Most homebuyers think all mortgage lenders work the same way, but that's far from reality. A mortgage lender is any institution or individual that provides funds to purchase real estate, with the loan secured by the property itself. The type of lender you choose directly impacts your interest rate, loan options, and overall borrowing costs. Understanding the differences between direct lenders, mortgage bankers, portfolio lenders, and wholesale lenders helps you make smarter financing decisions. This guide breaks down what mortgage lenders do, how the lending process works, and why wholesale lenders accessed through brokers often deliver the most competitive rates for both home purchases and refinancing.

Table of Contents

- Key takeaways

- What is a mortgage lender and how do they work?

- Types of mortgage lenders: direct, portfolio, wholesale, and bankers

- How the mortgage lending process works: from application to closing

- Why choose wholesale mortgage lenders: benefits and competitive rates

- Explore low mortgage rates and loan options at LO FI RATE

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Lender type matters | The category you choose affects interest rates, loan options, and total borrowing costs. |

| Direct vs bank loans | Direct lenders fund with their own capital and work with you from application to closing, often offering fewer loan options. |

| Portfolio lender flexibility | Portfolio lenders keep loans in house and can customize terms for borrowers who don't fit conventional guidelines, often with higher rates. |

| Wholesale via brokers | Wholesale lenders fund through licensed brokers, reducing retail costs and typically delivering the most competitive rates for purchases and refinances. |

What is a mortgage lender and how do they work?

A mortgage lender provides capital for real estate loans, expecting repayment with interest over time. The property you purchase serves as collateral, meaning the lender can foreclose if you default on payments. This security arrangement allows lenders to offer lower interest rates compared to unsecured loans like credit cards or personal loans.

Lenders assess your financial risk before approving any loan. They examine your credit history, income stability, existing debts, and available assets to determine whether you can reliably make monthly payments. This evaluation protects both parties by ensuring you don't take on unaffordable debt.

Mortgage lenders come in various forms:

- Traditional banks that offer mortgages alongside checking accounts and other services

- Credit unions that provide member-focused lending with competitive rates

- Online lenders that streamline applications through digital platforms

- Mortgage companies that specialize exclusively in home loans

- Individual private lenders who fund loans directly from personal capital

Each lender type operates differently, but all share the same basic function of providing borrowed funds. The key differences lie in their funding sources, overhead costs, and loan product variety. Understanding these distinctions helps you identify which lender category best matches your financial situation and homebuying goals.

Your relationship with a mortgage lender typically spans decades. Choosing the right one requires looking beyond just the interest rate to consider customer service quality, loan flexibility, and long-term support throughout the repayment period.

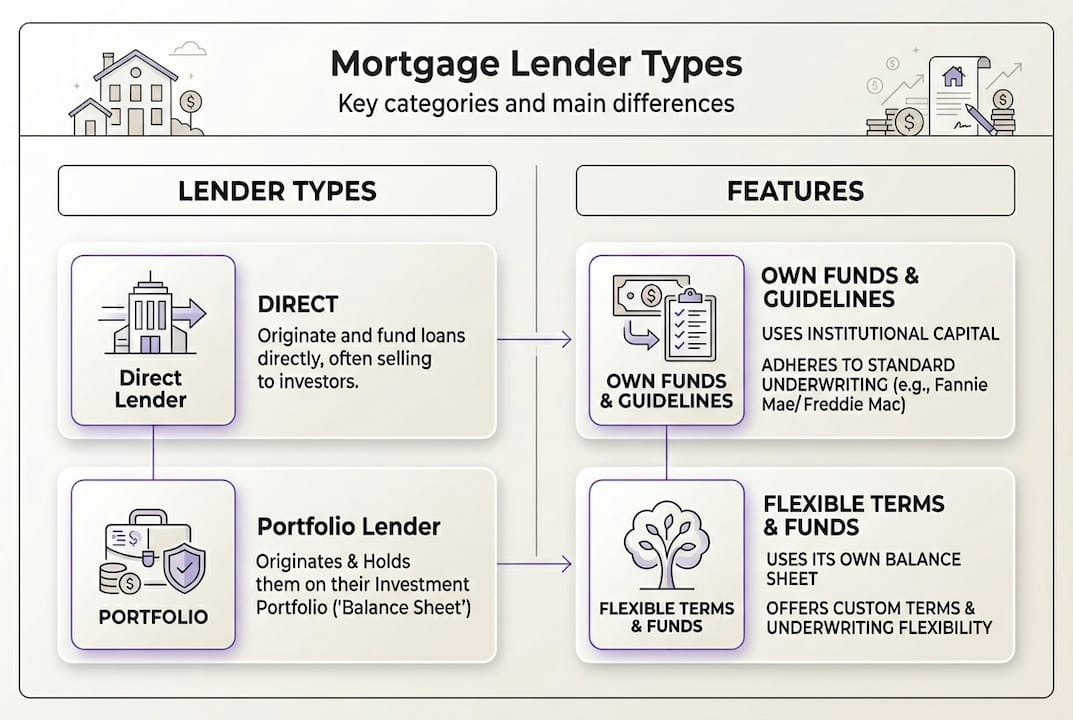

Types of mortgage lenders: direct, portfolio, wholesale, and bankers

Mortgage lenders fall into four main categories, each with distinct operational models that affect your borrowing experience and costs.

