ask your lender for the lock expiration date in writing on day one. Then count backward from your expected closing date and confirm the lock covers at least five extra business days as a buffer for last-minute delays.

What are the benefits and risks of locking your rate?

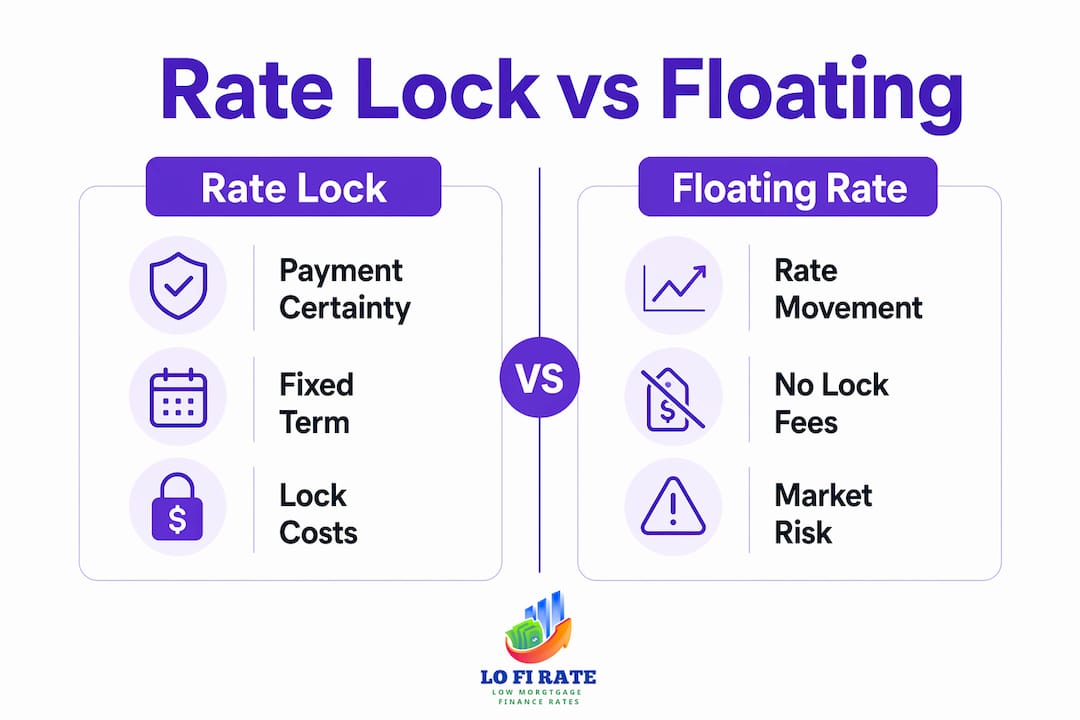

The primary benefit of a rate lock is payment certainty. Once locked, your principal and interest payment is fixed regardless of what happens in the broader market. This matters especially in volatile rate environments where mortgage rates can move 0.25% or more in a single week.

Rate locks also protect your buying power during processing. If rates rise after you lock, you keep the lower rate. If you are stretching your budget to qualify at a specific payment, a rate increase before closing could disqualify you entirely. The lock removes that risk.

The downsides are real but manageable:

- You may miss a rate drop. If rates fall after you lock, you are stuck at the higher rate unless you have a float-down option.

- Extensions cost money. If your closing is delayed, extending the lock can add fees. Cadence Bank confirms that extensions may alter cost and pricing, not just add a flat fee.

- Breaking the lock has consequences. You can walk away from a lock without a cancellation fee, but Better Mortgage notes that breaking a lock means losing the rate guarantee and may trigger lender-imposed waiting periods before you can re-lock on the same property.

"Many buyers use rate locks not to speculate on market movements but to manage risk and maintain focus on affordable payments after home contract acceptance." — U.S. Bank

This framing is worth internalizing. A rate lock is a risk management tool, not a bet on where rates are headed.

How do rate locks compare to floating your rate?

Floating your rate means you do not lock at application. Instead, you wait and hope rates move in your favor before closing. This approach can pay off in a declining rate environment, but it introduces real uncertainty into your monthly payment and qualification status.

| Feature | Rate lock | Floating the rate |

|---|---|---|

| Rate certainty | Guaranteed for lock period | Changes until closing |

| Protection from increases | Yes | No |

| Benefit from decreases | Only with float-down option | Yes |

| Cost | Free for 30-45 days; fees for longer | No upfront cost |

| Best for | Most buyers in stable or rising rate markets | Buyers in clearly declining rate environments |

Float-down options sit between these two choices. RefiGuide reports that float-down options typically cost 0.50% to 1% of the loan amount and include conditions that must be met before the lower rate applies. On a $350,000 loan, that is $1,750 to $3,500 for the option to capture a rate drop. Whether that cost is worth it depends on how much rates have moved and how much time remains before closing.

The meaningful comparison across lenders involves the entire lock package, not just the quoted rate. A lender offering 6.75% with zero points and a free 45-day lock may be a better deal than one offering 6.625% with one point and a 30-day lock that requires a paid extension.

