TL;DR:

- Even modest rate drops in 2026 can lead to significant savings due to rising home equity and smarter loan products.

- The decision to refinance should be based on calculating the break-even point and how long you plan to stay in the home.

- Comparing multiple lenders and understanding all costs are crucial for maximizing refinance savings in 2026.

Most homeowners assume refinancing only makes sense when mortgage rates drop by at least one full percent. That idea is outdated. In 2026, a combination of shifting rate conditions, rising home equity, and smarter loan products means even modest rate changes can translate into real monthly savings. This article walks you through the numbers, the options, and the strategies so you can decide whether refinancing is the right move for your situation. No guesswork, no vague advice. Just clear, honest information to help you make a confident decision.

Table of Contents

- Should you refinance your mortgage in 2026?

- How much can you really save? The numbers behind refinancing

- Fixed vs. variable rates, points, and 'no-cost' refinances explained

- 2026 refinance strategies: Who benefits most (and when to avoid it)

- The overlooked truth about refinancing in 2026

- Ready to make your refinance pay off?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Closing costs matter | Expect to pay 2-6% of your mortgage for refinancing fees, which impact your total savings. |

| Break-even analysis | Calculate your break-even to know exactly when a refinance pays off. |

| No-cost options trade-off | Zero out-of-pocket options typically carry higher rates but boost flexibility. |

| Personalize your timing | Refinancing makes the most sense if you’ll stay in your home past the break-even point. |

| Action beats waiting | Decisive refinancers often save more than those who wait for perfect rates. |

Should you refinance your mortgage in 2026?

Refinancing is on the minds of millions of homeowners right now, and for good reason. After years of elevated rates, even small shifts in the market are creating opportunities worth exploring. But refinancing is not a one-size-fits-all solution, and understanding why people refinance is the first step toward knowing whether it applies to you.

The four most common reasons homeowners refinance are:

- Lower their interest rate to reduce monthly payments

- Shorten their loan term to pay off the mortgage faster

- Cash out home equity for renovations, debt payoff, or other needs

- Switch loan types, such as moving from an adjustable rate to a fixed rate

In 2026, 2026 mortgage rate trends provide critical context for refinance decisions, with gradual rate movement creating windows where locking in a new rate makes financial sense. Home prices have also stayed elevated in many markets, which means many homeowners have built up significant equity, opening the door to cash-out options or better loan terms.

That said, refinancing is not always the smart play. If you have already paid down most of your mortgage, restarting a 30-year loan could cost you more in interest over time even if your monthly payment drops. If you plan to move within the next two or three years, you may not stay in the home long enough to recoup the upfront costs.