Direct lenders use their own capital to fund your mortgage. Banks and credit unions typically operate as direct lenders, drawing from depositor funds or institutional reserves. You work directly with these lenders from application through closing, which simplifies communication but limits your loan options to what that single institution offers.

Mortgage bankers originate loans using either their own funds or warehouse lines of credit from larger institutions. Unlike banks that hold deposits, mortgage bankers focus exclusively on loan origination. They often sell completed loans to secondary market investors, allowing them to recycle capital and fund new mortgages. This model provides more loan volume capacity than traditional banks.

Portfolio lenders keep loans in-house rather than selling them to secondary markets. This approach gives them flexibility to approve borrowers who don't fit conventional lending guidelines. Portfolio lenders can customize loan terms and consider unique financial situations that automated underwriting systems might reject. However, their rates may run slightly higher to compensate for increased risk retention.

Wholesale lenders fund mortgages exclusively through licensed mortgage brokers rather than working directly with borrowers. This distribution model eliminates retail branch costs, marketing expenses, and direct customer service infrastructure. The savings translate to more competitive rates and access to 50+ loan products from multiple wholesale lenders through a single broker relationship.

Pro Tip: Working with a mortgage broker who accesses wholesale lenders gives you the pricing advantages of multiple lenders without the hassle of applying separately to each one.

| Lender type | Funding source | Borrower access | Rate competitiveness |

|---|---|---|---|

| Direct lender | Own capital/deposits | Direct application | Moderate |

| Mortgage banker | Own funds/warehouse lines | Direct application | Moderate to good |

| Portfolio lender | Own capital (held) | Direct application | Moderate (flexible terms) |

| Wholesale lender | Institutional capital | Via mortgage brokers | Highest (lowest overhead) |

Understanding these lender types helps you decide whether to apply directly to a retail institution or work with a broker who can shop wholesale options. Many borrowers save thousands by exploring both paths and comparing actual rate quotes. The questions you ask mortgage brokers can reveal which wholesale lenders offer the best combination of rates and loan features for your situation.

How the mortgage lending process works: from application to closing

The mortgage lending process follows a structured sequence that protects both you and the lender while ensuring the property value supports the loan amount.

-

Pre-approval: You submit basic financial information to get a conditional approval letter showing how much you can borrow. This step strengthens your position when making offers on homes.

-

Formal application: Once you've found a property, you complete a full mortgage application with detailed financial documentation. Expect to provide pay stubs, tax returns, bank statements, and identification.

-

Processing and verification: The lender's processing team verifies your employment, income, assets, and credit history. They contact employers, review bank statements, and pull credit reports to confirm accuracy.

-

Underwriting assessment: Underwriters evaluate risk using the 4Cs: credit (payment history and score), capacity (income relative to debts), capital (reserves and down payment), and collateral (property value). This analysis determines whether to approve, deny, or request additional documentation.

-

Property appraisal: An independent appraiser inspects the property and compares it to recent sales of similar homes. The appraisal protects the lender by confirming the property's value justifies the loan amount. Low appraisals can require larger down payments or renegotiated purchase prices.

-

Final approval and closing: After satisfying all underwriting conditions and receiving an acceptable appraisal, you receive final loan approval. The closing appointment involves signing loan documents, transferring funds, and receiving property ownership.

Pro Tip: Gather financial documents early and avoid major purchases or credit changes during the mortgage process. New debts or income disruptions can derail approvals even days before closing.

The entire process typically takes 30 to 45 days, though complexity and documentation issues can extend timelines. Understanding each phase helps you respond quickly to lender requests and avoid delays. Your mortgage qualification preparation directly impacts how smoothly underwriting proceeds and whether you receive the best available rates.

Lenders scrutinize your financial stability because they're committing hundreds of thousands of dollars over decades. Demonstrating consistent income, responsible credit management, and adequate reserves gives underwriters confidence in your repayment ability.

Why choose wholesale mortgage lenders: benefits and competitive rates

Wholesale lenders accessed through mortgage brokers deliver significant advantages over retail lending channels, particularly for rate-conscious borrowers and those refinancing existing mortgages.

Lower overhead costs create immediate pricing benefits. Wholesale lenders eliminate retail branches, direct marketing campaigns, and large customer service departments. These savings flow directly to borrowers through reduced interest rates and lower origination fees. The difference often ranges from 0.25% to 0.5% compared to retail lenders, translating to thousands in savings over a 30-year mortgage.

