TL;DR:

- Your debt-to-income ratio measures the percentage of gross monthly income used for recurring debts. A ratio below 36% indicates healthy finances, while above 50% severely limits borrowing options. Lowering DTI involves paying off high-interest debts or increasing income, improving loan approval chances.

The debt-to-income ratio is defined as the percentage of your gross monthly income that goes toward paying recurring debt obligations. Lenders use this number, commonly called DTI, to judge whether you can handle new loan payments without financial strain. The formula is simple: divide your total monthly debt payments by your gross monthly income, then multiply by 100. A DTI below 36% signals healthy finances to most lenders, while anything above 50% severely limits your borrowing options. Understanding your DTI before you apply for a mortgage or personal loan puts you in a stronger position at the negotiating table.

What is debt-to-income ratio and how do you calculate it?

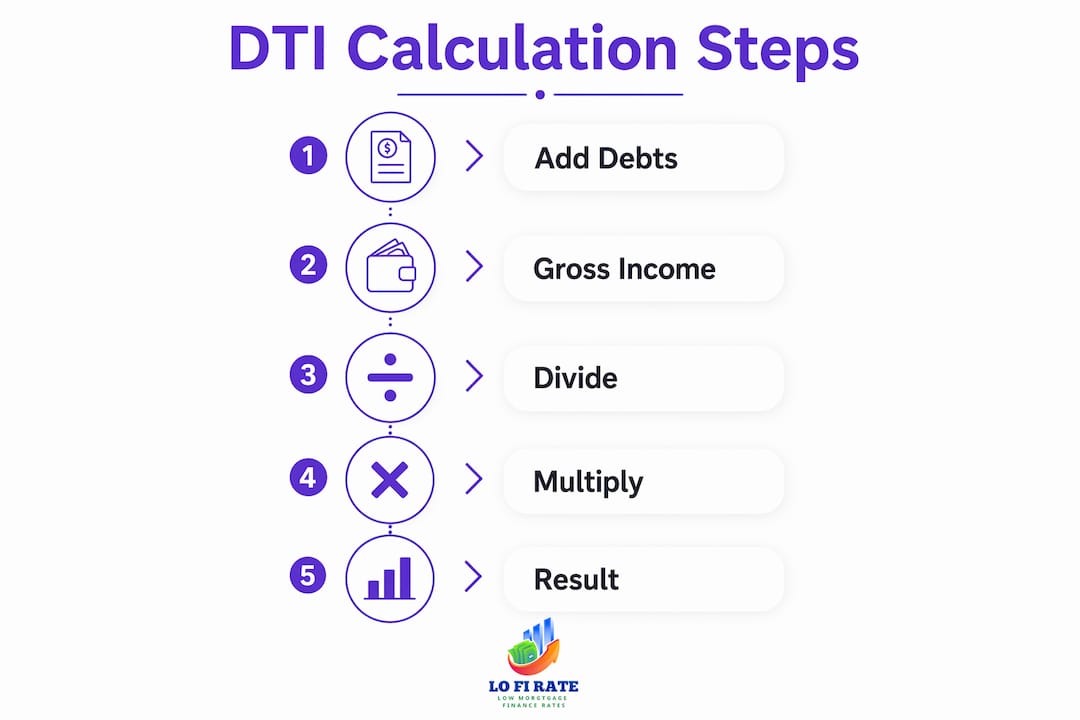

Calculating your DTI takes three steps, and the math is straightforward once you know what counts.

Step 1: Add up your monthly debt payments. Include every recurring debt obligation you owe each month. Qualifying debts include mortgage or rent payments, car loans, student loans, minimum credit card payments, and personal loan payments. Do not include utilities, groceries, subscriptions, or insurance premiums. Lenders exclude living expenses like utilities and groceries from DTI calculations entirely. Including them is one of the most common mistakes borrowers make.

Step 2: Determine your gross monthly income. Gross income is what you earn before taxes and deductions. If you earn $72,000 per year, your gross monthly income is $6,000. Include all reliable income sources: salary, freelance income, rental income, and alimony if it is documented and consistent.

Step 3: Apply the formula. Divide your total monthly debts by your gross monthly income, then multiply by 100.

