TL;DR:

- Refinancing investment properties in 2026 is accessible with conventional and DSCR loan options.

- Using wholesale brokers broadens lender access, saving investors money and securing better rates.

- Proper preparation, understanding requirements, and following a structured step-by-step process ensure a successful refinance.

Carrying a high-rate mortgage on a rental property is not just frustrating — it quietly drains your monthly cash flow and limits how fast you can grow your portfolio. Investors who locked in rates during market peaks or used short-term bridge loans are now sitting on unnecessary costs. The good news is that refinancing an investment property in 2026 is more accessible than many investors realize, especially with DSCR and conventional options available through wholesale brokers. This guide walks you through every stage of the process, from understanding your loan options and meeting eligibility requirements to comparing rates and closing faster.

Table of Contents

- Understand your refinancing options

- Know the requirements and get prepared

- Follow the refinancing step-by-step process

- Calculate costs, compare rates, and avoid common pitfalls

- Why smart investors always use wholesale brokers for refinancing

- Get the best investment property refinance rates now

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Multiple loan options | Investors can choose from conventional, DSCR, rate-and-term, or cash-out refinance loans. |

| Stricter qualifying requirements | Investment property refinances require strong credit, low DTI, and substantial equity. |

| Wholesale brokers unlock savings | Working with wholesale brokers connects you to more lenders and better rates for your investment. |

| Run the numbers | Calculating break-even and comparing offers is key to making refinancing profitable. |

| Maximize long-term gains | Refinancing smartly boosts cash flow, equity access, and future buying power. |

Understand your refinancing options

Not all refinance loans are built the same, and investment properties have their own set of rules compared to primary residences. Before you apply anywhere, you need to know which loan type fits your situation.

The two most common paths are conventional loans and DSCR loans. Conventional loans follow Fannie Mae and Freddie Mac guidelines, require personal income verification, and typically offer lower rates for borrowers with strong credit and W-2 income. DSCR loans are popular for investors because they require no personal income verification and can close faster, making them ideal for self-employed investors or those with complex tax returns.

Here is a quick breakdown of the main loan types:

| Loan type | Max LTV | Income verification | Best for |

|---|---|---|---|

| Rate-and-term (conventional) | 80% | Yes | W-2 investors, lower rates |

| Cash-out (conventional) | 75% | Yes | Equity access, portfolio growth |

| DSCR rate-and-term | 80% | No (rent-based) | LLC holders, self-employed |

| DSCR cash-out | 75% | No (rent-based) | STR owners, complex portfolios |

| Hard money exit | Varies | Minimal | Bridge loan payoff, fast close |

According to cash-out guidelines, rate-and-term loans allow up to 80% LTV while cash-out refinances cap at 75% LTV for investment properties. That 5% difference matters a lot when you are pulling equity for your next acquisition.

If your property is held in an LLC or is a short-term rental, conventional lenders may decline you outright. DSCR programs, available through investment loan options at wholesale brokers, are specifically designed for these scenarios. You can also explore home equity strategies to understand how equity access fits into a broader portfolio plan.

Pro Tip: If your rental income covers the mortgage payment at a 1.0 or higher ratio, a DSCR loan may qualify you even if your personal tax returns show losses from depreciation. This is one of the most overlooked advantages in investment refinancing.

Know the requirements and get prepared

Once you know which loan type fits your situation, the next step is confirming you meet the eligibility thresholds and getting your documents in order. Investment property refinances are held to stricter standards than primary home loans.

Refinance requirements for investment properties typically include a credit score between 620 and 720 or higher, a debt-to-income ratio below 45 to 50%, at least 25 to 30% equity in the property, and cash reserves covering several months of payments. For DSCR loans specifically, DSCR loan eligibility requires a minimum 660 credit score, a DSCR ratio of 1.0 or higher, and LTV limits of 80% for rate-and-term or 75% for cash-out.

Here is a side-by-side look at key requirements:

| Requirement | Conventional | DSCR |

|---|---|---|

| Minimum credit score | 620-720+ | 660+ |

| Income verification | Tax returns, W-2s | Rent rolls, lease agreements |

| Max DTI | 45-50% | Not typically calculated |

| Minimum equity | 25-30% | 25-30% |

| Reserves required | 6-12 months | 3-6 months |

For loan requirements for investment properties, lenders also look at property type, occupancy status, and whether the loan is in your personal name or an LLC.

Documents you will typically need include:

- Last 2 years of federal tax returns (conventional)

- Current signed lease agreements and rent rolls

- Recent bank statements showing reserves

- Property insurance declarations page

- Current mortgage statement

- Government-issued ID

- LLC operating agreement (if applicable)

Review refinance tips for investors before you start gathering documents. Also, understanding how to unlock better refinance rates through broker access can change your approach entirely.