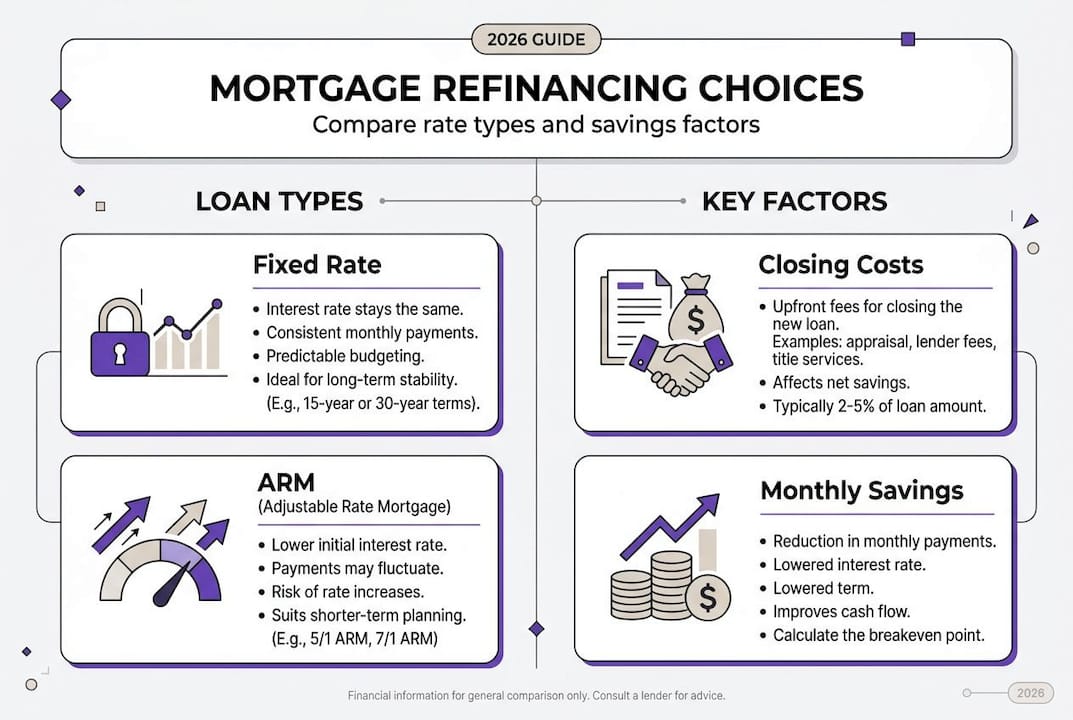

Speaking of costs: refinancing closing costs typically run 2 to 6 percent of the loan amount. On a $300,000 loan, that is between $6,000 and $18,000. That is not a small number, and it has to factor into any honest savings calculation.

A half-percent rate drop can make a noticeable impact depending on your balance and remaining term. But only if the timing and the costs align with how long you plan to stay.

| Refinance reason | Best situation | Potential risk |

|---|---|---|

| Lower rate | Rate dropped since original loan | Costs outweigh savings if moving soon |

| Shorten term | Income increased, want to pay off faster | Higher monthly payment |

| Cash-out equity | Major expense or debt consolidation | Increases loan balance |

| Switch loan type | ARM adjusting upward | Restart of amortization clock |

Before you decide, check whether you meet the 2026 qualification guide requirements, since lender standards for credit score, debt-to-income ratio, and equity have their own thresholds this year.

How much can you really save? The numbers behind refinancing

Once you understand the reasons to refinance, it is crucial to see what the actual savings and costs look like. Let us use a concrete example.

Suppose you have a $280,000 remaining balance on a 30-year fixed mortgage at 7.25%. You refinance to 6.75%, and your monthly payment drops by $95. Your closing costs come to $5,700. To find your break-even point, you divide costs by monthly savings: $5,700 divided by $95 equals 60 months, or five years. If you plan to stay in your home longer than five years, the refinance pays off. If not, you lose money.

Break-even analysis is calculated by dividing closing costs by monthly savings, and it is the single most useful number in any refinance decision.

Here is a quick look at how savings stack up across different scenarios:

| Loan balance | Rate change | Monthly savings | Closing costs (3%) | Break-even |

|---|---|---|---|---|

| $200,000 | 7.5% to 6.75% | ~$100 | $6,000 | ~60 months |

| $350,000 | 7.25% to 6.5% | ~$165 | $10,500 | ~64 months |

| $450,000 | 7.0% to 6.25% | ~$215 | $13,500 | ~63 months |

The main costs you will encounter when refinancing include:

- Origination fee: Charged by the lender to process the new loan

- Appraisal fee: Required to confirm current home value, usually $400 to $600

- Title insurance: Protects against ownership disputes

- Recording and transfer taxes: Vary by state and county

- Prepaid interest and escrow: Covers the gap between closing and your first payment

Pro Tip: A no-cost refinance rolls these fees into your loan balance or rate instead of requiring cash at closing. It can be a smart move if you are short on cash, but you will pay more over time. Compare the total cost of both paths before deciding.

When comparing mortgage rates across lenders, always ask for the APR, not just the interest rate. The APR includes fees and gives you a true cost comparison. Two loans with the same rate can have very different actual costs depending on what the lender bundles in.

Fixed vs. variable rates, points, and 'no-cost' refinances explained

Having looked at the math, the next step is understanding the nuts and bolts of your refinance options. There are a few key decisions you will face, and each one involves a trade-off.

Fixed rate vs. adjustable rate (ARM): A fixed rate stays the same for the life of the loan. An ARM starts lower but adjusts periodically based on a market index. If you plan to stay in your home long-term, a fixed rate gives you predictability. If you expect to sell or refinance again within five to seven years, an ARM's lower initial rate might save you money.

Paying points: Mortgage points are upfront fees you pay to buy down your interest rate. One point equals one percent of the loan amount. Paying one point on a $300,000 loan costs $3,000 and might reduce your rate by 0.25%. Whether that makes sense depends entirely on how long you keep the loan.

Pro Tip: Do not pay points if you are more than halfway through your current mortgage term. The savings rarely justify the upfront cost when your balance is already shrinking.

