TL;DR:

- Most homebuyers apply to only one lender, often overpaying thousands in fees.

- Comparing multiple lenders and focusing on APRs can save significant money over the life of a loan.

- Negotiating, understanding mortgage terms, and using wholesale brokers improve chances of securing better rates.

Most homebuyers make a costly mistake before they even sign a single document. They apply with one lender, accept the first offer, and move on, never realizing they may have left thousands of dollars on the table. Nearly 70% of U.S. homebuyers apply with only one lender and often overpay as a result. This guide breaks down exactly why that happens, what you need to know before you shop, and the specific steps to take so you stop overpaying and start saving real money on one of the biggest financial decisions of your life.

Table of Contents

- Why most homebuyers overpay on their mortgage

- What you need before shopping: Mortgage basics and key terms

- Step-by-step: How to shop for the best mortgage rate

- Common pitfalls and how to verify your results

- Our take: Most experts oversimplify mortgage savings

- Compare and save with LoFi Rate

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Rate shopping pays | Comparing multiple lender quotes can save you thousands on mortgage costs. |

| APR matters most | Always compare annual percentage rates and total fees, not just the lowest rate. |

| Beware hidden fees | Review loan estimates side-by-side to catch extra costs before you commit. |

| Brokers help you win | A good broker can connect you with wholesale rates and unbiased comparisons. |

| Behavioral traps | Sticking with one lender or rushing the process could cost you big. |

Why most homebuyers overpay on their mortgage

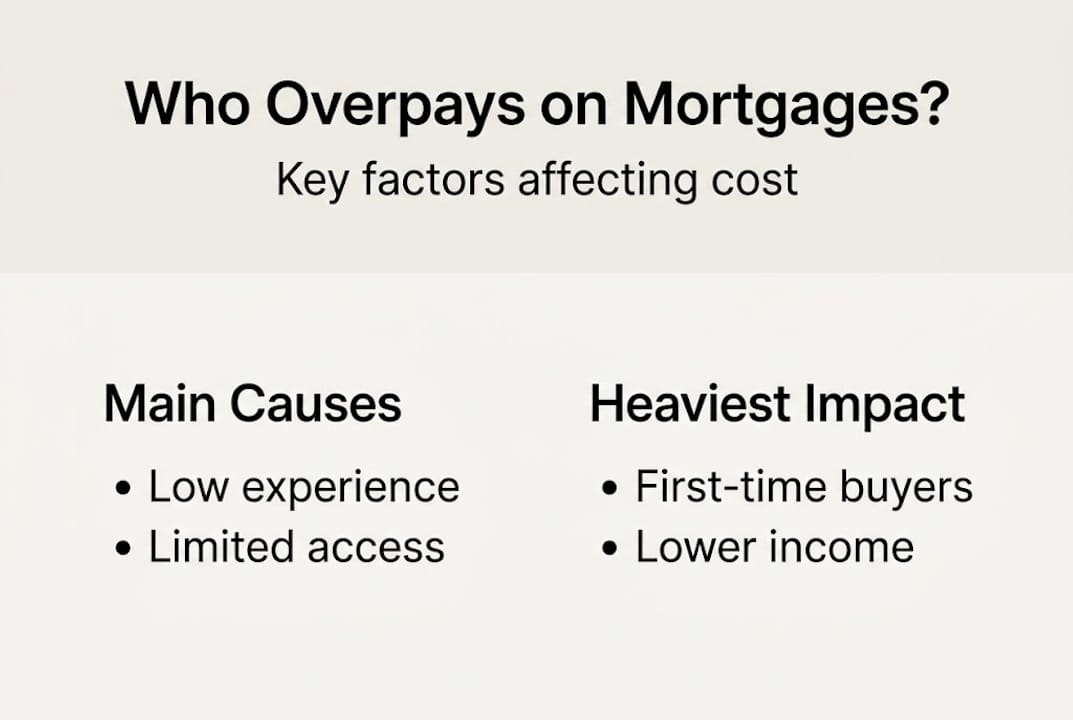

The numbers are hard to ignore. U.S. homebuyers overpay more than $13 billion annually in mortgage fees, and most of that loss is completely avoidable. The root cause is simple: most people do not compare. They find a lender through a real estate agent referral or a familiar bank name, apply once, and assume the offer is fair.

First-time buyers and lower-income borrowers carry the heaviest burden here. They are less familiar with how mortgage pricing works, less likely to negotiate, and more likely to trust a single source. Repeat buyers and higher-income borrowers, by contrast, tend to shop more aggressively and end up paying less. The gap is not small. It adds up to real money every single month.