Pro Tip: One of the most common delays is a missing or expired lease. Make sure all tenant leases are current and signed before you apply. Lenders will not count projected rent on a vacant unit without a valid lease in place.

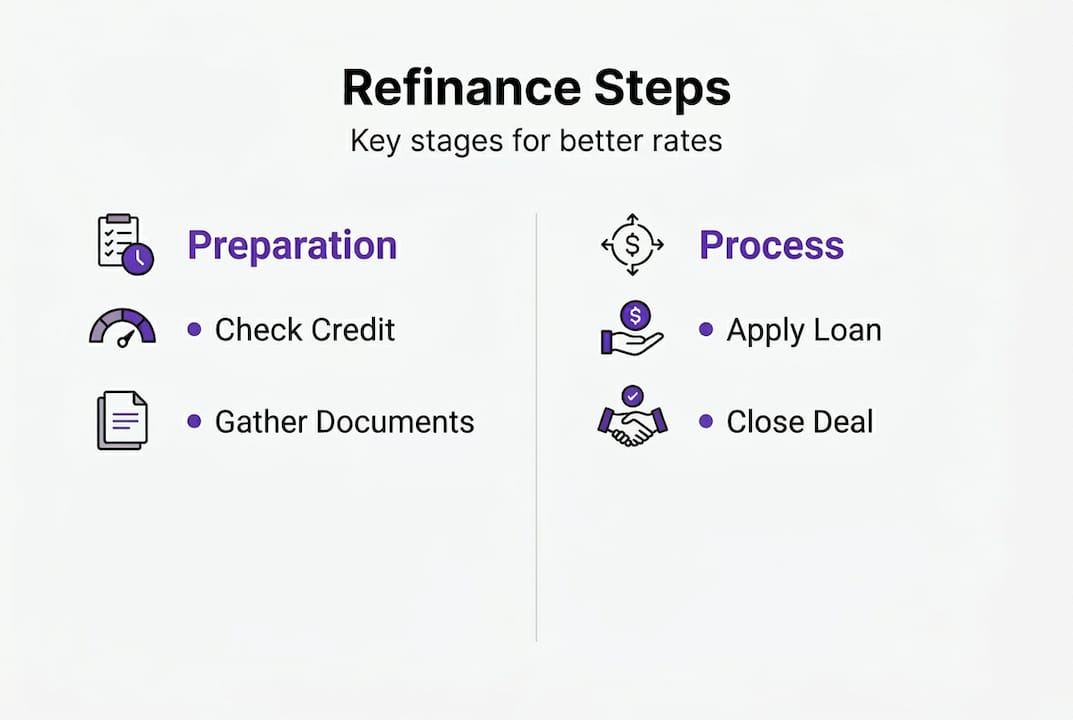

Follow the refinancing step-by-step process

Knowing your options and meeting the requirements is half the battle. The other half is executing the process efficiently so you close on time without costly surprises.

Here is the standard refinancing workflow for investment properties:

- Assess your goals and equity position. Know what you want: lower rate, cash out, or switching loan types. Pull a current property value estimate.

- Check your eligibility. Review your credit score, DTI, and equity before approaching lenders.

- Gather your documents. Collect everything from the list above before you start any application.

- Shop brokers and lenders. Get multiple quotes. Do not settle for the first offer.

- Submit your application. Your broker submits to the lender that best fits your profile.

- Order the appraisal. The lender will order an independent appraisal to confirm property value.

- Underwriting review. The lender verifies all documents and issues conditions.

- Close and fund. Sign final documents and receive your new loan terms.

"The biggest mistake investors make is skipping step four. Comparing just two lenders can mean the difference between a 7.5% and an 8.25% rate on a $400,000 loan. That gap costs thousands per year."

Wholesale brokers access 50 to 100 or more lenders and offer investor-specialized programs that retail banks simply do not carry. Following a clear refinancing workflow helps you avoid the most common bottlenecks: appraisal gaps, missing documents, and underwriting conditions that stall your close.

DSCR loans can close in 15 to 35 days when documents are clean. Conventional refinances typically take 30 to 45 days. Learn more about shopping lenders with brokers to speed up your timeline.

Pro Tip: Have your appraisal comps ready. If you know your neighborhood has strong rental comparables, share recent lease data with the appraiser. A higher appraised value means more usable equity and better LTV ratios.

Review the full investment property refinance process to make sure you understand each stage before you start.

Calculate costs, compare rates, and avoid common pitfalls

Refinancing costs money upfront, so you need to know exactly when and how you will break even before you sign anything.