Loan product variety expands your options dramatically. While retail banks typically offer 5 to 10 loan programs, brokers accessing wholesale lenders can present 50+ options from multiple institutions. This variety proves especially valuable for self-employed borrowers, those with unique income sources, or buyers seeking specialized loan features.

Refinancing becomes more attractive through wholesale channels. Homeowners looking to reduce monthly payments or tap equity benefit from the competitive rate environment wholesale lenders create. The ability to compare multiple wholesale offers simultaneously ensures you're not leaving money on the table by accepting the first retail quote you receive.

Pro Tip: Even if you're pre-approved with a retail lender, getting a second opinion from a broker with wholesale access costs nothing and often reveals better rate options you didn't know existed.

| Lender channel | Average rate markup | Loan options available | Best for |

|---|---|---|---|

| Retail bank | 0.50% to 0.75% | 5 to 10 products | Existing bank customers wanting convenience |

| Credit union | 0.25% to 0.50% | 8 to 15 products | Members seeking moderate rates |

| Online lender | 0.25% to 0.50% | 10 to 20 products | Tech-savvy borrowers comfortable with digital process |

| Wholesale via broker | 0.00% to 0.25% | 50+ products | Rate shoppers and refinancers maximizing savings |

The wholesale model works because brokers earn compensation from lenders rather than marking up rates to cover retail infrastructure. You gain access to institutional pricing typically reserved for high-volume mortgage operations. This arrangement particularly benefits refinancing scenarios where even small rate reductions generate substantial lifetime savings.

Shopping wholesale lenders through brokers requires understanding that brokers work for you, not the lender. Licensed brokers have fiduciary duties to present suitable options and disclose all compensation. This transparency protects borrowers while maintaining the competitive pricing advantages wholesale lending provides.

Many homeowners discover refinancing with wholesale brokers saves enough to justify the effort even when their current rate seems reasonable. Market conditions change, and wholesale access ensures you're comparing against true market-bottom pricing rather than retail markup rates.

Explore low mortgage rates and loan options at LO FI RATE

Understanding mortgage lender types and the lending process empowers you to make informed borrowing decisions, but finding actual competitive rates requires access to the right lending channels.

LO FI RATE connects homebuyers and homeowners with licensed wholesale mortgage brokers who shop multiple lenders to find competitive rate options. Unlike retail lenders offering only their own pricing, the platform provides access to diverse loan products from wholesale sources with lower overhead costs. Whether you're purchasing your first home or refinancing to reduce monthly payments, exploring loan options at LO FI RATE gives you a transparent second opinion on available rates.

The platform focuses on simplicity and consumer protection by connecting you with licensed brokers in your state for no-obligation consultations. You avoid overpaying retail pricing while gaining access to the same institutional rates that high-volume mortgage operations receive. This approach helps you apply the knowledge from this guide to actual lending scenarios where competitive rates translate to real savings.

Frequently asked questions

What is the difference between a mortgage lender and a mortgage broker?

A mortgage lender provides the actual loan funds and assumes the risk of your repayment. Lenders can be banks, credit unions, or specialized mortgage companies that use their own capital or institutional funding sources. A mortgage broker acts as an intermediary who connects you with multiple lenders and helps you compare loan options. Brokers don't lend money themselves but earn compensation from lenders for originating loans. Working with a broker gives you access to wholesale lenders and more loan products than approaching a single retail lender directly.

How can I get the best mortgage rates in 2026?

Securing the best mortgage rates requires comparing offers from multiple lenders, including wholesale options accessed through mortgage brokers. Maintain a strong credit score above 740, reduce existing debts to improve your debt-to-income ratio, and save for a larger down payment to qualify for better pricing tiers. Shopping mortgage lenders with wholesale brokers often reveals rates 0.25% to 0.5% lower than retail channels. Lock your rate when market conditions favor borrowers, and consider paying points if you plan to keep the mortgage long-term.

What documents are needed to apply for a mortgage?

Mortgage applications require proof of income including recent pay stubs, W-2 forms, and two years of tax returns. Self-employed borrowers need additional documentation like profit and loss statements and business tax returns. Lenders review your credit history through credit reports they pull directly. Provide bank statements showing assets for down payment and reserves, typically covering two to six months of mortgage payments. You'll need government-issued identification and details about the property you're purchasing, including the purchase contract and property address. Gathering these documents before applying speeds up the approval process significantly.

Why should I consider refinancing through a wholesale lender?

Wholesale lenders accessed through brokers typically offer lower refinance rates due to reduced overhead costs compared to retail banks. You gain access to a wider variety of loan products, increasing the likelihood of finding terms that match your financial goals. Refinancing with wholesale lenders can reduce your monthly payments, shorten your loan term, or allow you to tap home equity at competitive rates. Even small rate reductions of 0.5% translate to substantial interest savings over the remaining loan period. Brokers shop multiple wholesale lenders simultaneously, ensuring you see the most competitive options available for your situation.