Pro Tip: When comparing lenders, ask each one to quote the same scenario: rate, points, lock term, and fees. Then calculate the total cost of each package over your expected time in the home. The lowest rate is rarely the lowest cost.

When should you lock your mortgage rate?

Timing a rate lock well requires knowing your closing timeline and your own risk tolerance. Here is a practical framework for making the decision:

- Lock once you have an accepted offer. This is the most reliable trigger. You have a property, a contract, and a closing date. The uncertainty that made waiting reasonable is now gone.

- Choose a lock period that covers your closing date plus a buffer. Experts recommend locking for about 45 days when you are 30 to 40 days from closing. That buffer absorbs common delays like appraisal scheduling or title issues.

- Factor in your loan type. FHA and VA loans often take longer to process than conventional loans. If you are using a government-backed product, lean toward a 45 or 60-day lock rather than a 30-day lock.

- Assess the rate environment honestly. If rates have been rising for several weeks and your lender's forecast points upward, locking sooner reduces risk. If rates are clearly falling, a float-down option or a short delay may be worth considering.

- Confirm all loan details before locking. Changes to your loan amount, property type, or occupancy status after locking can invalidate the lock or require repricing. Review your mortgage shopping checklist before you commit.

One often-overlooked factor is lender processing speed. A lender that takes 45 days to close a loan is a riskier partner for a 30-day lock than one that consistently closes in 25 days. Ask your loan officer about average closing times before selecting your lock period.

For a deeper look at how rate protection fits into your overall loan strategy, the mortgage rate protection guide at Lofirate covers the full picture.

Key takeaways

A rate lock is the single most effective tool homebuyers have to protect their interest rate and monthly payment from market volatility between contract acceptance and closing.

| Point | Details |

|---|---|

| Rate lock definition | A written lender commitment that holds your interest rate for a set period during loan processing. |

| Optimal lock timing | Lock after your offer is accepted and choose a period that covers your closing date plus five extra days. |

| Lock package comparison | Compare rate, points, lock term, and fees together. The lowest rate is not always the lowest total cost. |

| Float-down option cost | Float-down options cost 0.50% to 1% of the loan amount and include conditions before the lower rate applies. |

| Breaking a lock | You can exit a lock without a cancellation fee, but you may face a waiting period before re-locking with the same lender. |

The part most buyers get wrong about rate locks

Most homebuyers treat a rate lock as a passive step, something the loan officer handles while they focus on packing boxes. That mindset costs money. The lock is a contract, and like any contract, the details matter more than the headline number.

What I have seen repeatedly is buyers who lock for 30 days because it is free, then face a two-week appraisal delay and end up paying an extension fee that wipes out the savings they thought they had locked in. The free lock is only free if your closing happens on time. Build the buffer in from day one.

The other mistake is treating the quoted rate as the only number that matters. Two lenders can quote identical rates on the same day with completely different lock packages. One charges a point to buy the rate down; the other does not. One offers a 45-day free lock; the other's free lock expires in 30 days. When you compare lenders, ask for the full lock package in writing before you decide. The fixed rate mortgage guide at Lofirate walks through how rate structures affect long-term cost, which is worth reading alongside any rate lock decision.

Rate locks are not about predicting the market. They are about removing one major variable from an already complex transaction. Lock the rate, confirm the expiration date, and focus on closing. That is the right approach for the vast majority of buyers.

— LoFi

Find the right rate lock through a wholesale broker

Retail lenders offer you one rate lock package from one lender. Wholesale mortgage brokers shop multiple lenders simultaneously, which means you can compare lock terms, points, and fees across several options before committing. Lofirate connects homebuyers and homeowners with licensed wholesale brokers in their state at no obligation. There is no cost to request a consultation, and brokers can often access pricing that retail channels do not publish. If you are approaching a rate lock decision and want to know whether your current lender's offer is competitive, explore your loan options through Lofirate before you sign the lock agreement.

FAQ

What is a rate lock in simple terms?

A rate lock is a lender's written promise to hold your mortgage interest rate at a specific level for a set number of days while your loan is processed. If market rates rise during that period, your locked rate stays the same.

How long does a mortgage rate lock last?

Most lenders offer free rate locks for 30 to 45 days. Longer lock periods of 60 days or more are available but typically cost between 0.125% and 0.5% of the loan amount.

Can you lose your rate lock?

Yes. Significant changes to your loan details after locking, such as a change in loan amount or property type, can invalidate the lock. Closing after the lock expiration date also voids the guarantee unless you pay for an extension.

What happens if rates drop after I lock?

You keep the locked rate unless you have a float-down option. Float-down options allow you to capture a lower rate after locking but typically cost 0.50% to 1% of the loan amount and include specific conditions.

When is the best time to lock a mortgage rate?

Lock your rate once you have an accepted purchase offer and a realistic closing timeline. Experts recommend a 45-day lock when you are 30 to 40 days from closing to absorb common delays without paying extension fees.