TL;DR:

- Rate sensitivity influences homeowners' decisions to sell or refinance based on current mortgage rates. The lock-in effect causes low-rate homeowners to stay put, reducing market supply and raising prices. Strategically evaluating thresholds and market signals helps homeowners act confidently without falling into paralysis.

If you've ever hesitated to sell your home because your current mortgage rate felt too good to give up, you already understand what is a rate-sensitive homeowner, even if you didn't have a name for it. Rate sensitivity isn't a personality trait. It's a financial condition that shapes when people buy, sell, and refinance. And right now, with mortgage rates staying elevated well above pandemic-era lows, millions of Americans are making major life decisions around a number on their loan statement.

Table of Contents

- Key takeaways

- What is a rate-sensitive homeowner?

- How rates affect refinancing decisions

- Rate sensitivity and buying power

- Strategies to manage rate sensitivity

- My honest take on rate sensitivity

- Ready to stop guessing and start comparing?

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Rate sensitivity defined | A rate-sensitive homeowner adjusts financial decisions based on how much rates have moved relative to their current mortgage. |

| The lock-in effect is real | Homeowners with sub-3% rates are financially penalized for selling, which shrinks housing supply and inflates prices. |

| Refinancing needs a threshold | A rate drop of at least 0.50% to 0.75% is typically required before refinancing saves more than it costs. |

| Buying power shrinks fast | A 0.5% rate increase on a $400,000 loan raises monthly payments by $130 to $150, pricing out thousands of buyers. |

| Strategy beats timing | Watching credit market signals and using break-even math produces better decisions than waiting for a perfect rate. |

What is a rate-sensitive homeowner?

A rate-sensitive homeowner is someone whose financial behavior changes meaningfully when mortgage interest rates shift. That behavior includes decisions about whether to sell, refinance, pull out equity, or hold still and wait. The sensitivity isn't about being financially fragile. It's about the math of opportunity cost.

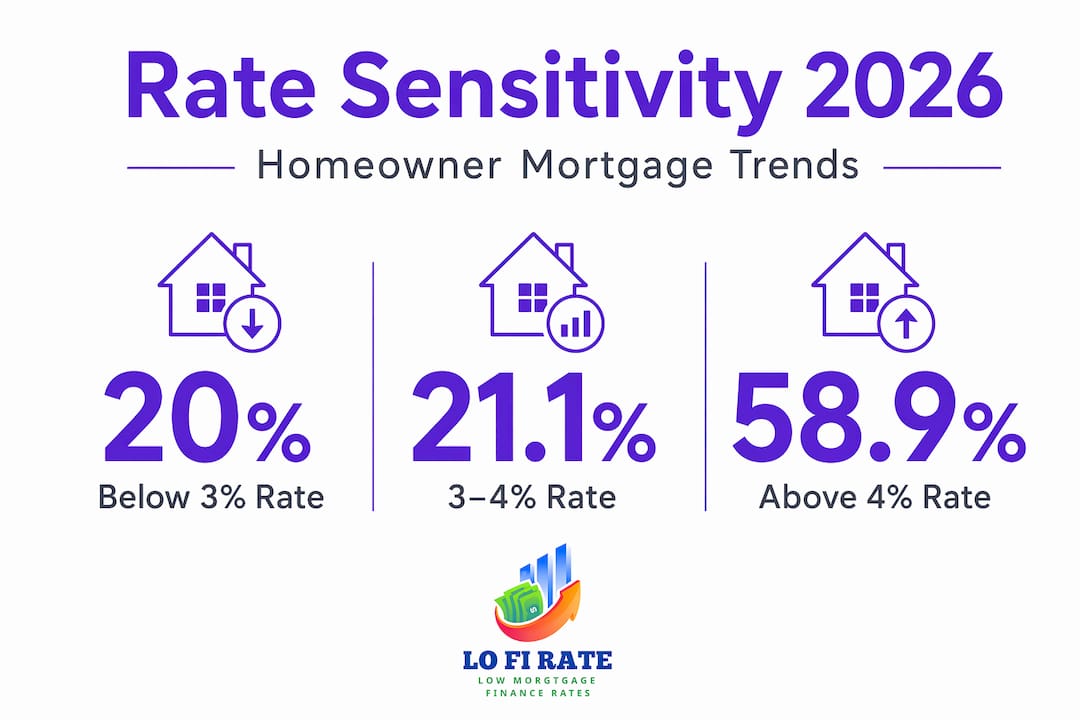

Here's why it matters right now. As of Q3 2025, 20% of U.S. mortgaged homeowners hold rates below 3%, while 21.1% hold rates of 6% or higher. That split creates two entirely different financial realities inside the same housing market. The homeowner locked into 2.75% has almost no financial incentive to sell and take on a new loan at 6.5% or 7%. That reluctance has a name: the lock-in effect.