Example: You pay $400 for a car loan, $200 in student loan payments, and $150 in minimum credit card payments each month. That totals $750 in monthly debt. Divide $750 by a gross monthly income of $5,000, and you get 0.15. Multiply by 100 to get a DTI of 15%. That is an excellent ratio by any lender's standard.

Pro Tip: Do not use your take-home pay as the income figure. Lenders always calculate DTI using gross income, which is your earnings before taxes. Using net pay will make your DTI look worse than it actually is.

Why does debt-to-income ratio matter to lenders and borrowers?

DTI is a lender's primary risk tool. A lower ratio tells a lender you have enough income to absorb a new monthly payment without defaulting. Lenders use DTI to measure borrower risk directly, and a low DTI increases their confidence in your ability to repay.

DTI works alongside your credit score, not instead of it. Your credit score reflects your payment history and credit behavior. Your DTI reflects your current financial load. A borrower with a strong credit score but a high DTI can still get denied, because the lender sees too little room in the monthly budget for a new payment.

One important distinction: DTI does not directly affect your credit score. However, the debts that push your DTI higher, especially high revolving balances, also raise your credit utilization rate. High credit utilization does hurt your score. The two metrics are separate but connected.

Here is what a healthy DTI does for you as a borrower:

- More loan options. Lenders offer better terms to borrowers with low DTI because the risk is lower.

- Lower interest rates. A strong DTI, combined with a good credit score, positions you for competitive rates.

- Greater financial flexibility. A low DTI means more of your income is free each month, which protects you during emergencies.

- Faster approvals. Underwriters spend less time scrutinizing applications from borrowers with clean DTI numbers.

Understanding the importance of debt-to-income ratio in the mortgage process helps you prepare before you ever submit an application.

What is a good debt-to-income ratio? DTI benchmarks explained

Mortgage lenders analyze two types of DTI ratios. The front-end DTI covers housing costs only, including principal, interest, taxes, and insurance, often called PITI. The back-end DTI covers all recurring debts combined. Most lenders focus on the back-end figure when making approval decisions.

The four standard DTI tiers work as follows:

| DTI Range | Lender Reaction | What It Means for You |

|---|---|---|

| Below 36% | Strong approval odds | You manage debt well; most loan products are available |

| 36%–42% | Caution zone | Approval is possible but lenders look harder at other factors |

| 43%–50% | Difficult to qualify | Many loan programs become unavailable; exceptions may apply |

| Above 50% | Severely limited options | Most lenders will decline; significant debt reduction needed |

These DTI tiers are the standard benchmarks used across the mortgage and personal loan industries. A DTI below 36% is the target most financial advisors recommend.

Borrowers in the 43%–50% range are not automatically disqualified. Compensating factors like significant cash reserves or a high credit score can lead lenders to make exceptions. These factors signal that you have a financial cushion even if your monthly obligations are heavy. Knowing this matters if your DTI is borderline and you are preparing a mortgage application.

Pro Tip: If you are comparing loan types, FHA loans historically allow higher back-end DTI ratios than conventional loans. Check the DTI thresholds for FHA vs. conventional loans before deciding which program fits your situation.

How to reduce your DTI before applying for a loan

Lowering your DTI before a major loan application is one of the highest-return financial moves you can make. The two levers are simple: reduce your monthly debt payments or increase your gross monthly income.

Here are the most effective strategies:

- Pay down high-interest installment debt first. Prioritizing installment debts like car loans or personal loans reduces your monthly obligation faster than making extra payments on revolving credit.

- Avoid taking on new debt before applying. Every new loan or credit card minimum payment raises your DTI. Hold off on financing a car or opening new credit accounts for at least six months before a mortgage application.

- Pay off small balances entirely. Eliminating a $150 monthly payment from a small personal loan drops your DTI immediately and noticeably.

- Increase your income. A raise, a part-time job, or documented freelance income raises the denominator in the DTI formula and lowers your ratio without touching your debts.

- Consolidate multiple debts. Rolling several high-payment debts into one lower-payment loan can reduce your total monthly obligation, though you should compare total interest costs before consolidating.

A common misconception is that closing a credit card improves DTI. Closing a card does not reduce your DTI unless you also pay off the balance. The monthly minimum payment is what counts, not the card's existence. Separately, closing a card can hurt your credit score by reducing available credit. Focus on paying balances down, not closing accounts.

You can also review strategies to increase refinance approval if you are working to qualify for a refinance with a higher current DTI.