No-cost refinancing usually means a higher interest rate but preserves flexibility by avoiding upfront fees. It is a practical option if you expect rates to fall further and want to refinance again in a year or two without having wasted thousands on closing costs.

| Option | Best for | Trade-off |

|---|---|---|

| Fixed rate | Long-term homeowners | Higher initial rate than ARM |

| Adjustable rate | Short-term plans | Rate can rise after fixed period |

| Paying points | Staying 7+ years | High upfront cost |

| No-cost refinance | Uncertain timeline | Higher ongoing rate |

For a deeper look at how to get better refinance rates, the key is shopping multiple lenders rather than accepting the first offer. Wholesale brokers, in particular, can access pricing that retail banks do not offer directly to consumers. Broker refinance tips consistently show that borrowers who compare at least three quotes save significantly more than those who do not. The refinancing workflow in 2026 has also become more streamlined, making it easier than ever to get multiple quotes quickly.

2026 refinance strategies: Who benefits most (and when to avoid it)

After breaking down each refinance option, let us focus on who refinancing actually helps in 2026 and who should pass.

The homeowners who stand to gain the most include:

- High-rate borrowers: If you locked in a rate above 7% in 2022 or 2023, even a modest drop to the mid-6% range can produce meaningful monthly savings.

- Those with improved credit: A credit score jump of 40 to 60 points since your original loan could qualify you for a noticeably lower rate.

- Cash-out candidates: If your home has appreciated significantly, a cash-out refinance lets you tap that equity at mortgage rates, which are typically lower than personal loans or credit cards.

On the other hand, refinancing is probably not worth it if:

- You plan to sell or move within the next two to three years

- You are already 20 or more years into a 30-year mortgage

- Your credit score has dropped since your original loan

- Current rates are not meaningfully lower than what you already have

"Divide costs by monthly savings; only refinance if you will stay long enough to benefit." This principle is the foundation of every smart refinance decision. Refinancing makes sense when the break-even point fits your expected time in the home.

Common mistakes homeowners make when refinancing:

- Focusing only on the monthly payment and ignoring total interest paid over the new term

- Not factoring in all closing costs, including prepaid items and escrow

- Extending back to a 30-year term when they were already 10 years in, resetting the amortization clock

- Skipping the comparison step and accepting the first rate offered

- Refinancing too frequently and paying closing costs multiple times without enough savings to justify it

The refinance step-by-step guide walks through each stage of the process in detail, from pulling your credit to closing the new loan.

The overlooked truth about refinancing in 2026

With the basics covered, let us address what most homeowners and even financial media get wrong about refinancing. The narrative is almost always about timing the market. Wait for rates to drop. Hold out for the perfect moment. But here is the uncomfortable reality: waiting has a cost too.

Every month you stay in a higher-rate loan is money you are not saving. If refinancing would save you $150 per month and you wait 12 months hoping for a better rate, you have already given up $1,800 in potential savings. That is real money.

The homeowners who come out ahead are not the ones who time the market perfectly. They are the ones who run their numbers, understand their break-even point, and act when the math works for their situation. Rates do not have to hit some magic number. The question is whether your numbers work for you right now.

The smartest move is to compare lenders using wholesale access rather than walking into a single retail bank. The difference in rate offers can be substantial, and it costs nothing to compare. Indecision dressed up as patience is still costing you money every single month.

Ready to make your refinance pay off?

If the numbers in this article made you think twice about your current mortgage, that reaction is worth acting on. Knowing the break-even math is one thing. Getting a real quote based on your actual loan balance, credit profile, and goals is where savings become concrete.

LoFiRate connects you with licensed wholesale mortgage brokers who shop multiple lenders to find competitive low mortgage rates you will not find walking into a retail bank. There is no obligation and no pressure. You can explore your 2026 loan options at your own pace and see what a refinance could actually look like for your situation. Start with a free consultation through our mortgage broker matching service and find out what you could be saving every month.

Frequently asked questions

What are typical closing costs when refinancing in 2026?

Expect to pay 2 to 6 percent of your loan amount in closing costs, covering origination, appraisal, title insurance, and related fees.

How do I know if refinancing will save me money?

Divide closing costs by your expected monthly savings to find your break-even point; if you plan to stay in the home past that point, refinancing likely pays off.

Is a no-cost refinance a good option?

A no-cost refinance works well for short-term flexibility, but you will typically carry a higher interest rate than if you paid closing costs upfront.

Who benefits most from refinancing in 2026?

Homeowners with high existing rates, improved credit scores, or significant home equity tend to see the largest monthly savings from refinancing this year.