Understanding why comparing lenders matters is the first step to protecting yourself. Lenders price loans differently based on their own costs, risk appetite, and profit targets. There is no single "market rate" that every lender offers you. What one bank quotes you today could be a quarter point higher than what a wholesale broker finds tomorrow.

Here is what overpaying actually looks like in practice:

- One lender, no comparison: You accept a 7.25% rate when 6.75% was available elsewhere

- Ignoring fees: A low advertised rate comes with $4,000 in origination fees you did not see coming

- Skipping the APR: You compare monthly payments instead of the annual percentage rate, missing the true cost

- Trusting the referral: Your real estate agent sends you to their preferred lender, who may not offer the best pricing

"On a typical $360,000 loan, shopping for a lower rate can save $1,104 per year." That is over $33,000 across a 30-year loan.

The math is straightforward. The behavior change is harder. But once you see what is at stake, it becomes very difficult to justify skipping the comparison step. The typical mortgage fees explained on a standard loan can vary widely from lender to lender, and that variation is where your savings hide.

What you need before shopping: Mortgage basics and key terms

Before you request a single quote, you need a working vocabulary and the right documents. Walking into rate shopping unprepared is like negotiating a car price without knowing what the dealer paid for it. You need the basics first.

Key terms to know:

- APR (Annual Percentage Rate): The true yearly cost of your loan, including interest and most fees. Always use this for comparisons.

- Rate lock: An agreement that freezes your interest rate for a set period while your loan closes.

- Origination fee: What the lender charges to process your loan, often expressed as a percentage of the loan amount.

- Mortgage broker: A licensed professional who shops multiple wholesale lenders on your behalf, rather than lending their own money.

- Retail lender: A bank or direct lender offering only their own loan products at their own pricing.

- Loan estimate: A standardized three-page document every lender must give you within three business days of your application. Use it to compare apples to apples.

To understand mortgage fees properly, you also need to know what to bring to the table. Gather these documents before you start:

- Last two years of tax returns and W-2s

- Recent pay stubs (last 30 days)

- Two to three months of bank statements

- Your credit report (check it free at AnnualCreditReport.com)

- A list of your debts and monthly obligations

| Term | What it means | Why it matters |

|---|---|---|

| Interest rate | The base cost of borrowing | Starting point, but incomplete |

| APR | Rate plus fees, annualized | Best comparison tool |

| Points | Upfront fee to lower your rate | Trade-off: pay now or pay monthly |

| Origination fee | Lender processing charge | Varies widely, always negotiate |

| Rate lock | Frozen rate during closing | Protects you from rate spikes |

The single biggest mistake shoppers make is comparing interest rates instead of APRs. Evaluate total cost using the APR, not just the interest rate, because two loans with the same rate can have very different total costs once fees are included.

Pro Tip: When you receive a loan estimate, go straight to Page 2, Section A. That is where origination charges live. This number tells you exactly what the lender is making on your loan.

Step-by-step: How to shop for the best mortgage rate

Now that you are prepared, here is a clear process to follow. Do not skip steps. Each one builds on the last.

- Pull your credit report first. Know your score before any lender does. Errors on your report can cost you a better rate, and you have the right to dispute them.

- Contact at least three to five lenders or brokers. Include at least one licensed mortgage broker who can access wholesale pricing. Mortgage brokers often get better rates because they shop multiple lenders simultaneously.

- Request a loan estimate from each one. This is a federally standardized form. Every lender must provide it, and it makes direct comparisons possible.

- Compare APRs, not just monthly payments. A lower payment can hide higher fees or a longer loan term that costs more overall.

- Ask each broker or lender specifically about wholesale options. Wholesale rates are not available directly to consumers but are accessible through licensed brokers.

- Negotiate. Once you have multiple estimates, go back to your preferred lender and ask them to beat the best offer. Many will.

- Avoid locking in too early. Do not commit to a rate lock until you are confident in your choice and your closing timeline is clear.

"Shopping saves an average of $1,000+ in interest per loan." That savings comes directly from the comparison process, not from luck.

Here is a quick look at what rate differences mean in real dollars on a $360,000 loan:

| Rate | Monthly payment | Annual interest cost | 30-year total interest |

|---|---|---|---|

| 7.25% | $2,457 | $25,786 | $484,580 |

| 6.75% | $2,335 | $24,682 | $460,880 |

| 6.50% | $2,275 | $24,162 | $449,100 |

A 0.5% lower rate saves $1,104 per year. Over 30 years, that is more than $23,000. The time it takes to collect five loan estimates is maybe two hours. That is a strong return.