Investment property refi rates run 0.5% to 1% above primary home rates. In 2026, DSCR rates typically range from 7.5% to 9% depending on credit, LTV, and property type. Conventional investment property rates sit slightly lower for well-qualified borrowers.

Closing costs average 2% to 5% of the loan amount. To calculate your break-even point, divide total closing costs by your monthly savings. If you save $300 per month and pay $6,000 in closing costs, your break-even is 20 months. If you plan to hold the property beyond that, the refinance makes financial sense.

Here is a rate and cost comparison snapshot:

| Loan type | Typical 2026 rate | Closing cost range | Break-even estimate |

|---|---|---|---|

| Conventional (investment) | 7.0-7.75% | 2-4% | 12-24 months |

| DSCR | 7.5-9.0% | 2-5% | 18-30 months |

| Cash-out refi | 7.25-8.5% | 2-5% | Depends on use of funds |

Common pitfalls to avoid:

- Refinancing too often. Each refi resets your break-even clock and adds fees.

- Selling before break-even. If you plan to sell within 12 to 18 months, the costs may not justify the savings.

- Ignoring prepayment penalties. Some DSCR loans carry prepayment penalties of 3 to 5 years. Read the terms carefully.

- Comparing rates without comparing APR. APR includes fees and gives a more accurate total cost picture.

- Not locking your rate. Rates can shift during underwriting. Ask about rate lock options.

With investment vs primary rates running higher, finding every basis point of savings matters. Strategies to get lower mortgage rates through wholesale access can meaningfully reduce your long-term cost of capital. Notably, 71% of real estate investors plan to make additional purchases in 2026, making rate optimization a critical part of portfolio strategy.

Why smart investors always use wholesale brokers for refinancing

Here is a perspective that most rate-shopping articles skip: the investor who calls their bank directly is almost always leaving money on the table. Not because the bank is dishonest, but because the bank only sells its own products.

A wholesale broker works differently. Wholesale brokers access 50 to 100 or more lenders, including specialty investors that carry DSCR programs, LLC-friendly loans, and short-term rental approvals that retail banks do not offer. When you go direct, you get one menu. When you use a broker, you get the whole market.

Experienced investors know this. They build long-term relationships with brokers who understand their portfolio structure, their entity setup, and their growth goals. That relationship pays dividends every time a new deal comes up. The broker already knows your profile and can move fast.

Another misconception is that brokers cost more. In wholesale lending, the lender pays the broker's compensation, not you. You get broader access without paying extra for it. The savings from saving with brokers on even a single refinance can easily exceed what most investors spend on property management for a full year. That is not a small detail.

Get the best investment property refinance rates now

If you have read this far, you already know more than most investors do when they walk into a bank. Now it is time to put that knowledge to work.

LoFiRate connects real estate investors with licensed wholesale mortgage brokers in their state who specialize in investment property refinancing. Instead of one lender's pricing, you get access to a broader market, including DSCR programs, cash-out options, and LLC-friendly loans. Whether you are optimizing an existing rental or pulling equity for your next acquisition, explore your refinance services and loan options through brokers who understand investor needs. There is no obligation to proceed, just a clearer picture of what is available to you in 2026.

Frequently asked questions

What is a DSCR loan and why is it popular for investors?

A DSCR loan qualifies borrowers based on the property's rental income rather than personal income, making it ideal for investors with multiple properties or variable income. DSCR loans are preferred for investors because no personal income verification is required.

How much equity do I need to refinance an investment property?

Most lenders require at least 25% equity for a rate-and-term refinance and 30% for a cash-out refinance on investment properties. Equity needs of 25-30% apply to most standard refinance programs.

How fast can I close an investment property refinance?

DSCR loans can close in as little as 15 to 35 days when your documents are complete and clean. Conventional refinances typically take 30 to 45 days from application to funding. Faster DSCR closes are one of the main reasons investors prefer this loan type.

Are interest rates for investment refinances higher than for primary homes?

Yes, investment refi rates typically run 0.5% to 1% higher than rates on a primary residence refinance due to the increased risk lenders associate with non-owner-occupied properties.

When should I avoid refinancing my investment property?

Avoid refinancing if your expected monthly savings are small, you plan to sell the property before reaching break-even, or if prepayment penalties on your current loan would offset the gains. Frequent refis or selling soon can quickly eliminate any financial benefit.

Recommended

- How to refinance your mortgage for better rates and savings

- Refinance evaluation process: step-by-step guide to better rates

- Unlock Better Refinance Rates: How Brokers Help Homeowners Save

- Home equity in refinancing: strategies for 2026

- 7 Smart Examples of Property Investment Strategies - ULI & LISA Mallorca Property Blog

- How to Leverage Real Estate Equity for Lasting Wealth