How lenders calculate DTI differently from your own estimate

Your personal DTI calculation and a lender's DTI calculation can produce different numbers. Knowing why helps you avoid surprises during underwriting.

- Self-employed income averaging. Mortgage lenders may average income over two years for self-employed borrowers. If your income was lower in one of those years, the averaged figure will be lower than your current earnings, which raises your calculated DTI.

- Excluded short-term debts. Some lenders exclude debts with fewer than 10 or 12 payments remaining. A car loan with 8 months left may not count against you.

- Rental income treatment. Lenders typically count only 75% of rental income to account for vacancy risk. Using 100% in your own calculation will give you an optimistic DTI.

- Alimony and child support. These count as monthly debt obligations in most lender calculations, even if you think of them as personal expenses.

The practical takeaway: always ask your lender exactly which income sources and debts they will include before you estimate your qualifying DTI. A mortgage calculator can help you model different scenarios before you sit down with a lender.

Key Takeaways

Your debt-to-income ratio is the single most controllable financial metric you can improve before applying for a mortgage or major loan.

| Point | Details |

|---|---|

| Core DTI formula | Divide total monthly debt payments by gross monthly income, then multiply by 100. |

| Target ratio | A DTI below 36% gives you the strongest loan approval odds and best rate options. |

| What counts as debt | Include loans, credit cards, and mortgages. Exclude utilities, groceries, and insurance. |

| Credit score connection | DTI does not directly affect your credit score, but high balances raise credit utilization, which does. |

| Lender differences | Lenders may adjust income or exclude short-term debts, so your self-calculated DTI may differ from theirs. |

DTI is the number most borrowers ignore until it's too late

Most people check their credit score obsessively and never look at their DTI until a lender flags it. I have seen borrowers with 760 credit scores get surprised by a denial because their monthly obligations were too high relative to their income. The score opened the door. The DTI closed it.

The real value of tracking your DTI is that it forces you to think about your monthly cash flow, not just your credit history. A credit score tells a lender how you have behaved in the past. Your DTI tells them what your life looks like right now. Both matter, but DTI is the one you can change fastest with deliberate action.

One thing I consistently see misunderstood: people assume that earning more money automatically fixes a high DTI. It helps, but only if you do not simultaneously take on more debt. Lifestyle creep is real. A raise that gets absorbed by a new car payment and a larger apartment does nothing for your DTI. The ratio only improves when income grows faster than obligations.

My honest recommendation is to calculate your DTI every six months, the same way you check your credit report. Treat it as a vital sign. If it is climbing, that is a signal to pause before taking on new financial commitments. If it is falling, you are building real borrowing power.

— LoFi

Your DTI and your mortgage options, explained by Lofirate

Understanding your DTI is the first step. Knowing how it interacts with real loan programs is where most borrowers need a guide.

Lofirate connects you with licensed wholesale mortgage brokers who review your full financial picture, including your DTI, credit profile, and income sources, to find loan options that fit your situation. Wholesale brokers shop multiple lenders, which means you get competitive rate options instead of a single retail quote. Whether you are buying your first home or refinancing an existing mortgage, a no-obligation consultation through Lofirate can show you exactly where your DTI stands and which loan programs are within reach. You can also review available loan options to see which programs align with your current ratio.

FAQ

What is the debt-to-income ratio in simple terms?

The debt-to-income ratio is the percentage of your gross monthly income that goes toward paying recurring debts. Divide your total monthly debt payments by your gross monthly income and multiply by 100 to get your DTI.

What counts as debt in a DTI calculation?

Lenders count mortgage payments, car loans, student loans, personal loans, and minimum credit card payments. Utilities, groceries, and insurance are not included in DTI calculations.

What is a good DTI ratio for a mortgage?

A DTI below 36% is considered strong by most mortgage lenders. DTI ratios above 43% make qualifying for most conventional loan programs significantly harder.

Does DTI affect my credit score?

DTI does not directly affect your credit score. However, the high revolving balances that raise your DTI also increase your credit utilization rate, which does negatively impact your score.

Can I get a mortgage with a high DTI?

Yes, in some cases. Compensating factors like strong cash reserves or a high credit score can help borrowers with DTI ratios in the 43%–50% range qualify for certain loan programs, including FHA loans.