Use a mortgage shopping checklist to stay organized and make sure you are comparing the same loan type, term, and down payment across every quote. Mixing 30-year and 15-year estimates, or fixed and adjustable rates, will muddy your comparison.

Pro Tip: Get all your quotes within a 14-day window. Credit bureaus treat multiple mortgage inquiries in that period as a single inquiry, so your credit score will not take repeated hits.

Common pitfalls and how to verify your results

Even careful shoppers can get tripped up at the finish line. Here are the traps that catch people most often, and how to sidestep them.

Mistakes vs. solutions:

| Common mistake | What to do instead |

|---|---|

| Applying to only one lender | Get at least three to five quotes |

| Comparing interest rates only | Always use APR for final comparison |

| Ignoring the loan estimate | Review every line on Page 2 |

| Accepting zero-fee loans without checking | Calculate the true total cost including rate |

| Locking in before you are ready | Confirm your timeline before committing |

Zero-fee loans deserve special attention. They sound appealing, but lenders rarely absorb those costs. Instead, they roll the fees into your interest rate. Consider zero-fee loans but evaluate their total cost carefully, because a higher rate over 30 years can cost far more than the fees you avoided upfront.

Here are the most common hidden fee traps to watch for:

- Yield spread premium: A payment from the lender to the broker for placing you in a higher rate loan

- Discount points buried in estimates: Points that lower your rate but inflate upfront costs without clear disclosure

- Junk fees: Vague charges like "administrative fee" or "document preparation fee" that have no regulatory basis

- Rate lock extension fees: If your closing is delayed, extending a rate lock can cost hundreds

The loan estimate is your best defense. Read it line by line before you sign anything.

For additional protection, review mortgage compliance tips to understand your rights as a borrower. Lenders are legally required to provide accurate disclosures, and knowing what to look for puts you in control.

Our take: Most experts oversimplify mortgage savings

The standard advice is "just shop around." It is correct but incomplete. Shopping around only works if you know what you are comparing. Collecting five loan estimates and picking the lowest number is not smart shopping. It is a coin flip with extra steps.

Behavioral biases are the real enemy here. Time pressure from a closing deadline, trust in a familiar bank name, and the emotional exhaustion of the homebuying process push people toward the path of least resistance. That path almost always costs more.

The real edge comes from treating mortgage shopping as a negotiation, not a survey. You are not just gathering information. You are creating competition between lenders for your business. Lender competition directly lowers mortgage rates when borrowers use it intentionally.

Reading loan estimates line by line, asking brokers about wholesale access, and going back to negotiate with a competing offer in hand are the behaviors that actually move the needle. The savings are real. The process just requires more than a passive comparison.

Compare and save with LoFi Rate

You now have the knowledge to shop smarter, compare the right numbers, and avoid the traps that cost most homebuyers thousands. The next step is putting that knowledge to work with the right people in your corner.

LoFi Rate connects you with licensed wholesale mortgage brokers in your state who can shop multiple lenders on your behalf. Unlike retail banks that offer only their own pricing, the brokers in our network access wholesale rates that are not available to the public directly. Whether you are buying your first home or refinancing an existing loan, you can compare brokers and rates with no obligation. Take two minutes to see your loan options and find out what you could be saving.

Frequently asked questions

How many mortgage quotes should I get to avoid overpaying?

You should aim for at least three to five quotes from different lenders and brokers to maximize your savings. Nearly 70% of homebuyers apply with only one lender and consistently pay more as a result.

Is the lowest rate always the best mortgage deal?

No, always compare the APR rather than just the rate, because fees can make a low rate more expensive over time. Total cost using the APR is the only reliable way to compare two loan offers accurately.

What fees should I watch out for when comparing mortgages?

Common fees include origination, processing, underwriting, and appraisal charges. U.S. homebuyers overpay $13 billion annually largely because hidden fees go unreviewed in loan estimates.

Who overpays most on mortgages?

First-time and lower-income borrowers tend to overpay more than repeat or high-income buyers. Less familiarity with the process and less confidence in negotiating are the primary reasons, according to research on mortgage fee overpayment.

Can I negotiate my mortgage fees?

Yes, many fees are negotiable and you should always ask lenders or brokers to improve their offer. Shopping saves over $1,000 on average per loan, and much of that comes directly from negotiation, not just comparison.