The lock-in effect describes how financially disincentivized homeowners become when market rates rise above their current rate. According to FHFA research, for each percentage point that market rates exceed a homeowner's current rate, the probability of selling drops by 18.1%. That's not a small behavioral nudge. That's a structural freeze. Researchers estimate that 1.72 million home sales have been deferred since 2022 because of this effect.

The downstream consequence is that fewer homes hit the market, supply stays tight, and prices stay elevated. The lock-in effect increased national home prices by 7.0% through mid-2024. Understanding rate-sensitive markets means recognizing this feedback loop: low supply driven not by construction gaps alone, but by millions of homeowners doing rational math and staying put.

| Mortgage Rate Bucket | Share of U.S. Mortgaged Homeowners | Likely Behavior |

|---|---|---|

| Below 3% | 20% | Highly unlikely to sell or refinance |

| 3% to 5.99% | ~59% | Moderately rate-sensitive; situational decisions |

| 6% or higher | 21.1% | More flexible; open to refinancing if rates drop |

How rates affect refinancing decisions

Refinancing is where rate sensitivity shows up most visibly. Most homeowners think about refinancing the moment they see rates drop on the news. But chasing a headline rate without doing the math first is one of the most common and expensive mistakes a homeowner can make.

The general threshold that financial professionals use is a rate reduction of at least 0.50% to 0.75% below your current rate before refinancing makes sense. That benchmark exists because refinancing carries real costs. Typical closing costs run between $6,000 and $8,000. On a $400,000 loan, dropping from 7.25% to 6.27% saves approximately $247 per month, which means you'd need roughly 25 to 32 months just to break even before you see any net savings.

Here's a practical framework for making a refinancing decision:

- Calculate your break-even point. Divide your total closing costs by your projected monthly savings. If you plan to stay in the home beyond that timeline, refinancing likely makes sense.

- Set a mental rate floor. Decide in advance what rate would trigger your refinance. This keeps you from second-guessing every rate movement.

- Look beyond the monthly payment. Refinancing into a longer term at a lower rate can actually cost more over time. Evaluate total interest paid, not just monthly relief.

- Consider non-rate goals. Shortening your loan term, consolidating debt, or tapping home equity are all valid reasons to refinance even when rate savings alone don't justify it.

- Use rate locks and float-down provisions. A float-down option allows borrowers to lock a rate today while preserving the ability to capture a lower one before closing, typically for a small fee. In volatile markets, that flexibility is worth serious consideration.

Pro Tip: If you're refinancing primarily to lower your rate, document your break-even calculation before you apply. It will protect you from making an emotional decision when rates shift during the process.

Rate sensitivity and buying power

Rate sensitivity doesn't only affect current homeowners. It hits buyers hard, often before they even realize what's happening. Understanding how rates affect home buying means understanding how directly they translate into dollars a lender will approve.

A 0.5% rate increase on a $400,000 loan raises monthly payments by $130 to $150. That may not sound catastrophic, but multiply it across a qualifying income calculation and it can reduce the maximum loan amount by $20,000 to $30,000 or more. Early 2025's 62-basis-point rate drop enabled 2.8 million more households to qualify for mortgages. Rates move, and millions of people cross a qualification threshold in either direction.

Here's what a rate movement looks like in real payment terms:

| Rate | Monthly Payment on $400,000 Loan | Difference vs. 6.5% |

|---|---|---|

| 6.0% | $2,398 | -$134 |

| 6.5% | $2,528 | Baseline |

| 7.0% | $2,661 | +$133 |

| 7.5% | $2,797 | +$269 |

The pricing-out effect is where this gets serious. A buyer approved at 6.5% may be looking at homes priced up to $450,000. When rates move to 7.0%, that same buyer might only qualify for $415,000. They don't disappear from the market. They just get pushed into a lower price tier, which intensifies competition at more affordable price points.

The rate-sensitive buyer is often squeezed from both sides: rates make the loan more expensive, and lock-in effect among existing homeowners keeps inventory low, which keeps prices high. That's a difficult position requiring real strategy, not just patience.

Strategies to manage rate sensitivity

The goal isn't to predict rates perfectly. No one does that consistently, including institutional investors with rooms full of analysts. The goal is to improve your decision-making odds using information that's actually available to you.

- Watch Treasury yields, not just mortgage rates. Mortgage rates track closely with 10-year Treasury yields. When you see yields moving, mortgage rate changes are usually not far behind. Credit market commentary from institutions like S&P, Moody's, and BlackRock can give you a directional read before rates officially shift.

- Avoid the decision paralysis trap. Waiting for a rate that never comes is a real cost. If refinancing makes sense at your break-even threshold today, waiting six months for a rate that's 0.125% better may cost you thousands in interest paid on your current loan.

- Use a documented decision framework. Refinancing should be a disciplined decision tied to your financial goals, not a reaction to a news headline. Write down your threshold, your break-even, and your timeline before you start shopping.

- Consider float-down provisions as insurance. These underutilized risk management tools let you lock in a rate without fully sacrificing upside if conditions improve before closing. Ask your broker whether the cost makes sense given current market volatility.

- Recognize when rate sensitivity isn't the real issue. Sometimes homeowners stay put not because of the math, but because of the psychological weight of mobility. If a job change, family growth, or lifestyle shift is driving the decision, acknowledge that rates are only one variable.

Pro Tip: Set a calendar alert to review your mortgage situation every six months, not every time rates make the news. Reviewing on a schedule keeps you informed without letting market noise drive reactive decisions.

Explore smart mortgage-saving tactics that go beyond just watching rates, including how to negotiate terms, reduce closing costs, and evaluate your loan structure.

My honest take on rate sensitivity

I've seen what happens when homeowners understand this concept clearly versus when they don't. The ones who don't often make one of two mistakes: they freeze entirely, holding a property that no longer fits their life because the rate math scares them, or they act impulsively, refinancing for a 0.25% improvement that barely covers closing costs.

What I've learned is that rate sensitivity is a real financial condition, but it becomes a trap only when it drives decisions in isolation. The lock-in effect is real and powerful. But I've also watched homeowners stay in homes that stopped serving them for five years past the point of wisdom, waiting for a rate that never came back. That's not financial discipline. That's paralysis.

My take is this: the homeowners who handle rate sensitivity best treat their mortgage like any other financial position that needs periodic review. They set a threshold. They know their break-even. They watch bond markets, not mortgage ads. And when the numbers support a move, they move, without waiting for perfection.

The goal isn't to time the market. The goal is to be informed enough to act confidently when the right opportunity appears for your situation, not the average homeowner's.

— LoFi

Ready to stop guessing and start comparing?

If this article has you thinking about your own rate situation, whether you're locked into a great rate and wondering when it makes sense to move, or sitting in a higher-rate mortgage looking for relief, the next step is a conversation with someone who shops multiple lenders for you.

At Lofirate, we connect homeowners and buyers with licensed wholesale mortgage brokers who access rates from multiple lenders, not just one institution's pricing. That means you get a real comparison, not a single quote dressed up as a deal. Whether you're exploring a refinancing opportunity or evaluating purchase financing, a no-obligation consultation through Lofirate's broker matching gives you the information to make a decision grounded in actual numbers. You can also browse available loan options to see what programs fit your situation. Start at lofirate.com to request your connection today.

FAQ

What is a rate-sensitive homeowner?

A rate-sensitive homeowner is someone whose decisions about selling, refinancing, or staying put are significantly influenced by changes in mortgage interest rates. This sensitivity is most pronounced when current market rates are much higher than the rate on their existing loan.

What is the lock-in effect?

The lock-in effect occurs when homeowners with low mortgage rates avoid selling because taking on a new loan at higher market rates would dramatically increase their monthly costs. Research shows that selling probability drops 18.1% for each percentage point that market rates exceed a homeowner's current rate.

When does refinancing make financial sense?

Refinancing generally makes sense when the new rate is at least 0.50% to 0.75% lower than your current rate, and you plan to stay in the home long enough to pass the break-even point after closing costs.

How much does a 0.5% rate change affect buying power?

A 0.5% mortgage rate increase raises monthly payments on a $400,000 loan by $130 to $150 and can reduce your maximum qualifying loan amount by tens of thousands of dollars.

What is a float-down provision and why does it matter?

A float-down provision lets you lock in a mortgage rate today while keeping the option to capture a lower rate if one becomes available before closing. It's a practical tool for rate-sensitive borrowers in volatile markets who want protection without sacrificing potential savings.